By Sebastian Moya

Associate at Kay Properties & Investments and the Kay Properties Team

One of the common topics that frequently pops up in investment conversations these days is discussion about what stage of the “cycle” the market is in. Why does cycle matter, and what does the current cycle mean for DST investment opportunities?

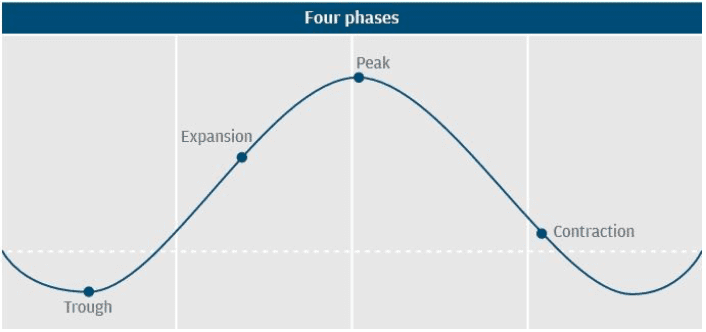

Simply put, market cycles refer to the periodic ebbs and flows that occur in the economy and across individual sectors, such as tech, energy and commercial real estate. Markets rise and fall across four phases: expansion, peak, contraction and trough.

Four stages to the cycle:

Recovery/Expansion: The market is following a healthy, positive growth trajectory.

Peak: The top of the market where assets are fully priced.

Contraction: Growth slows but isn’t negative.

Trough/Recession: Growth stalls or becomes negatives and can fall into a recession, which is usually defined as two consecutive quarters of negative growth.

Record-breaking expansion cycle

Timing investments right can help to maximize returns. Yet getting market timing exactly right is never easy unless you happen to have a crystal ball handy. There are plenty of savvy investors making educated guesses about where the market is at in its current cycle. Most are willing to wager that it is late in the expansion phase. The reality is that the current cycle has moved into uncharted territory. The U.S. is officially in its longest expansion, breaking the record of 120 months of economic growth previously occurring from March 1991 to March 2001, according to the National Bureau of Economic Research.

The length of the current economic expansion has many people worried that an inevitable end must be in sight. Yet this current period of slow and steady growth has proved to be sustainable, and there doesn’t appear to be anything imminent that could derail that pattern. The “peak” that some were worried was nearing in both the economy and commercial real estate markets could very well turn out to be more of a plateau. Even if there is a contraction or trough ahead it could be a slight downturn rather than a sharp drop off a cliff. There are numerous variables that contribute to the shape of market cycles that range from Fed monetary policy to market bubbles that pop, such as the housing and dot com booms that caused the last two recessions. Hindsight is always 20/20, but it is challenging to predict exactly what events may surface and when they will hit.

Real estate cycles vary

The added challenge in real estate is that it is not a one-size-fits-all market. Different property types and cities are at different stages of their market cycles. For example, the Manhattan office market, may be viewed by some as being close to the peak with slowing or flat growth ahead, whereas the Nashville or Orlando apartment markets could still be considered to be in the mid-stage of expansion with more upside potential.

Defense vs offense? Cyclical investing strategies

What does the current market cycle mean for DST investors? People can and do invest across all phases of the cycle. However, strategies can change depending on the phase. During expansion, investors may choose to be more aggressive as they see more upside for growth. Investors in early stage expansion cycles are more prone to play offense so to speak and are willing to take on more risk. The closer a market gets to peak and a potential down shift to a contraction or trough phase, the more likely investors are to be cautious of risk and gravitate towards defensive strategies.

In some cases, mature market cycles are fueling an increase in property sales and 1031 tax deferred exchanges. Property owners who believe values may be at or near peak see it as a good time to take chips off the table and sell real estate that has experienced good appreciation. DSTs are an accepted alternative for use in a 1031 tax-deferred exchange. Individuals also have an opportunity to reinvest proceeds into a variety of different property types and geographic markets. For example, Kay Properties has DST opportunities with a minimum investment amount of $100,000 for investors with offerings that span multifamily, student housing, self-storage, net lease (NNN), industrial and medical office properties.

About Kay Properties and www.kpi1031.com

Kay Properties is a national Delaware Statutory Trust (DST) investment firm. The www.kpi1031.com platform provides access to the marketplace of DSTs from over 25 different sponsor companies, custom DSTs only available to Kay clients, independent advice on DST sponsor companies, full due diligence and vetting on each DST (typically 20-40 DSTs) and a DST secondary market. Kay Properties team members collectively have over 115 years of real estate experience, are licensed in all 50 states, and have participated in over 15 Billion of DST 1031 investments.