The recent increase in interest rates is forcing institutions and investors to reassess growth strategies in the single-family rental market, according to a report from Yardi Matrix.

“With home sales cooling as rising mortgage rates bump up against soaring property values, institutional single-family rental property companies are adjusting growth strategies and facing the prospect of lower total returns,” the report says.

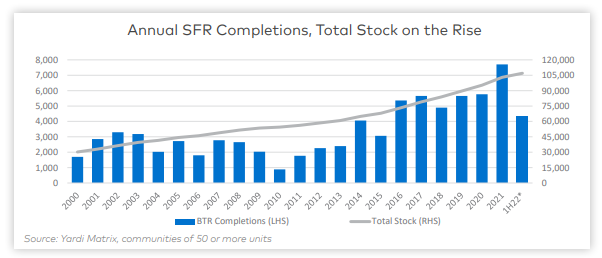

Growth in the near future, however, may be concentrated on build-to-rent projects, which are being delivered at record levels.

Institutional Ownership Of Single-Family Rentals

Institutions’ growth is currently focused on build-to-rent projects or acquiring portfolios from smaller owners.

“Institutional ownership of single-family rentals is growing rapidly as investors seek property segments with outsize growth prospects as long-term demand for single-family rentals solidifies.

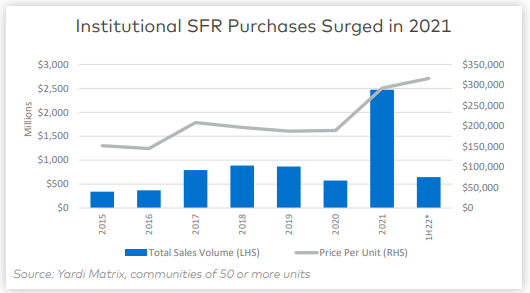

“Institutions have committed more than $60 billion to buying single-family homes over the past year, according to various corporate announcements and news articles.”

Single-family Rentals Will Continue to be in Demand

While costs of homes has skyrocketed, demand for homes has continued to be strong. And there are multiple drivers for this demand.

“Some households decided during the pandemic lockdowns to move out of urban areas to suburbs to get more space for children and pets, and as a better environment to work from home.”

Plus historically low interest rates contributed to a spike in home buying.

The average 30-year mortgage in the U.S. dipped to 2.8 percent in late 2021, about one-third of the 7.8 percent 50-year average and half of the 30-year 5.7 percent average, according to Freddie Mac.

The weakening of the single-family for sale market and affordability should keep the single-family for rent market strong, Yardi Matrix says in the report.

Families Will Continue To Rent

The industry looks to be fundamentally sound and poised for growth, Yardi Matrix says.

“Homeownership will likely be in for a bumpy ride over the next year or two as home prices reset and mortgage rates remain at recent higher levels, but that should be good news for single-family rentals. Families still aspire to the amenities provided by detached houses, and if they can’t afford to purchase, they will rent.

“What’s more, supply of single-family homes is likely to remain weak as supply-chain issues delay materials, development and labor costs skyrocket, and the entitlement process delays deliveries. The annualized number of new housing starts dropped 14% between April and June, moving in the wrong direction as the U.S. faces a long-term shortage of housing units estimated at 2 million to 4 million. While the housing shortage is unfortunate on many levels, it improves the investment prospects of the single-family rental market.”

About Yardi Matrix

Yardi Matrix researches and reports on multifamily, office and self-storage properties across the United States, serving the needs of a variety of industry professionals. Yardi Matrix Multifamily provides accurate data on 18+ million units, covering more than 90 percent of the U.S. population. Contact the company at (480) 663-1149.