The median rent in Salt Lake City fell by 0.4% over the course of August, and has now decreased by a total of 0.9% over the past 12 months, according to the September report from Apartment List.

Salt Lake City’s rent growth over the past year has is similar to both the state (-1.7%) and national averages (-0.7%).

Eight months into the year, rents in the city have risen 1.6%. This is a faster rate of growth compared to what the city was experiencing at this point last year: from January to August 2023 rents had increased 0.4%.

Rents in the city are 11.8% lower than the metro-wide median

Across the metro area, the median rent is $1,510 meaning that the median price in Salt Lake City proper ($1,333) is 11.8% lower than the price across the metro as a whole. Metro-wide annual rent growth stands at -1.5%, below the rate of rent growth within just the city.

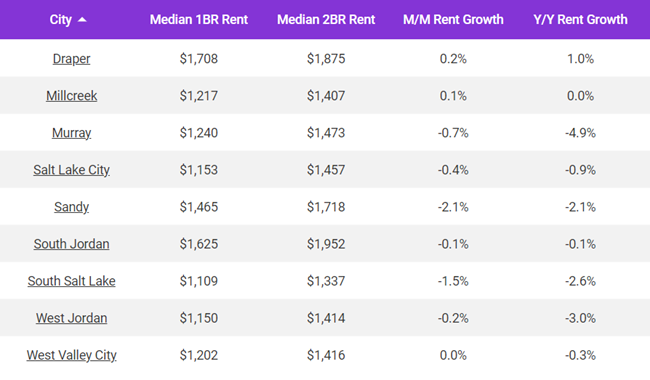

The table below shows the latest rent stats for 9 cities in the metro area that are included in the Apartment List database.

Among them, Draper is currently the most expensive, with a median rent of $1,932. South Salt Lake is the metro’s most affordable city, with a median rent of $1,270. The metro’s fastest annual rent growth is occurring in Draper (1.0%) while the slowest is in Murray (-4.9%).

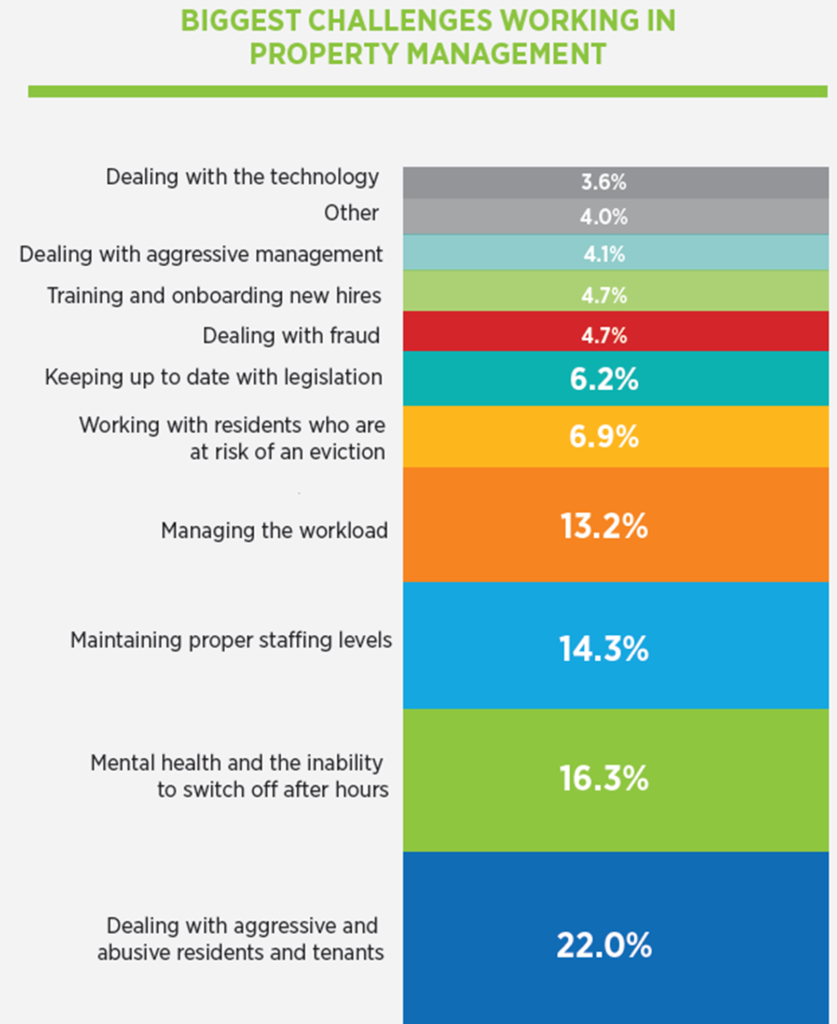

The single biggest challenge facing property managers in 2024 is dealing with aggressive or abusive tenants and residents, according to a new study from the National Apartment Association (NAA).

The “Voice of the Property Manager” NAA Research, sponsored by MRI Software, surveyed nearly 1,000 industry professionals from July 9–22. The analysis in this report represents the voices of more than 850 property managers and regional managers across the United States, a majority of whom are women.

“The most frequently cited challenges in 2024 were dealing with aggressive and abusive residents (22%) and the inability to disconnect after hours (16%). These findings indicate that confrontational interactions and the struggle to separate work from personal time are major stressors for property-management staff, potentially contributing to mental-health concerns,” the report says.

Other challenges relate to maintaining staffing levels (14%) and managing workload (13%). There were also concerns about employee retention and reinforcing the ongoing battle to balance workloads within the industry.

“Other issues such as dealing with residents at risk of eviction, inadequate communication and support from upper management, managing staff, keeping up with legislative changes and addressing fraud were cited less frequently, but still affect a notable portion of the workforce,” the report says.

Who responded to the survey?

Of those professionals surveyed, 32% were between the ages of 35-44, while another 29% were in the 45-54-year-old age group. Nearly half of respondents worked for owner/operators and 88% indicated that their companies owned or managed conventional multifamily properties. Just over half of those companies managed fewer than 5,000 units, while nearly one in five operated more than 30,000 units.

“Overall, property managers are happy in their jobs, particularly with their co-workers and with the flexibility offered to them. A slight majority have been in their current positions for more than seven years, while 22% have tenure of two years or fewer,” the report says.

About 60% feel they have the training they need to do their jobs. Nearly three-fourths expect to be in the industry three years from now, which appears to be at odds with some 39% not recommending a career in property management to their friend or colleague. See more detail on this in the full report linked at the bottom of this article.

Conclusion: Transparency And Technology

“While owners and operators should be encouraged by this year’s “Voice of the Property Manager” survey results, there is certainly room for improvement in providing a work environment that will not only retain existing employees, but create more promoters of the industry, potentially helping with recruiting efforts as well.

“Managing workloads, maintaining proper staffing levels and providing tools and resources that help property managers do their jobs more effectively will go a long way in improving work-life balance,” the report says.

When it comes to technology, transparency is important as “open communications, and change management will be key as the industry continues to embrace technology, which stands to disrupt operations, roles and responsibilities all while remaining a people-first business.”

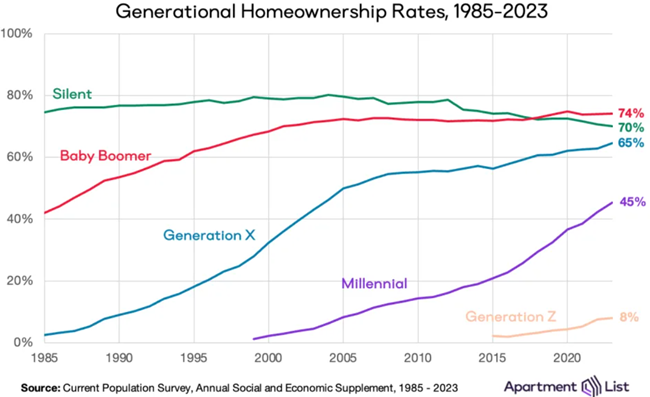

Millennials are the nation’s largest generation, and by sheer volume they are purchasing more homes than any other group, Apartment List research reports.

The Census Bureau even credits them with driving a recent upward trend in homeownership nationwide. But despite some positive trends recently, long-term data show millennials remain well-behind previous generations when it comes to owning homes. (Millennials were born from 1981-1996, making them 28 to 43 today. Those in Generation Z were born from 1997-2012, making them 12 to 27 years old today.)

Much of the reason for the lag in millennial home ownership is tied to the 2008 housing market collapse, which happened right as they were entering the work force.

Also, when the economy recovered, and many millennials were drawn to jobs in centrally-located cities, some found that renting apartments made more financial sense than buying starter homes that were becoming increasingly scarce and expensive.

Some research points:

Millennial homeownership is growing slower than that of previous generations.

Millennials are finding the most success in smaller, Midwestern housing markets.

Millennials in large metros are less likely to own homes.

Gen Z homeownership is keeping pace with millennials, for now.

Gen Z and millennials are living with their parents longer.

As millennials grapple with the housing market into their 40s, the next generation is also getting old enough to start buying homes. As of 2023, 8 percent of Gen Z adults own a home, and so far, their homeownership rate is trending in line with millennials through their mid-20s.

What does this mean for the future?

“We’re already seeing the housing market adapt to these homeownership trends. Anticipating that millennials and Gen Z’ers will still want to live in single-family homes even if they can’t afford to buy them, the “built-for-rent” sector is booming.

“Nearly one in 10 new single-family homes in 2023 were built to be rented instead of owned. Similarly, the past year has seen a flood of new multifamily units hit the market, which has helped moderate the cost of renting relative to owning.

“One source of optimism for Generation Z and prospective first-time homebuyers is that the housing market is finally drawing widespread attention from policymakers, at every level of government,” writes Rob Warnock, senior research associate at Apartment List, in the report.

In my experience, most of these items are small inconveniences that landlords and tenants work out between themselves without the need for attorneys like me.

Tenants may make unreasonable demands over maintenance issues asking for compensation or damages so landlords need to know the law.

The landlord/tenant relationship naturally has its ups and downs. Anyone who has ever lived in a house knows how things inevitably break down, need repairs, and/or require fixing.

In my experience, most of these items are small inconveniences that landlords and tenants work out between themselves without the need for attorneys like me. Occasionally, I have seen tenants make unreasonable demands for rent credits, damages, and other monetary claims for the smallest of inconveniences—if they can be called that.

Fortunately, much of these demands can be pushed back upon, if the landlord has knowledge of the law and their legal obligations.

As an initial matter, Oregon landlords are required to provide habitable housing consistent with ORS 90.320, which is commonly known as the “landlord duties” statute. If the premises “substantially lacks” any of the items set forth within that statute, then a tenant may have a claim for diminution of rent. On that point, it is important for both tenants and landlords to understand that diminution does not immediately mean “a month of rent.”

Diminution of rent is often discussed as a percentage of diminution—i.e., how much of the premises is diminished—or how much of the daily rent should be discounted based upon said diminution. An old case practitioner’s reference for this point is Lane v. Kelley. Additionally, diminution of rent is only discussed in terms of the stated monthly rent, and no more. The case to review for this point is L&M Investments v. Morrison.

These two cases inform the basis of legal analysis as to damages that may or may not be owed to a tenant for a particular issue. It goes without saying that any maintenance issue should be remedied as quickly as possible to avoid triggering any demands for compensation or damages. However, that’s not always attainable or avoidable.

For example a maintenance issue. Assume that a tenant’s bathroom—one of two they have in the premises—was out of commission for a week. Because the property has multiple bathrooms, the premises may not “substantially lack” what is required under ORS 90.320 at all. Even if it does, it would certainly be an appropriate argument that the premises was not diminished by 100% of the rental amount. However, even assuming that it was diminished by 100%, the tenant would not be entitled to any diminution of rent beyond one week (as that’s the amount of time it took to remedy the issue).

Additional issues can arise when substitute housing is brought up. ORS 90.365 discusses substitute housing, which is required if the landlord “intentionally or negligently fails to supply any essential service.”

After a notice period and allowing the landlord “a reasonable time and reasonable access under the circumstances to supply the essential service,” the tenant may procure substitute housing if the dwelling unit is unsafe or unfit to occupy. This provision is not triggered under the following circumstances:

(a) The landlord substantially supplies the essential service; or

(b) The landlord is making a reasonable and good-faith effort to supply the essential service and the failure is due to conditions beyond the landlord’s control; or

(6) …. if the condition was caused by the deliberate or negligent act or omission of the tenant or a person on the premises with the tenant’s consent.

If substitute housing is required for some reason, then it behooves the landlord to control the substitute-housing cost by either offering the tenant a vacant unit in the complex/property, if available, or by procuring an extended-stay hotel with kitchen facilities in the area.

If that doesn’t happen, and tenants are left to their own devices, it is not uncommon for tenants to book Airbnbs and seek to recover those costs from landlords. While the statutes contain some pushback for such actions, litigation that often comes after substitute-housing demands will cause costs to skyrocket beyond the costs of that Airbnb.

Habitability issues are no fun.

Things like acts of God that displace tenants—which, in my opinion, are not the fault of landlords, despite what other narratives exist—often arise and sour the landlord/tenant relationship beyond repair. While that likely cannot be stopped, positioning yourself to mitigate costs and expense associated with such things requires knowledge of the laws, rules, and cases that control the analysis.

Brad Kraus, Warren Allen LLP

About the author:

Bradley S. Kraus is an attorney and partner at Warren Allen LLP. His primary practice area is landlord/tenant law, but he also assists clients with various litigation matters, probate matters, real estate disputes, and family law matters. You can reach him at [email protected] or at 503-255-8795.

Multifamily is awaiting the news of the September rate cut with “hope that lower rates will break the logjam in the transactions market and spur refinancing activity,” Yardi Matrix says in the August report.

However, the rate cut also presages a slower growing economy. For example, rents in August stopped growing in most places except the Midwest and are likely to trend lower in coming months.

Some highlights of the report

The multifamily market’s run of rent gains ended in August, as seasonality and the high number of deliveries in the Sun Belt served to mute growth. The average U.S. advertised rent fell by $1 in August to $1,741, while year-over-year growth was unchanged at 0.8%.

Despite the end of the six-month streak of positive rent growth, the news was not all bad. Demand continues to hold up, keeping the national occupancy rate unchanged at 94.7% in the face of rapid supply growth.

Single-family rental rents hit a bump in August, with advertised rents falling $7 nationally to$2,164. The year-over-year growth rate dropped 40 basis points to 0.7%. The national occupancy rate fell 10 basis points to 95.3% in July.

Change is brewing

The coming changes are likely to be incremental rather than drastic, the report says.

“Lower rates will be a relief to multifamily, potentially unlocking asset sales and refinancings, while reducing the pressure on properties that are underwater on their mortgages.

“The flip side of rate relief, however, is that it is a result of the economy slowing,” the report says.

The slowing jobs market is also a point of concern.

“The declining quits rate and weakness in office-using job growth are other signs of slowing, which could turn into a drag on consumers and apartment demand,” the report says.

Yardi Matrix researches and reports on multifamily, office and self-storage properties across the United States, serving the needs of a variety of industry professionals. Yardi Matrix Multifamily provides accurate data on 18+ million units, covering more than 90 percent of the U.S. population. Contact the company at (480) 663-1149.

The Consumer Financial Protection Bureau (CFPB) has received more than 1,700 complaints about rental-debt collection, according to a new report, and has been taking action against debt collectors.

The report says that in the United States, rental debt is estimated to be more than $9 billion, with more than 4.5 million households behind on rent payments.

Rental-debt collectors often charge renters collection fees in addition to the unpaid rent itself. As the CFPB has observed with medical debt, many debt collectors furnish rental debt to credit-reporting companies as a means of collecting debt through coercion.

The complaints submitted by consumers and the CFPB’s own research show that the infusion of consumer financial products and services into the rental market raises risks for renters, including improper debt collection due to:

Illegal price-fixing: Law enforcement officials in several states as well as individual renters have alleged that rapid increases in rent have been driven by illegal price-fixing. Landlords and management companies may have used “revenue-management software” to collect improper amounts that ultimately end up in debt collection. Debt collectors collecting on bills that are inflated due to illegal price-fixing may be violating the Fair Debt Collection Practices Act.

Tacked-on rental fees: Renters, as well as landlords, have complained to the CFPB about rental junk fees, including fees from rental-payment processing services that are added onto and required as a condition for rent payment. It is often not clear whether these fees are allowed under the lease agreement or local law, and, thus, able to be targeted by debt collectors.

Consumer Financial Protection Bureau Actions

The CFPB is taking steps to ensure that debt collectors follow consumer financial protection laws, including the Fair Debt Collection Practices Act and the Fair Credit Reporting Act.

The CFPB also has brought enforcement actions against debt collectors for their efforts to collect on unsubstantiated debt, unlawfully threatening legal action against consumers, and other violations.

What is the best software for rental property management is the question this week for Ask Landlord Hank. Remember Hank is not an attorney and is not offering legal advice – always check your local and state laws. If you have a question for him please fill out the form below.

Dear Landlord Hank,

What’s the best rental property management software for a person who has 51 units?

I have built this portfolio over the last 13 years and have been using a property manager. I am exploring options to bring management in-house if it makes financial sense.

-Chad

Hi, Landlord Chad,

At one time I personally owned about 50 units and had no problem keeping up with everything easily without a property-management software package.

Now, since I own a property management and leasing company and we have a few hundred rentals and have to deal with owners and tenants, we have been using AppFolio for about 10 years.

It is a good platform, but not cheap, and it has some drawbacks. There are others out there as well and I’d thoroughly check them out too before deciding.

Sincerely,

Landlord Hank says, “At one time I personally owned about 50 units and had no problem keeping up with everything easily without a property-management software package.”

Hank Rossi

Each week I answer questions from landlords and property managers across the country in my “Dear Landlord Hank” blog in the digital magazine Rental Housing Journal. https://rentalhousingjournal.com/asklandlordhank/

Ask Landlord Hank Your Question

Ask veteran landlord and property manager Hank Rossi your questions from tenant screening to leases to pets and more! He provides answers each week to landlords.

“I started in real estate as a child watching my father take care of our family rentals- maintenance, tenant relations, etc , in small town Ohio. As I grew, I was occasionally Dad’s assistant. In the mid-90s I decided to get into the rental business on my own, as a sideline. In 2001, I retired from my profession and only managed my own investments, for the next 10 years. Six years ago, my sister, working as a rental agent/property manager in Sarasota, Florida convinced me to try the Florida lifestyle. I gave it a try and never looked back. A few years ago we started our own real estate brokerage. We focus on property management and leasing. I continue to manage my real estate portfolio here in Florida and Atlanta. “ Visit Hank’s website here.

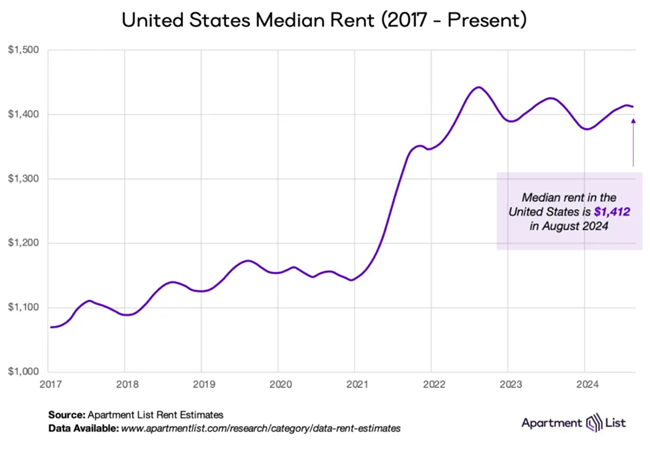

National rents fell 0.1% in August signaling the end of the rental market’s typical busy season, according to the September report from Apartment List.

The median national rent is now $1,412. In August, 59 of the nation’s 100 largest cities saw rents fall.

This is the second consecutive summer of modest rent growth, “as the market remains sluggish thanks to a windfall of new supply. If historical trends hold, rents will continue to fall on a monthly basis for the remainder of the year,” the Apartment List research team writes in the report.

In the fall, fewer households tend to move when school resumes and temperatures cool.

The report says that apartments are on average slightly cheaper today than they were one year ago.

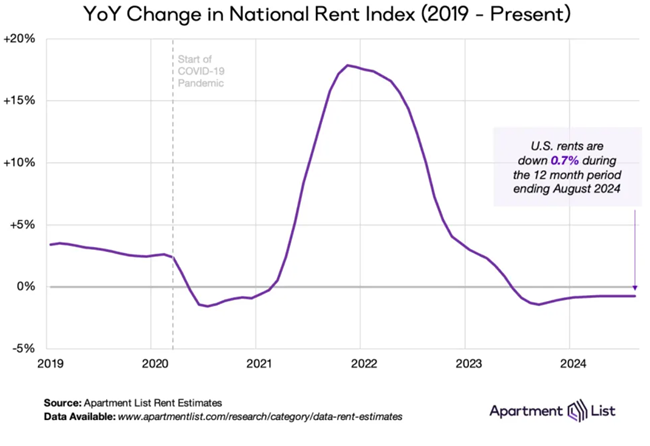

Year-over-year rent growth is -0.7 percent and “has now been in negative territory for over a full year. Despite this, the national median rent is still more than $200 per month higher than it was just a few years ago,” the report says.

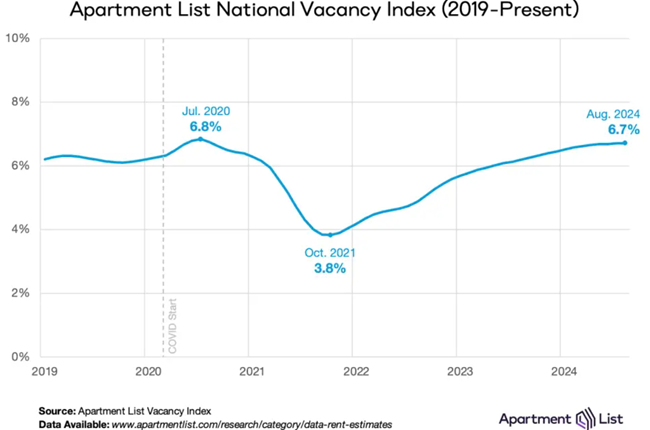

Vacancy Index continues elevated

Through August the Apartment List vacancy index sits at 6.7 percent, the highest reading since August 2020.

“And there’s good reason to expect that it could rise even further during the remainder of the year,” the report says. “This means that renters should have more available options than they have had in some time, especially in the Sun Belt markets where construction activity has been strongest.”

Report Summary

The report concludes that with August’s 0.1% decrease, the busy season is officially over and rents will continue to fall for the remainder of the year.

“Year-over-year rent growth also indicates a sluggish market, remaining negative at -0.7 percent. Rent increases are currently being moderated by a robust construction pipeline expected to deliver a decades-high number of new apartment units in 2024.

“Improving consumer sentiment about broader macroeconomic conditions seems to have driven a rebound in rental demand this year, but that bounce back has so far been outweighed by the impact of incoming supply. And recent signals of labor market softness could dampen demand going forward,” says the Apartment List research team in the report.

Freddie Mac and Fannie Mae have announced new tenant protections for residents in multifamily properties with mortgages backed by the two Government-Sponsored Enterprises (GSEs), according to a release from the Federal Housing Finance Agency (FHFA).

The new multifamily lease standards policy requirement starting February 28, 2028 will require borrowers with new Enterprise-backed financing to provide residential tenants the following three minimum standards which will be included in all residential leases at properties for which applications for new loans are signed on or after the effective date.

The new multifamily least standards are:

30-Day Notice of Rent Increases: Written notice of a rent increase at least 30 calendar days prior to said increase;

30-Day Notice of Lease Expiration: Written notice of the scheduled expiration of the residential lease at least 30 calendar days prior to said expiration;

5-Day Grace Period for Late Rent Payments: A minimum five calendar day period from the rent due date before late fees or other penalties can be charged, e.g., if rent is due on the 1st day of the month, a late fee cannot be charged until the 6th day of the month if rent is still unpaid.

“Fannie Mae and Freddie Mac’s (GSEs) announcements today of new multifamily tenant protections mark an important milestone by increasing transparency and improving communication between housing providers and tenants,” said FHFA Director Sandra L. Thompson.

In 2023, Fannie Mae financed approximately 482,000 units of multifamily rental housing, a significant majority of which were affordable to households earning at or below 120% of area median income, according to Mortgage Point.

“These lease standards seek to extend the reach of common baseline tenant protections,” said Kevin Palmer, Head of Multifamily for Freddie Mac. “Although many borrowers already exceed these minimum standards, all will be required to meet the standards to obtain GSE financing in the future. The details we released are intended to give lenders, borrowers, and other market participants clearer expectations with regard to how we will implement, monitor, and enforce the new requirement.”

What is decent monthly cash for for a rental property for a real estate investor is the question this week for Ask Landlord Hank. Remember Hank is not an attorney and cannot offer legal advice. If you have a question for him please fill out the form below.

Dear Landlord Hank:

What is a decent monthly cash flow on an investment home for rental?

-Mitchell

Dear Landlord Mitchell,

That is a tough/easy question and very individual.

Your face can tell you the answer after you do a little homework. If you are considering a property as a rental investment, determine your fixed expenses every month and think of EVERYTHING – this is critical, so go over this list until you have it all and then check it again:

Mortgage if you will have one

Taxes

Insurance

HOA fees

Reserve

Landscaping

Pest control

Management

Add all those up and then determine the rental rate.

Are you going for an annual tenant or are you going short-term?

Annual is slow and steady; short-term can generate more cash flow income, but it’s more work and less steady.

After you do all your calculations and you see the monthly profit, are you smiling or are you worried?

If you aren’t smiling, this is not the investment for you. Sometimes the market is too high and you can’t find a property that makes sense financially.

Keep looking and hold on for the right property. Keep doing your homework, and make sure you know the value that you are looking for.

To me, buying a rental property is like looking for treasure. If it was easy to find, everyone would be doing it. Rental properties are my favorite investment. It took me a year of looking to find my first one.

I had a wonderful broker that really knew value and he took me around and showed me properties so I could see and learn for myself.

I’ve had stocks and bonds, T-bills and CDs, and used to trade commodities (no bitcoin) – and real estate is my mainstay and true love. Make sure you always have needed insurance, a reserve to cover unforeseen and costly expenses (new HVAC, etc.), and do thorough background screening on all tenants.

Sincerely,

Landlord Hank says, “Keep looking and hold on for the right property. Keep doing your homework, and make sure you know the value that you are looking for.”

Hank Rossi

Each week I answer questions from landlords and property managers across the country in my “Dear Landlord Hank” blog in the digital magazine Rental Housing Journal. https://rentalhousingjournal.com/asklandlordhank/

Ask Landlord Hank Your Question

Ask veteran landlord and property manager Hank Rossi your questions from tenant screening to leases to pets and more! He provides answers each week to landlords.

“I started in real estate as a child watching my father take care of our family rentals- maintenance, tenant relations, etc , in small town Ohio. As I grew, I was occasionally Dad’s assistant. In the mid-90s I decided to get into the rental business on my own, as a sideline. In 2001, I retired from my profession and only managed my own investments, for the next 10 years. Six years ago, my sister, working as a rental agent/property manager in Sarasota, Florida convinced me to try the Florida lifestyle. I gave it a try and never looked back. A few years ago we started our own real estate brokerage. We focus on property management and leasing. I continue to manage my real estate portfolio here in Florida and Atlanta. “ Visit Hank’s website here.