Seattle rents declined 0.2 percent over the past month, the third month in a row of slight declines, but have increased slightly by 1.8 percent year-over-year, according to the latest report from Apartment List.

Median rents in Seattle are $1,345 for a one-bedroom apartment and $1,675 for a two-bedroom.

Seattle proper rents over the past year lag the state average increase of 1.9 percent.

Rents rising across the Seattle metro

During the past year, rent increases have occurred not just in the city of Seattle, but across the entire metro.

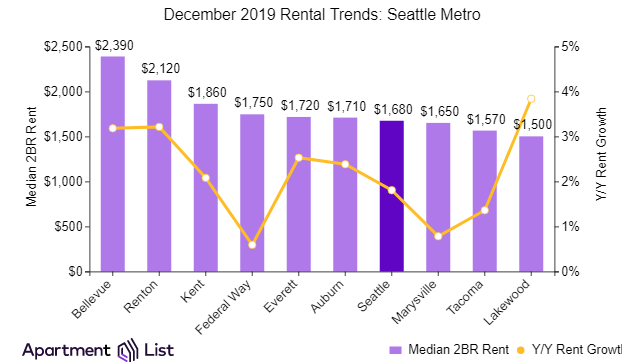

Of the 10 largest cities that Apartment List has data for in the Seattle metro, all of them have seen prices rise.

Here’s a look at how costs compare across some of the largest cities in the metro.

Lakewood has the least-expensive rents in the metro, with a two-bedroom median of $1,502; the city has also experienced the fastest rent growth in the metro, with a year-over-year increase of 3.8 percent.

Over the past month, Auburn has seen the biggest rent drop in the metro, with a decline of 0.7 percent. Median two-bedrooms there cost $1,710, while one-bedrooms go for $1,373.

Bellevue has the most expensive rents of the largest cities in the metro, with a two-bedroom median of $2,389; rents decreased 0.4 percent over the past month but were up 3.2 percent over the past year.

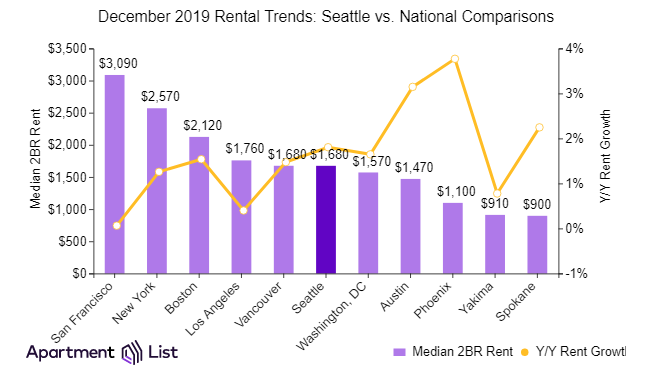

Comparable nationwide cities show more affordable rents than Seattle

As rents have increased slightly in Seattle, a few similar cities nationwide have also seen moderate growth. Compared to most other large cities across the country, Seattle is less affordable for renters.

Rents increased slightly in other cities across the state, with Washington as a whole logging rent growth of 1.9 percent over the past year. For example, rents have grown by 2.2 percent in Spokane and 1.5 percent in Vancouver.

Nationwide, rents have grown by 1.4 percent over the past year compared to the 1.8 percent increase in Seattle.

While Seattle rose slightly over the past year, many cities nationwide also saw increases, including Phoenix (+3.8 percent), Austin (+3.1 percent), and DC (+1.6 percent).

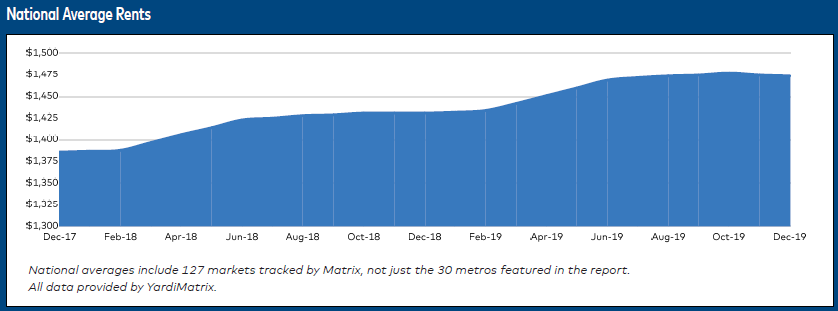

There was a weak end to a solid year for multifamily, with national average rents falling by $1 in December, according to the latest report from Yardi Matrix.

The report says 2019 will go down as a year without much drama in the multifamily sector as U.S. rent growth finished at a solid 3 percent.

Highlights of the report

The average U.S. rent fell $1 in December to $1,474, with the growth rate falling 10 basis points from November. That said, U.S. multifamily rents finished a remarkably consistent 2019 up 3.0%. Year-over-year growth remained between 3.0% and 3.3% the entire year.

Rents were essentially flat for the fourth quarter, which is a normal seasonal trend. The last time rents grew significantly during the end of the year was 2014 and 2015.

Rent growth continues to be strong in all regions, led by secondary markets in the West and Southeast. Phoenix, Las Vegas, Sacramento and Nashville were among the top-performing metros all year. However, growth decelerated significantly during the year in some metros, notably San Jose, Orlando and Denver.

Rent gains softened, but the market is steady

The report says “the market is sound, with no red flags on the immediate horizon.

“Despite deliveries of roughly 300,000 units for the year, the occupancy rate for stabilized properties was 94.9 percent as of November, down only 10 basis points over the last year,” it says.

A healthy job market and low unemployment also helped handle the new deliveries of apartments during 2019.

Rent growth softened, yet again, to 3.0 percent on a year-over-year basis in December, down 10 basis points from November. Year-over-year rent growth is at its lowest level since May 2018, when it reached 2.9 percent.

Phoenix (7.7 percent) and Las Vegas (5.4 percent) have topped the rankings together for 16 months and counting. The last time these two markets did not top the charts was in September 2018, when Orlando claimed the first-place position, with Las Vegas and Phoenix following closely behind.

Three California markets—Sacramento (5.1 percent), the Inland Empire (4.1 percent) and Orange County (3.9 percent)—ranked in the top 10. Despite California’s affordability issues and the recent passage of statewide rent control, these three markets continue to find a way to increase rents.

Bay Area is weakening

“The Bay Area is weakening due to concern over growth in startup technology firms, the feeble IPO market and the lack of affordable housing, which is prompting large employers to seek cheaper markets,” the report says.

San Jose started the year at 4.7 percent and ended up -0.3 percent.

San Francisco started at 4.5 percent and ended at 1.6 percent.

Even Denver started at 3.4 percent and ended at 1.5 percent.

“All of these metros have a strong economic base, so it would seem likely that growth will rebound. Despite pockets of concern, 2020 should be a healthy year,” Yardi Matrix says in the report.

Also the report said multifamily continues to benefit from abundant debt capital sources. Total apartment lending in 2019 was on track to reach 2018’s record $338 billion.

Rental pricing and how to set the price of their rentals is naturally one of the first questions asked by owners.

They often have some idea – which, unsurprisingly, may lean towards the optimistic end of the spectrum. Independent pricing sources are available to provide pricing guidance and counter any internal bias. But there also are some general guidelines you can calculate yourself based on size, which are very important to understand regarding total rental yields.

Pricing is important both directly and indirectly. Directly as rental income, and indirectly in that it determines occupancy – or vacancy – and lease-up times. High pricing may result in higher volatility of rent payments and lower total revenues due to longer lease-up times or increased vacancy.

Pricing also affects the pool of applicants. The higher the price, the smaller the pool of applicants. Using a common 3x rent-to-income approach diminishes the pool quickly as you move into the upper echelons of household income. For example, rent of $3,000 per month would require an annual household income of $108,000 – which equates to roughly the 70th percentile of household income in the Portland/Vancouver MSA. Said another way, only 30 percent of the population would qualify to rent your unit based upon income. Other exclusions (such as no pets) may quickly reduce that pool further. Rental-pool size is a larger subject, but you get the idea.

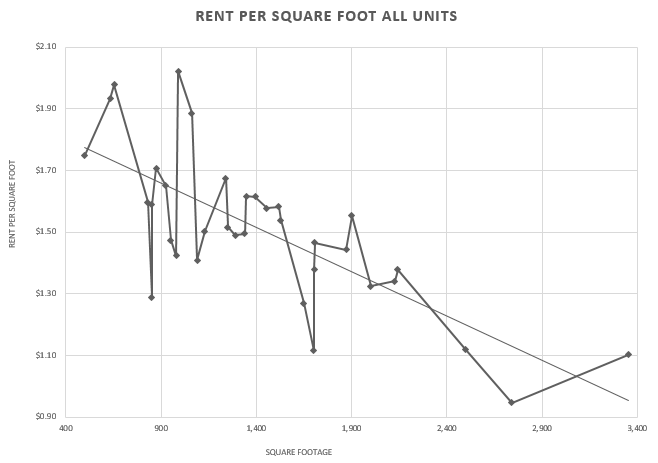

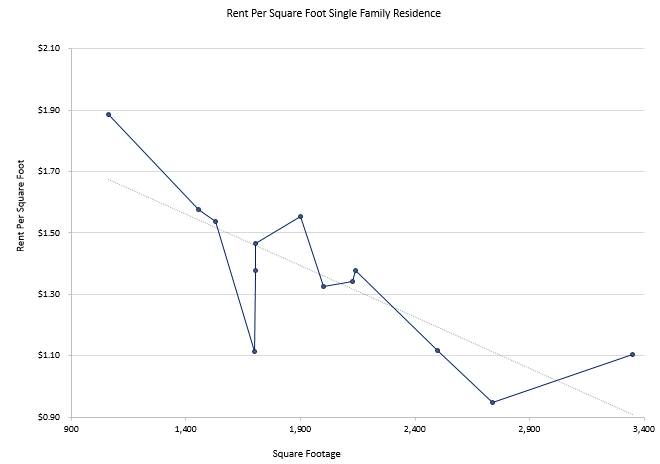

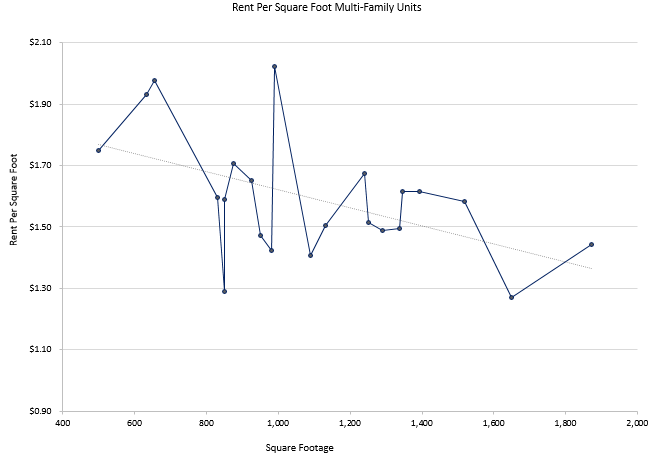

As housing increases in size, pricing can be difficult to estimate due to diminishing returns. While the difference tenants are willing to pay for 200 more square feet may be significant as square footage increases from 800 to 1,000 square feet, the extra they are willing to pay as it increases from 2,000 to 2,200 may be significantly less. The diminishing-return trend can be calculated by plotting available rentals and their asking prices.

Rental pricing per square foot

The following graph illustrates the declining price-per-square-foot as the rental size increases. This graph includes all properties currently listed for rent on Zillow in West Linn, OR (as of December 14, 2019). The price per square foot is shown on the vertical axis and the total square foot of the unit on the horizontal. For example, a 1,400-square-foot house may rent for $1.50 per square foot ($2,100 per month) while a 2,500 square foot house will rent for $1.10 per square foot ($2,750 per month).

There is a distinct trend of diminishing income per square foot as size increases. The breadth of pricing at a given square footage may stem from various factors, including location of rental, quality, included amenities, pet acceptance, and simple pricing errors.

As you may imagine, type of rental (single- or multi-family) affects the slope of the rental-income curve. The following charts illustrate single- and multi-family separately. The range of square footage for multi-family units is more compact than SFR.

Interestingly, the slopes of the trendlines for both single and multi-family units decrease at very similar rates. The decline in average rent as size increases is as follows for this group of rentals:

SFR

3.3¢ per 100 square feet

33¢ per 1,000 square feet

Multi

2.9¢ per 100 square feet

29¢ per 1,000 square feet

At first glance those may seem like small numbers but extrapolating into annual rents for long-term properties the results can be highly significant. The yield differential between a 1,500 square foot rental and a 2,000 square foot unit is very significant – especially when you factor in the additional costs of purchasing, operating, and maintaining the larger homes – think roofs, window counts, flooring, yard maintenance, etc.

Third party pricing guides are very helpful in providing an unbiased (albeit unseen) estimate of your property. And absent notable differentiators such as location or amenities, are likely reasonably accurate. Rentometer (www.rentometer.com) and RentRange (www.rentrange.com) are 2 sites worth a visit. And again, Zillow will automatically provide an amount that will be seen by all visitors. The combination of these 3 estimates will provide you with a default rental amount.

Keep in mind that renters will likely also see estimates – particularly on Zillow – and may assume that your higher price is out of line with the market. Owners must counter that price anchoring effect with photos and a compelling description that justifies a higher rent variance. On a side note, while I love Craigslist please exercise caution when using it for anything rental related including rent pricing. Most rental horror stories begin with “I saw an ad on Craigslist…”

Using these third-party pricing sources will you give several data points as a backdrop for your pricing decision. Understanding the diminishing return trends in pricing will also help to guide your pricing – and investment decisions. Good luck!

About the author:

Steve Geidl

Steve Geidl is a licensed Property Manager and Residential General Contractor living in West Linn, Oregon. He can be reached at geidl.steve@gmail.com.

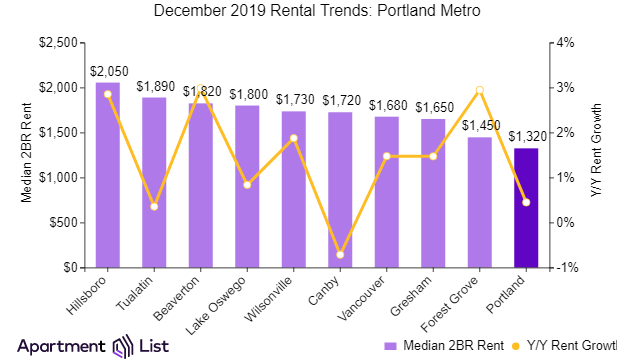

Portland rents continued their decline for the third month in a row after the last increase in September, according to the January report from Apartment List.

Portland rents have declined 0.5 percent over the past month, but have been relatively flat at 0.4 percent in comparison to the same time last year. Median rents now are $1,122 for a one-bedroom apartment and $1,324 for a two-bedroom in Portland.

Rents rising across the Portland metro

While rents have remained steady in the city of Portland throughout the past year, cities across the metro have seen a different trend. Rents have risen in nine of the largest 10 cities in the Portland metro for which Apartment List has data.

Here’s a look at how rents compare across some of the largest cities in the metro.

Beaverton has seen the fastest rent growth in the metro, with a year-over-year increase of 3.0 percent. The median two-bedroom there costs $1,824, while one-bedrooms go for $1,546.

Over the past month, Canby has seen the biggest rent drop in the metro, with a decline of 2.6 percent. Median two-bedrooms there cost $1,725, while one-bedrooms go for $1,462.

Portland proper has the least expensive rents in the Portland metro, with a two-bedroom median of $1,324.

Hillsboro has the most expensive rents of the largest cities in the Portland metro, with a two-bedroom median of $2,055; rents fell 1.0 percent over the past month but rose 2.9 percent over the past year.

Portland rents more affordable than many other large cities nationwide

Rent growth in Portland has been relatively stable over the past year, while some other large cities have seen more substantial increases.

Portland is still more affordable than most comparable cities across the country.

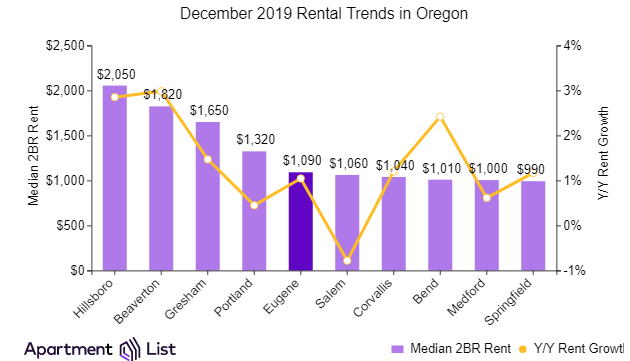

Oregon as a whole has logged 1.5 percent year-over-year growth, while rent trends across other cities throughout the state have varied. For example, rents have grown by 1.0 percent in Eugene and have fallen 0.8 percent in Salem.

While rents in Portland remained moderately stable this year, similar cities saw increases, including Phoenix (+3.8 percent), Las Vegas (+3.2 percent), and Austin (+3.1 percent); note that median 2BR rents in these cities go for $1,099, $1,193, and $1,471 respectively.

Eugene Rents Continue Decline, While Corvallis is Flat

Eugene rents have declined 0.5 percent over the past month, but have increased slightly by 1.0 percent in comparison to the same time last year, according to the latest report from Apartment List.

Median rents in Eugene are $820 for a one-bedroom apartment and $1,091 for a two-bedroom.

This is the third straight month that the city has seen rent decreases after an increase in September. Eugene’s year-over-year rent growth lags the state average of 1.5 percent, as well as the national average of 1.4 percent.

Corvallis rents flat over the past month

Corvallis rents have remained flat over the past month, however, they are up slightly, by 1.2 percent year-over-year.

Median rents in Corvallis are $828 for a one-bedroom apartment and $1,039 for a two-bedroom.

Salem rents decline sharply over the past month

Salem rents have declined 0.7 percent over the past month, and have decreased moderately by 0.8 percent in comparison to the same time last year.

Median rents in Salem are $808 for a one-bedroom apartment and $1,062 for a two-bedroom.

This is the third straight month that the city has seen rent decreases after an increase in September.

The top 3 questions property managers ask when they call a roofer are because property managers have two interests at heart – they don’t like their roofs to leak and they don’t want to spend any more money on them than they have to, according to Eric Skoog, owner of Sunvek Roofing in Phoenix.

No. 1 – Can we do a localized repair rather than replace the whole roof?

That is their first fear, that we are going to come back and say everything needs to be redone. And sometimes that is the case but usually we are able to do one plane or face of the roof, or in a flat roof just a section of it as far as repairs go. Our general experience with flat roofs is that if we can catch it early enough we can do roof restoration. If maintenance is deferred too long then we are looking at replacement. And there is a tremendous difference in cost.

No. 2 – How much will it cost?

Money is always an issue.

Can it be a localized repair, and what will it cost?

No. 3 – How quickly can you get it done?

If it is a leak they want us there immediately to at least stop the leak and then come back when it is not raining to do the repairs.

“With the property managers that we deal with it really has been nice that for the most part they are proactive,” he said.

“They are looking ahead for their budget for next year. They want us to walk their roofs and give them our honest opinion about the condition of the roofs and what they can do to maintain them rather than having to replace them,” he said.

“Regular maintenance and a good roofing contractor can help. If, for example, property managers have their roofs walked at least annually, and preferably semi-annually, the roofer can verify all roofing penetration areas are water-tight and sealed as needed,” Skoog said. “Also, on pitched roofs, valleys need to be cleaned out so water or snow can move quickly off the roof, resulting in less chance of damage and water entry.

“I think quite often, building owners mistake maintenance with roofing cost. Our experience is that if you maintain a roof – meaning having someone go up there periodically, do minor repairs, check the roof to make sure everything is in good shape, you are much more likely to be able to extend the life of that roof than you are by ignoring it in order to save money until it leaks,” he said.

Especially that is the case with flat roofs.

“Very typical on multifamily roofs, you will have mansards, eaves or porch covers on the exterior and a flat roof in the central area simply because it is a less costly way to build initially, and you hide most of the roof,” Skoog said.

“You typically have larger, flat, expanses of roof to deal with. And those flat roofs are going to be some form of roll product – which is either self-adhered, heat-sealed, or some form of adhesive – or maybe spray polyurethane foam,” he said.

“With foam roofs you do have the issue that they need to be periodically coated. It is much less expensive to maintain than replace. With a roll product you have the issue that seams can pop open, sealant can come loose, and you can have water entry.

“If those roofs are periodically checked and maintained you can defer the need for major investments in restoring them.

“Additionally, with any flat roof system you should be able to coat it at some point and extend the useful life, thereby saving significant sums of money rather than letting that system deteriorate to a point where you need to replace it.

“It is much more cost effective to maintain, coat and restore a roof than to ignore, repair and replace a roof. And of course your tenants tend to be happier when they don’t have water leaking in their unit,” he said.

Cost of an annual roof walk for preventive maintenance?

The cost of a roof walk check by a roofer is going to vary depending on the size of the apartment complex. If you have a number of buildings, the unit investment is going to be lower.

“But I think for a typical, 12-unit multifamily building, which might be either two or three stories, it would be reasonable, semi-annually, to have somebody walk the roof, check the penetrations, assess the need for repairs and/or replacement or restoration for $500 to $1,000,” he said.

The larger the number of units, the more cost effective it could be. It could get down to as little as $50 per unit dependent on the type of roof system, he said.

Tenant communication is key for roofers in roof work

Photos courtesy of Sunvek Roofing

“The ideal client for us is one who is proactive. They want to maintain their building. They want to keep their tenants happy. And they see the value of having a roof system that keeps water, snow and ice out because that is much cheaper than having to come back and fix it,” he said.

He gave an example of how it worked at an apartment complex he replaced the roofs on several years back.

“The complex had roughly 450 units, so we had hundreds of tenants to deal with. The complex consisted of 20 buildings. We did one building, then moved to the next, and so on through the complex. The property management company was very good to work with. We sent notice in advance saying, ‘We will be on building A, starting this date, we expect it will take a week to 10 days.’ They would then send a notice to the tenants and post a notice on every door. Plus they sent digital communication, either text or email to every one of the tenants so everyone would know that we were coming.

“They were also really good about including a telephone number to call so that if the tenants had any questions, they could call the property management office, or our office, and one of us would address the issue.

“Our crews went there, set up our tape lines, and did our work. First we had to replace underlayment on the tile roofs, then we did the repair work and coating to restore the flat roofs. It worked out as well as it did because the property management company was very willing to work with us to ensure their tenants were communicated with – as well as to ensure our work crews had the information they needed to do their work.

“For example, they asked the tenants to please not park in these spaces where we need the space available to get our equipment in. And we, on our part, tried to make sure the tenants were notified at least a week or two in advance that we are going to be on their building – ‘here’s what you can expect, here are the hours we will be here, if you have any questions here is who you can contact.’

“It works really well when the property management company and the roofer can work together to coordinate the work,” he said.

Starting a roof repair can highlight other maintenance issues

“We have had tenants approach our roofing crews and ask, ‘Ok that’s great you are getting the roof fixed but when are you going to come back and fix the damage inside my unit from the leaks?’

“And our guys say we really don’t know the answer to that. But, our guys have been very good about telling the tenants we will pass the information on to the property management company because that is not typically something we do. And typically the property management company has somebody who does that type of repair,” Skoog said.

Local codes and requirements for roofs and roofers

In some states each community may adopt its own building codes and standard requirements. So you do have variation in requirements. Property management has to be sure and check all locally applicable codes and requirements and be sure your roofer knows them as well.

Rental maintenance jobs – no matter the circumstances – that should be left to a maintenance professional is the maintenance checkup from Keepe this week.

Fixing a paint job yourself that didn’t turn out right is one thing. However having to pay thousands of dollars for repairing the structural damages that resulted from a poorly done plumbing, electrical or HVAC job is another.

Leaving these maintenance projects to a professional will make what you spend worth the peace of mind and safety you’ll get in return.

No. 1 – Hands-on Electrical Work

Repairing or re-configuring wiring is not do-it-yourself project. You might change a lightbulb or even install a new light fixture – maybe. But there is a reason why electricians charge higher rates. They have to go through extensive professional training to prepare for safely tackling wiring repairs. A property’s wiring/electrical configuration can be made unique by different electrical work being done throughout the years. This makes “one size fits all” procedures that are advertised online completely useless. The main risk of attempting electrical work yourself is being shocked or starting a fire. Both potentially deadly side effects to handling wiring without experience. Also doing it yourself can risk creating further damage that requires more extensive, and pricier, repairs down the road.

No. 2 – Gas Appliances

Working on gas appliances implies handling hazardous materials and facing potentially deadly side effects. Gas furnaces, ovens, water heaters or dryers should only be worked on by professionals. Turning off the gas while working on them is not a sufficient precaution. Gas leaks can easily be created by a poorly done project or reassembly. That could expose your rental home to a leak that could cause carbon monoxide poisoning, or worse, an actual explosion.

No. 3 – HVAC

Our HVAC professionals strongly encourage property owners and tenants to stick to the basics. That means changing filters and cleaning around vents. Let the professionals handle anything more serious or complicated. Air conditioning and furnace repairs affect the air quality within a property. Poorly installed or maintained equipment can reduce efficiency and inflate. It can also be the root cause of respiratory infections and problems for those living and breathing in the property. Just like electrical professionals, HVAC professionals are required to undergo specialized training. That training allows them to obtain special licenses that legally allow them to work with certain materials. When refrigerants are concerned, one would not be complying with the Environmental Protection Agency’s (EPA) regulations by working on air conditioning as a do-it-yourselfer.

No. 4 – Plumbing

That clogged drain might have been a piece of cake to work on. However major plumbing projects like re-routing existing plumbing or spot-fixing a leak is a whole different story. Water damage is extremely costly to repair. Even a small leak can be the culprit behind a plumbing-related emergency that costs a property thousands of dollars in damages.

No. 5. – Chimney Sweeps

Chimneys require regular cleanings/chimney sweeps to clear combustion buildups that could cause fires or restrict adequate air flow, which degrades the air quality within the property and can potentially cause severe breathing problems. Our experts encourage scheduling a yearly inspection to ensure everything is in adequate working condition. The actual inspection and cleanup involve working closely to toxic fumes and flammables, which only a professional is safely equipped for.

No 6 – Structural Alterations

Created by Freepik.com

Do not demo existing walls to “open up the space” like you see on TV. Demolishing a wall that might not only be bearing, but also encasing other circuits and piping, will permanently damage a property’s systems and potentially cause major, long-lasting structural damages. Additionally, official permits are generally needed to move forward with structural alterations, which is why working with a professional is always best.

No. 7 – Pest Extermination

Over-the-counter products, traps and gadgets are rarely ever enough to guarantee the successful extermination of an established pest colony. Those solutions result in a “surface clearing” without actually affecting nests and nearby populations. Stronger chemicals should be handled by a professional as they are extremely toxic to humans. Professional exterminators will be able to assess the characteristics of a property and treat the area in the most effective way. They are trained in the safe handling of chemicals and products.

No. 8 – Siding Installation

Most people attempting the installation of siding by themselves are trying to save money. Our experts warn that poorly secured siding can allow for harsh weather to strip it off and/or for moisture to penetrate underneath. That can damage the frame of the home and thus require repairs that are vastly more expensive than what having a professional doing the installation costs.

No 9 – Tiling

Tiling is one of those projects that is not as dramatically high-risk when it comes to DIY. However it is important to keep in mind that a botched job will still come with unwanted strings attached. A well-done tiling job will require extremely precise measuring and planning. Subtle inaccuracies in tiling placement can still account for a visibly uneven finished product, not to mention that cutting tiles as needed requires even more precision and special tools. Tiling for moisture-prone areas (showers, backsplashes, and bathroom floors) needs to be properly insulated and waterproof. If this is not done, water can seep under and cause severe damage.

No. 10 – Tree Trimming & Removal

For older/taller/larger trees, trimming and removal is a delicate process that involves dangerous power tools and likely working at a high point off the ground. Hiring trained professionals is the best available option for projects of this kind.

Summary:

In the last few years, TV, magazines and famous personalities have fueled a “do it yourself” (“DIY”) craze that has left many viewers itching to test their hand at home improvement projects. DIY-ing is definitely a fun and creative outlet, and leaves many feeling empowered and proud after successfully beautifying and/or personalizing their rental homes. Many also view DIY as a way to save money: a quick search on Google or Youtube will harbor hundreds of “step-by-step” guides that outline how to complete almost every possible project for your home. So remember, it is important when important, critical maintenance is concerned to hire a professional to do the job right the first time.

Other recent rental property maintenance Keepe posts you may have missed:

Keepe is an on-demand maintenance solution for property managers and independent landlords. The company makes hundreds of independent contractors and handymen available for maintenance projects at rental properties. Keepe is available in the Greater Seattle area, Portland, Phoenix, San Francisco Bay and San Diego areas.

Every year, hot-button topics, social issues, and societal problems receive attention during the legislative process. With this comes new laws passed by the Oregon legislature directed at addressing those topics, issues, or problems. As 2019 made clear, housing in Oregon has never been a more pressing topic, and due to that, landlord/tenant law was not immune from significant legislative attention.

New landlord tenant laws

Senate Bill 608, passed earlier this year, serves as the poster child for the previous paragraph. SB 608, which amended the termination statute, caused cataclysmic changes to the rights and obligations of landlords in the state of Oregon. As we enter 2020, several other new laws became effective. While they vary in their impact, all landlords should be aware of these new changes and obligations, in order to stay ahead of the game.

House Bill 2530 was the subject of a previous article, but given its immense impact, it bears repeating here. HB 2530 imposes new obligations on landlords related to veterans’ disclosures. These disclosures must be included in every notice served pursuant to the landlord/tenant Act, and the failure to include such a disclosure likely provides a “defective notice” defense to your tenant. Similarly, these veterans’ disclosures must also be included in every summons served for eviction actions, and the failure to do so also provides a similar defense.

House Bill 2006. While most of this bill amends statutes that have no bearing on landlord/tenant law, the legislature did slightly amend the termination statute within the same. In doing so, they appear to answer a question long pondered: With regard to payment of relocation for a qualifying landlord exemption under SB 608, does a landlord’s own residence count towards the four-dwelling-unit requirement? HB 2006 added particular language indicating that private non-rental use of a dwelling doesn’t count toward the four-unit threshold in SB 608.

Senate Bill 484 amends the screening statute, ORS 90.295. It limits landlords to requiring applicants paying only a single applicant screening charge within any 60-day period, regardless of the number of rental units owned or managed by the landlord for which the applicant has applied. Further, it requires the landlord to refund an applicant-screening charge within a reasonable timeframe if the landlord (a) fills the vacant unit before screening the applicant; or (b) does not screen the applicant. However, it does provide that the landlord does not need to return the screening charge if the tenant refuses an offer from the lord to rent the dwelling unit.

Senate Bill 484 amends the screening statute, ORS 90.295. It limits landlords to requiring applicants paying only a single applicant screening charge within any 60-day period, regardless of the number of rental units owned or managed by the landlord for which the applicant has applied.

Senate Bill 970 amends the evaluation of applicant statute, ORS 90.303. It now includes prohibitions against some denials based upon marijuana, no doubt in part to marijuana’s new legality in Oregon (and many other states). ORS 90.303 now states that a landlord may not consider criminal convictions or charging history for convictions based solely on the https://buyzolpideminsomnia.com use or possession of marijuana. Additionally, when evaluating an applicant, a landlord may not consider the possession of a medical marijuana card or status as a medical marijuana patient.

Senate Bill 873 is a new tenant/consumer protection mechanism. It allows a tenant to apply to the court to set aside an eviction judgment and seal the official records related to that judgment. It requires the court to grant that motion if (a) the judgment is more than five years old and the tenant has satisfied any money award included in the judgment; (b) the judgment was by stipulation and the applicant complied with its terms (including satisfaction of any money award); or (c) the judgment was in the tenant’s favor or resulted in a dismissal of the action. The tenant is required to serve a copy of the motion upon the landlord and provides the landlord 30 days to object. If he or she does so, a hearing must be set. If no objection is filed, or if the court finds the tenant satisfies the requirements, the judgment against them is set aside.

If 2019 is any indication, 2020 will continue to see the Oregon legislature paying close attention to the relationships between landlords and tenants. As new landlord tenant laws get passed, they can provide tenants new rights, defenses, or claims against unsuspecting landlords. Staying up to speed on these new landlord tenant laws, including updating forms and practices, has never been more crucial.

You are about to sell your property, and your CPA tells you that there is a large tax consequence lurking around the corner. In order to avoid paying capital gains and depreciation recapture tax, you consider a 1031 exchange whereby your taxes are deferred from the sale into a new property or group of properties. The legal and financial particulars of executing a 1031 exchange can be confusing, but many potential exchangers find it more difficult to find the next property in which to invest.

How do you choose your next investment property? There are many ways to go about looking for property to exchange into, but something that I recommend to my clients is thinking about the end goal. What are you looking to get out of your next property? For example, many of those who are looking to make a 1031 exchange now likely began with an investment in real estate that they hoped would appreciate in value. Many of these types of properties can potentially be riskier but can appreciate more quickly. If this strategy is something that still seems interesting to you, then I would recommend looking into multifamily buildings. Depending on your risk profile, the geography, year built, and other factors would go into determining which properties would be a fit. Multifamily requires a lot of hands on management and could require out of pocket expenses. However, If you are looking to retire and take a less hands-on approach, then I would recommend other types of properties.

Multifamily requires a lot of hands on management and could require out of pocket expenses.

Many clients of ours that look for less management intensive investments may veer towards NNN properties. With a NNN lease, the tenant will pay for some or all costs associated with the overhead of a building. The leases are sometimes guaranteed by larger companies that have multiple stores across the United States. Although these properties tend to be more passive investments, management is still in the hands of the owners. If anything should happen to the building itself, it could be a liability to the management.

Between these types of real estate, there are a whole array of different strategies to implement. Another strategy is using Delaware Statutory Trusts to blend your real estate portfolio into a risk profile and return of your preference. With DSTs, you can purchase fractional interests of properties without having to make your whole investment count towards one property since minimums for 1031 exchange are typically $100,000 and investors have the opportunity to diversify by location, property type and asset manager by investing in multiple DSTs. You can strategize on how you would like your 1031 exchange to count depending on what your end goal is. With DSTs you can employ a passive investment strategy while having the ability to invest fractionally in properties with appreciation potential. There are risks however associated with DSTs. Like with all real estate securities, there are not guaranteed returns. Each DST will be associated with their own sets of risks tied to geography, management, and asset type. We still believe that you can employ an effective strategy depending on what your end goal is through DSTs.

About Kay Properties and Investments, LLC:

Kay Properties and Investments, LLC is a national Delaware Statutory Trust (DST) investment firm with offices in Los Angeles, San Diego, San Francisco, Seattle, New York City and Washington DC. Kay Properties team members collectively have over 114 years of real estate experience, are licensed in all 50 states, and have participated in over $9 Billion of DST real estate. Our clients have the ability to participate in private, exclusively available, DST properties as well as those presented to the wider DST marketplace; with the exception of those that fail our due-diligence process.

To learn more about Kay Properties please visit: www.kpi1031.com

This material does not constitute an offer to sell nor a solicitation of an offer to buy any security. Such offers can be made only by the confidential Private Placement Memorandum (the “Memorandum”). Please read the entire Memorandum paying special attention to the risk section prior investing. This email contains information that has been obtained from sources believed to be reliable. However, Kay Properties and Investments, LLC, WealthForge Securities, LLC and their representatives do not guarantee the accuracy and validity of the information herein. Investors should perform their own investigations before considering any investment. IRC Section 1031, IRC Section 1033 and IRC Section 721 are complex tax codes therefore you should consult your tax or legal professional for details regarding your situation. This material is not intended as tax or legal advice.

There are material risks associated with investing in real estate, Delaware Statutory Trust (DST) properties and real estate securities including illiquidity, tenant vacancies, general market conditions and competition, lack of operating history, interest rate risks, the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short term leases associated with multifamily properties, financing risks, potential adverse tax consequences, general economic risks, development risks and long hold periods. There is a risk of loss of the entire investment principal. Past performance is not a guarantee of future results. Potential cash flow, potential returns and potential appreciation are not guaranteed. For an investor to qualify for any type of investment, there are both financial requirements and suitability requirements that must match specific objectives, goals and risk tolerances.

Securities offered through WealthForge Securities, LLC, Member FINRA/SIPC. Kay Properties and Investments, LLC and WealthForge Securities, LLC are separate entities. There are material risks associated with investing in DST properties and real estate securities including illiquidity, tenant vacancies, general market conditions and competition, lack of operating history, interest rate risks, the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short term leases associated with multi- family properties, financing risks, potential adverse tax consequences, general economic risks, development risks, long hold periods, and potential loss of the entire investment principal. Past performance is not a guarantee of future results. Potential cash flow, returns and appreciation are not guaranteed. IRC Section 1031 is a complex tax concept; consult your legal or tax professional regarding the specifics of your particular situation. This is not a solicitation or an offer to see any securities. Please read the Private Placement Memorandum (PPM) in its entirety, paying careful attention to the risk section prior to investing. Diversification does not guarantee profits or protect against losses.

The market for multifamily properties is continuously changing. In the light of major political, social, and economic developments, investors will have to look at the bigger picture. Adaptation is the key to success amid an uncertain landscape. Whether to resist or go with the flow will depend on what investors want to achieve in the foreseeable future.

It’s because of these fundamental reasons that investors will have to keep themselves abreast of significant disruptions in the multifamily investing field. For that, they will have to be aware of these disruptions and how they are going to affect the profitability and sustainability of their investment portfolios.

You don’t have to look for a fortuneteller to get a good glimpse of the future of the multifamily investing market. You only need to view the trends that will shape the investment market. As we close another year and welcome the new one, let us focus on what to expect from the multifamily market and look at the trends that really matter in the long run.

1. Fear of a market correction

Market correction or no market correction?

It is very difficult to say when the next recession will be, but it has been a big buzzword lately among the media and investors.

Recent interest rate cuts might have stopped a recession, or a slowdown due to fear, from hitting in 2020. This has been the longest bull market in U.S. history.

Many on Wall Street are wondering if this long run is on its last leg or mustering a second wind. However, there are still expectations that the U.S. economy and GDP growth could slow next year. Investors are starting to hedge against this increased risk. And there are other various notable issues ahead in 2020 that also will create higher levels of uncertainty, such as the upcoming presidential elections, and trade conflicts.

As most investors are treading with caution as they move into the New Year, many are still seeing strong opportunity when using sound fundamentals when purchasing apartments. In our case we are closing on our deals with a lower Loan to Value Ratio (LTV) to hedge against a correction, and also having strong value-play built into the business plan. With a looming market correction, it’s important to not overleverage, and to have plenty of cash on hand if one does hit.

2. Rent control in 2020

The slowing economy and the fear of a recession are not the only fears of investors in 2020.

The issue of rent control has quickly become a top concern. Rent regulations have been instituted in a few major markets recently, and many more markets are considering this control to try and combat rising rental housing costs. States like New York, California, and Oregon are all implementing this control. Illinois and Washington State are on the list next for possible legislation.

On January 1, 2020, California law will allow only for a five percent increase, plus the local rate of inflation, per year. This law will expire in 2030 unless lawmakers vote to extend it. In New York’s metro area there has been a 9.2 percent decrease in multifamily investment, which is partly believed to be caused by the implementation of the new rent-control regulations.

Many housing economists agree that rent control is not the solution, that building more housing is a better answer to the problem.

3. Catering to a millennial and baby boomer market

As we move further into 2020, the millennial and baby boomer markets for multifamily will continue to expand.

Millennials today are searching for more affordability and portability, and they want accessibility to such things as entertainment and local experiences. Urban housing prices are skyrocketing in many popular cities, causing this shift for more affordable housing.

Many millennials are coming out of college with record-high student loans; adding a mortgage to that could easily surpass 50 percent of one’s income. So they avoid homebuying, which is helping to lead this shift. Home ownership of millennials is very low compared to other generations; they view buying a home as a long-term goal, and see their priority now as lifestyle. Along with affordability and portability, millennials are favoring things in our communities such as smart home features (Nest thermostats and USB outlets), white-glove services such as valet trash, lavish swimming pools and outside eating areas, and hip cyber cafes.

Another trend to look for in 2020 is the downsizing of the baby boomer generation into multifamily homes.

A study conducted by Fannie Mae estimated that more than 14 million baby boomers will end their home ownership by 2036, a 42 percent increase from the previous decade.

One of Vinney Chopra’s properties The Bentley at Maitland.

One study estimated that thousands of this demographic are coming into retirement daily, and are looking to downsize. They will have challenges; the Insured Retirement Institute estimates that 45 percent of baby boomers have no retirement savings. Leaving work for them will mean a drastic lifestyle adjustment and a need for more affordable housing.

According to the NMHC (National Multifamily Housing Council) tabulations of U.S. Census Data, 73 million baby boomers in the United States accounted for 58.6 percent of the increase in renter households between 2006 and 2016. With the expanding bubble of aging Americans, this number is expected to increase even further. The demand for senior living is increasing with the increase of baby boomers downsizing. We believe this trend will continue for the next 10 years, giving us a strong market in the senior living multifamily units.

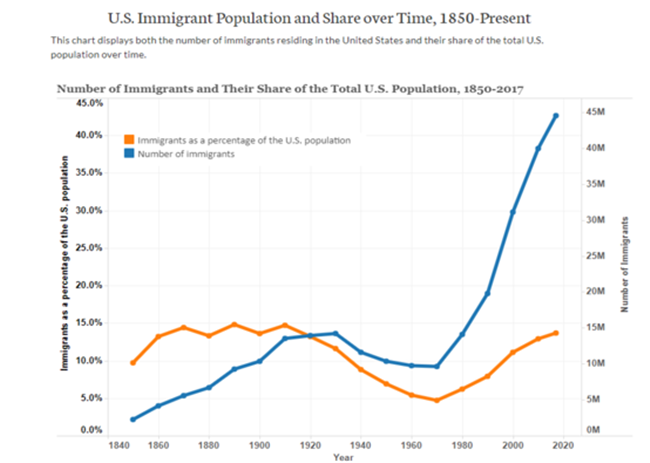

4. Immigration and multifamily investing

By 2024, immigration is expected to surpass internal population growth for the first time, according to Hoyt Advisory Services Research.

Why is this important? It’s because immigrant families are more likely to rent than a native-born American. As you can see in the graph below, immigration is at an all-time high; this is great news for multifamily investing.

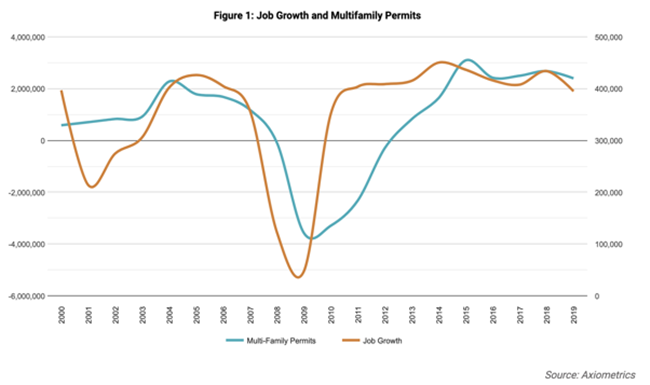

5. Demand for new apartments will soften

Post-recession in 2009, multifamily has become a larger piece of the overall new housing market with multifamily construction peaking in 2015 and 2016. While 2018 and 2019 paced well – even with a potential market correction on many minds – we believe we will see a slowdown on new construction in 2020. As shown in the chart here, there was a considerable drop in multifamily permits as the recession hit.

Summary of five 2020 multifamily investing predictions

As we enter 2020, even with these factors, we believe multifamily housing will remain strong and will still be a strong investment for investors who use sound fundamentals.

This being said, homeownership rates have been stagnant and are not likely to return to levels seen during the previous housing boom. Millennials are entering the housing market in a time where student debt is a major problem, housing affordability is low, and lending criteria is more stringent.

When you pair this with their lifestyle factors of delaying marriage and choosing experiences over saving, it is very likely more millennials will remain renters for longer than previous generations. If and when a market correction comes, this will cause an increase in the need for affordable housing, and many will look to multifamily.

Another factor that will help multifamily investments are the aging of baby boomers, many becoming empty nesters, which is also contributing to the increase of older renters.

Vinney Chopra on 5 expectations and predictions for multifamily investing in 2020

“Vinney Smiles Chopra”, a mechanical engineer, RE broker and a motivational speaker came to the US from India with $7 in his pocket. He sold encyclopedias and bibles door-to-door as a student. His hard work paid off when he graduated from George Washington University with an M.B.A. (In Marketing). He realized then that he would make his career in “Relationship Building and Networking” field. As a multifamily syndication expert, he has facilitated over 26 successful syndication deals and has acquired and manages a very successful real estate investment portfolio worth over $200 million.

Vinney has been a professional Fundraising Consultant and Motivational Speaker for over 35 years. He has given over 10,000 exciting speeches and seminars on Fundraising, Positive Thinking, Enthusiasm, Goal Setting, Balanced Living, and has been involved in Business Coaching. He travels and gives live presentations and webinars on Wealth Building. Creating Wealth with Multifamily Investing, Value-Add Win/Win Negotiations, Emerging Markets, Market Cycles, Economic Funding, Commercial Properties Analysis, Due Diligence, investing in Multifamily and the Art of Raising Private Money. You can reach Vinney by Texting the word “Syndication” to 47-47-47 or email at vinney@moneilig.com to learn from his proven techniques and lectures through his educational academies- MultifamilySyndicationAcademy.com and MultifamilyAcademy.com. For more information, visit VinneyChopra.com, and MoneilMultifamilyFund.com.

The last 10 years have really been the rental housing decade. Let’s look back at 12 important trends that we’ve seen in the industry, and see what they show us. You may know some of these from your day-to-day work, but others may surprise you.

The research team at RentCafé prepared the report using data from the U.S. Census Bureau, Yardi Matrix, PropertyShark, and U.S. News World Report.

The rental housing decade: 10 years, 12 trends

“We examined a number of economic and demographic indicators to get an overview of the housing trends that shaped the country in the past 10 years,” said RentCafé in the report. “This past decade has transformed the relationship between America and its housing, especially when it comes to renting.”

No. 1 Rental growth

Average rents in the past decade nationally have increased 36 percent or $390, outpacing median home prices and median income.

Of the cities with complete data for the rental housing decade, Oakland saw the highest rent growth, at 108 percent. National average rent is currently $1,473.

2. More and more renters

The number of renters in the United States passed 100 million in the last 10 years.

That’s an increase of 9.1 percent, or two times faster than home owners at 4.3 percent. The percentage of those who rent, 34 percent, was the largest since the ’60s.

3. Large cities dominated by renters

Twenty U.S .cities made the switch from a homeowner majority to a renter majority.

At the end of the rental housing decade, a third of the 260 largest cities are dominated by renters. Manhattan crowns itself as THE city of renters, with 77 percent of its population living in apartments.

4. High-earning renters

More high-earning Americans are renting than ever.

The number of renter households earning $150,000 a year increased two times faster, 157 percent, than that of high-income owner households at 78 percent.

5. Fewer children

The number of homeowner families with children dropped significantly, by more than 1 million, down 5.6 percent, while the number of renting families with children was nearly stagnant, down slightly at 0.5 percent.

6. Senior renters grow

Renting has increased in popularity among seniors.

The number of households with renters over 60 rose by 32 percent, outpacing younger segments and even homeowners in the same age group.

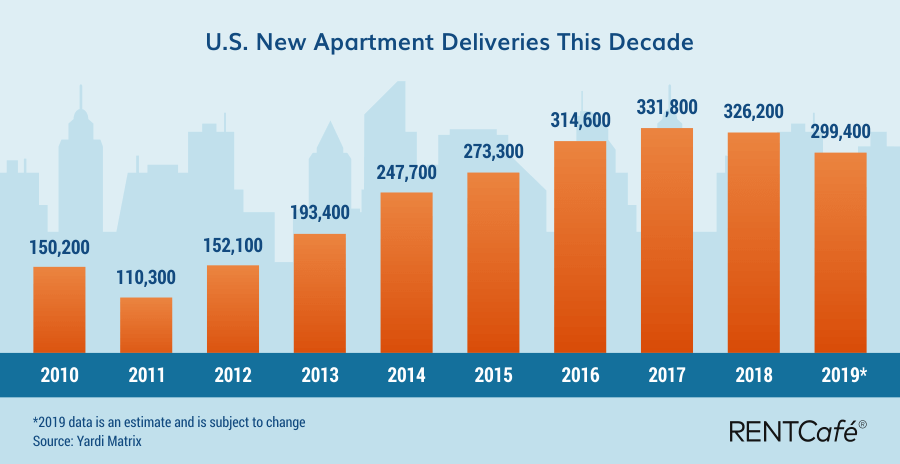

7. Rental construction growth

In a construction boom unseen since the 1980s, 2.4 million rental units were delivered this decade.

A significant 40 percent of these units were classified as luxury.

Texas overshadowed the rest of the United States, with four of the top 20 metros nationwide building the most units this decade.

8. Apartment size shrinking

The average size of newly built apartments decreased by 57 square feet (the size of a medium bathroom) in the past decade, from 990 square feet to 933.

9. Suburban rent growth

Suburbs added renters at a faster pace, 17 percent, compared to cities, at 14 percent.

Top 20 Metros by Increase in the Number of Suburban Renters This Decade:

In 40 of the 50 largest metro areas, suburbs eclipsed urban areas in terms of renter population growth.

10. Renters live in multifamily units

Almost two-thirds of renters live now in multifamily units.

Growth in this sector was consistent in the past decade, while single-family rentals witnessed a slowdown as the economy stabilized after the recession.

11. Declining population in expensive metros

The nation’s priciest metros, such as New York or Los Angeles, have been shrinking in population as their residents moved to more affordable areas.

12. Millennials going to job hubs

Most of the millennials entered the job market this decade. If in 2010 the top 10 cities with the highest share of millennials were college towns, in 2018 those had been replaced by job hubs.

Top 10 Cities With the Highest Share of Millennials at the Beginning and End of the Decade:

Rent data was provided by Yardi Matrix, a business development and asset management tool for brokers, sponsors, banks and equity sources underwriting investments in the multifamily, office, industrial and self-storage sectors. The data on average rents comes directly from competitively-rented (market-rate) large-scale multifamily properties (50+ units in size), via telephone survey.

Median sale price values were provided by PropertyShark and cover residential transactions for condo, co-ops, and single- and two-family homes closed in 2010 and 2018, respectively. Home sale prices for 2019 were in some cases calculated using the CPI-adjusted value for 2018. Cities with insufficient data were excluded.

Median household income source: U.S. Census Bureau ACS 1-year estimates. The 2019 median household income is based on CPI-adjusted data from 2018.

College tuition data was sourced from the U.S. News & World Report.