Keeping jobs during downturns, often called “durable employment,” shows up much more in some cities than in others, according to new research from Yardi Matrix.

Job stability is key to tenants being able to pay rent in the multifamily industry, as well as to landlords who are struggling to collect rent during the pandemic.

Employment losses caused by the COVID-19 pandemic have been unevenly spread across the economy, so Yardi Matrix studied which metros have the highest concentration of jobs in finance, professional and technical services, and government—sectors that have lost the lowest proportion of jobs.

“Metros with the highest percentage of durable jobs generally are home to a government capital, state university and/or strong presence of knowledge-based industries,” the report says.

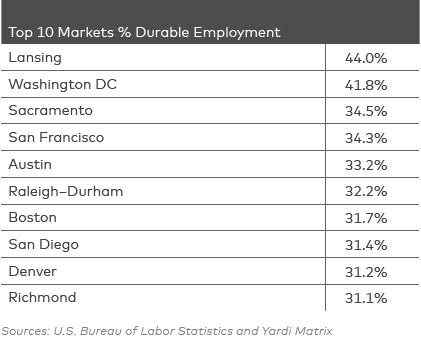

Metros with the most durable jobs

- Lansing, Mich. – 44 percent

- Washington, D.C. – 41 percent

- Sacramento – 34.5 percent

“All of which include federal or state government capitals. The Lansing/ Ann Arbor metro also is home to the University of Michigan and Michigan State University.

“Washington has for decades been among the most consistently performing U.S. metro for commercial real estate because of the stability afforded by being the capital of the U.S. government. The presence of government-related industries that include lobbying, legal, trade groups, foundations, think tanks, etc., gives the metro an employment base that is extremely stable,” the report says.

Finance jobs also help keep cities stable

Jobs in banking, insurance and real estate also help with “durable” jobs.

Roughly two-thirds (33) of the Yardi Matrix top 50 metros are above the national average, which reflects the concentration of financial jobs in urban centers.

Metros with the highest percentage of jobs in this sector are:

- New Haven, Conn. – 9.5 percent

- Dallas – 9.3 percent

- Jacksonville – 9.3 percent

- Phoenix – 9.2 percent

- Tampa – 8.8 percent

Jobs During Downturns Conclusion

“The goal of this study was to determine metros’ exposure to the job segments that have performed the best at the outset of the pandemic. The upshot is that having a base of government jobs (including state universities) and/or concentrations of knowledge-based industries including (but not limited to) finance and technology should help metros weather the downturn,” the report says.

“Questions remain about the economy in coming quarters. Our study was based on jobs lost through April, and the composition of job losses may evolve. For example, government has lost relatively few jobs so far, but we could see massive layoffs of state employees if the federal government doesn’t provide aid to states. And the job picture could change rapidly as states begin to reopen. Most unemployment claims have been filed by furloughed workers that are subject to callbacks as the economies of those states reopen,” Yardi Matrix says in the report.

Download the full report here: Special research bulletin: Which Metros Have the Most Durable Employment Sectors?

Job Postings Still Strong for Apartment Industry