Whether you are a first-time investor or an existing apartment owner, here are the top six things to remember before buying an apartment building, according to Carlos Azucena, founder of CFA Property Advisors of Marcus & Millichap.

Azucena, who focuses on small and mid-sized apartments, said in a release that investment in multifamily properties continues to be one of the most attractive plays in today’s real estate market. So, he provides this checklist to potential investors.

1. Understand the market you’re investing in

Before deciding to make a considerable investment in an apartment building, it is important to understand what makes the area great (or not so great), and there is some basic information that can help you do that. Having a good understanding of market vacancy, current asking rents, and today’s interest rates will give you a good snapshot of what you are immediately facing were you to invest today. To understand future potential, know what drives employment in the area, what inventory is in the development pipeline, and how market rents are performing. These items and others can give you clues as to how your investment will perform in the future.

2. Know what factors affect your specific location

Knowing what factors play into the desirability of your specific location will give you an idea if you will be able to easily find renters and how high you can push your asking rents. For example, as traffic has worsened in many regions, public transit has become more important as renters look for ways to avoid long commutes.

Questions you can ask yourself are, “Is the property near public transportation or does it have easy access to freeways?

What is the tenant profile and why would renters want to live here? Is it close to their work or school?

What kinds of amenities are available to them – retail, outdoor recreation, dining, and nightlife?”

3. Do your due diligence

Once your offer is accepted but before you complete your purchase, do your due diligence to understand the condition of the property and to make sure the books and records are in order. In commercial apartment sales (5 units+) unlike residential apartments (2-4 units), the seller is not required to provide a set of detailed disclosures although they are required to disclose any material facts. Your due diligence should at minimum include a full property and termite inspection on the physical side. Regarding books and records, a thorough review of all the leases, income/expense statements, natural hazard disclosure report and preliminary title report are among the critical items for your review.

4. Know the lending environment

Real estate is one of the few investments where you can readily secure large amounts of money from a lender to aid you in your purchase. Having a good lender on your team can either make or break your next purchase. It is important for you to identify the type of loan that best suits your need and what the lender’s requirements are. What type of lender should you go to – a portfolio or agency lender? Would you prefer a residential apartment loan or a commercial apartment loan? What are interest rates for a 5-, 7- or 10-year terms? Does it make sense to go interest only for a few years to have extra capital for improvements or a higher cash-on-cash yield?

5. Decide what is most important to you – cash flow, appreciation, tax shelter or all the above

Each type of real estate whether it be apartments, retail, office, land, etc., have their own pros and cons. In many instances that includes whether the property is more of a cash flow producing asset or if the value is more likely to be derived from appreciation. Apartments in tier one markets tend to provide the lowest initial cash-on-cash returns but often offer the promise if accelerated appreciation. If you are looking for more substantial cash flow from day one, perhaps looking at tier two and tier three markets may be a better fit.

6. Find a specialized agent

Finding an agent that specializes in apartment sales that can help educate you on all the factors above is critical to your success. Consider them part of your real estate network. A network that should include accountants, real estate attorneys, handymen, money lenders, professional property managers and even other real estate investors. A good, seasoned agent can be an invaluable resource by helping you develop your network and also educating you on current market conditions and location pros and cons.

About the author:

Since 2005, Carlos Azucena has worked in commercial real estate specializing in the sale of multifamily investments throughout the San Francisco Bay Area. He joined Marcus & Millichap and participated in the successful sale of over $2 billion worth of real estate in the early part of his career. During that time, he specialized in the sale, marketing, and analysis of apartment buildings over 100 units for some of the region’s largest private and public investors including real estate investment trusts (REITs), sponsorships, private equity groups and some of the most influential developers in the area. It was his goal to take his experience from a highly competitive and sophisticated arena and share that with all apartment investors, regardless of the size of their portfolio.

The personal and professional lives of the average person are now often intertwined in today’s busy world so how does this trend affect apartment amenities?

By Holly Welles

With the rising popularity of telecommuting, the living space and the workspace are beginning to blend, phasing out the familiar nine-to-five. Needless to say, it’s crucial to keep current with these trends.

Naturally, potential tenants are searching for properties that support all aspects of their lifestyle. This includes their work, and since that definition is evolving, apartment amenities have to change as well. Adaptation is one of the key factors behind continued success.

With that in mind, how should property managers approach the subject of their amenities? Which workforce trends should they consider when planning improvements for their multifamily properties?

It isn’t always such a simple subject, especially with the limitations of a strict budget.

Regardless, it’s possible to attract a greater number of tenants and increase occupancy rates with only a few adjustments. Many of them are comparatively inexpensive when compared to other renovations. What are the best modifications, and how can a property manager make room for them?

High-Speed Internet Connection

More people are remaining at home over the course of their workday, sending emails, completing projects and fulfilling their responsibilities from the comfort of their home. Internet connectivity has made this possible.

Property managers can enhance that connectivity with an investment in high-speed internet. While their existing infrastructure no doubt supports an internet connection already, they can take additional measures to ensure it’s strong and reliable. That said, an upgrade may prove expensive.

Given the cost of a multiunit wi-fi network, property managers with the means might decide to offer it for free as an attractive competitive advantage. As they enjoy the benefits of this change, they can research the potential of 5G networks, which are likely to lead to new developments in wireless infrastructure.

Flexible Community Spaces

Telecommuters will want a work-friendly area outside their apartments where they can congregate with other residents. Though they can manage their responsibilities without leaving their apartments, a little variation is appealing. Sitting at the same workstation day after day can start to feel stale.

Taking this into account, potential tenants will prioritize a multifamily property with a flexible community space. The fact that 43 percent of Americans spent time working remotely last year only reinforces the value of this amenity. It’ll continue to increase in relevance, moving through 2019 into the next decade.

Of course, creating a new community space can cost a substantial amount of money — but property managers don’t have to invest in large-scale renovations. They should evaluate their properties and see how they might adjust or rearrange an existing room to make it more accommodating for remote workers.

Package Delivery Service

In the past, property managers handled packages for their tenants, an obligation that is unsustainable as the number of home deliveries increases.

Fortunately, the installation of package lockers has alleviated much of the burden. They differ in their capabilities, depending on the quality of the technology, from a basic setup to a more complex smart locker. These storage alternatives send a text message and email with a code when a tenant receives a package.

While these smart lockers aren’t a mandatory addition, they’re an attractive amenity for tech-savvy tenants and an incredible convenience for property managers. The latter should assess their budgets and research their available options, setting aside time to review other trends relevant to their bottom line.

Apartment Amenities of the Future

Property managers should acknowledge the changing integration of life and work with the amenities above, investing in the features that attract and retain today’s telecommuting tenants. They’ll likely represent a large majority of tomorrow’s workforce.

It’s critical to keep current with the latest technologies and modifications. Whether a property manager decides to invest in an update to their internet connectivity, flexible community spaces or a smart locker, they can feel confident knowing they’ve made a change with widespread appeal.

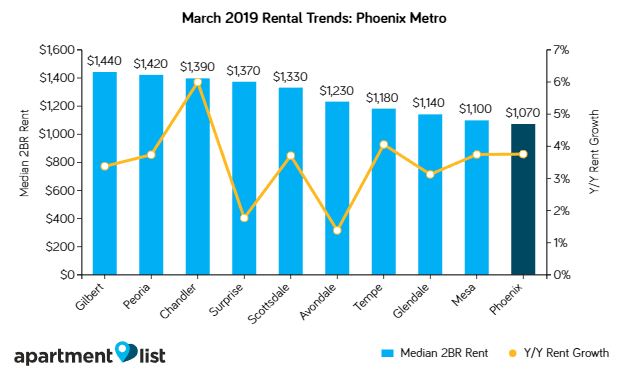

Phoenix rents have increased 0.5% over the past month, and have increased moderately by 3.7% in comparison to the same time last year, according to the latest report from Apartment List.

Currently, median rents in Phoenix stand at $860 for a one-bedroom apartment and $1,070 for a two-bedroom.

The city’s rents have been increasing for 16 straight months – the last time rents declined was in November 2017. Phoenix’s year-over-year rent growth leads the state average of 3.1%, as well as the national average of 1.3%.

East Valley Rents Report

Throughout the past year, rent increases have been occurring not just in the city of Phoenix, but across the entire metro.

Of the largest 10 cities that Apartment List has data for in the Phoenix metro, all of them have seen prices rise.

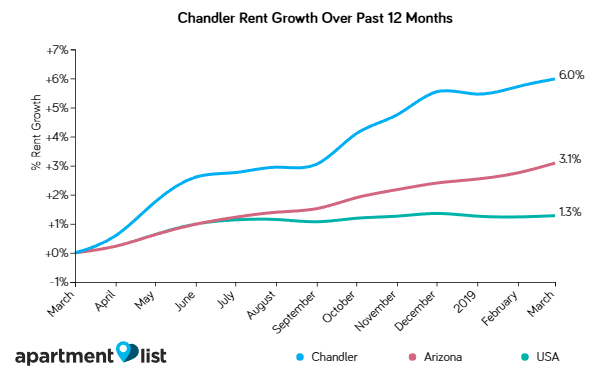

Chandler has seen fastest rent growth in Phoenix metro

Chandler rents have increased 0.2% over the past month, and are up sharply by 6.0% in comparison to the same time last year.

Currently, median rents in Chandler stand at $1,120 for a one-bedroom apartment and $1,390 for a two-bedroom. This is the second straight month that the city has seen rent increases after a decline in January. Chandler’s year-over-year rent growth leads the state average of 3.1%, as well as the national average of 1.3%.

Gilbert rents decline slightly

In Gilbert, rents have declined 0.9% over the past month, but have increased moderately by 3.4% in comparison to the same time last year. Gilbert is still the most expensive city for rents.

Currently, median rents in Gilbert stand at $1,160 for a one-bedroom apartment and $1,440 for a two-bedroom. This is the third straight month that the city has seen rent decreases after an increase in December of last year. Gilbert’s year-over-year rent growth leads the state average of 3.1%, as well as the national average of 1.3%.

Mesa rents continue upward trend

Mesa rents have increased 0.6% over the past month, and have increased moderately by 3.7% in comparison to the same time last year.

Currently, median rents in Mesa stand at $880 for a one-bedroom apartment and $1,100 for a two-bedroom. The city’s rents have been increasing for 16 straight months – the last time rents declined was in November 2017. Mesa’s year-over-year rent growth leads the state average of 3.1%, as well as the national average of 1.3%.

Scottsdale rents continue climbing for 16 straight months

Scottsdale rents have increased 0.3% over the past month, and are up moderately by 3.7% in comparison to the same time last year.

Currently, median rents in Scottsdale stand at $1,070 for a one-bedroom apartment and $1,330 for a two-bedroom.

The city’s rents have been increasing for 16 straight months – the last time rents declined was in November 2017. Scottsdale’s year-over-year rent growth leads the state average of 3.1%, as well as the national average of 1.3%.

Tempe rents up 4 percent over same time last year

Tempe rents have increased 0.8% over the past month, and have increased significantly by 4.0% in comparison to the same time last year.

Currently, median rents in Tempe stand at $950 for a one-bedroom apartment and $1,180 for a two-bedroom. This is the third straight month that the city has seen rent increases after a decline in December of last year. Tempe’s year-over-year rent growth leads the state average of 3.1%, as well as the national average of 1.3%

West Valley Rents Report

Glendale rents

Glendale rents have increased 0.5% over the past month, and have increased moderately by 3.1% in comparison to the same time last year.

Currently, median rents in Glendale stand at $910 for a one-bedroom apartment and $1,140 for a two-bedroom. This is the third straight month that the city has seen rent increases after a decline in December of last year. Glendale’s year-over-year rent growth is on par with the state average of 3.1%, but exceeds the national average of 1.3%.

Peoria rents up moderately compared to last year

Peoria rents have increased 0.4% over the past month, and are up moderately by 3.7% in comparison to the same time last year.

Currently, median rents in Peoria stand at $1,140 for a one-bedroom apartment and $1,420 for a two-bedroom. The city’s rents have been increasing for 16 straight months – the last time rents declined was in November 2017. Peoria’s year-over-year rent growth leads the state average of 3.1%, as well as the national average of 1.3%.

Avondale rents lag state average

Avondale rents have increased 0.2% over the past month, and have increased slightly by 1.4% in comparison to the same time last year.

Currently, median rents in Avondale stand at $990 for a one-bedroom apartment and $1,230 for a two-bedroom. This is the second straight month that the city has seen rent increases after a decline in January. Avondale’s year-over-year rent growth lags the state average of 3.1%, but exceeds the national average of 1.3%.

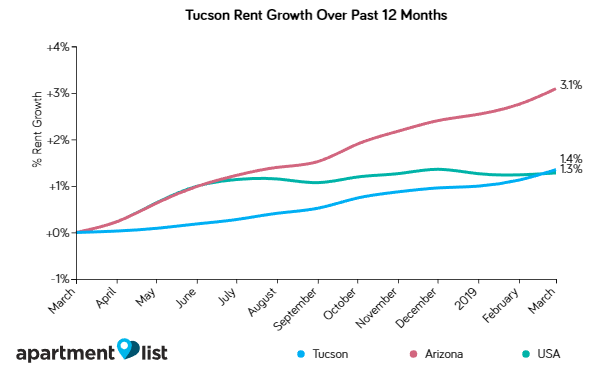

Tucson rents increase for 33 straight months

Tucson rents have increased 0.2% over the past month, and have increased slightly by 1.4% in comparison to the same time last year.

Currently, median rents in Tucson stand at $710 for a one-bedroom apartment and $940 for a two-bedroom. The city’s rents have been increasing for 33 straight months – the last time rents declined was in June 2016.

Tucson’s year-over-year rent growth lags the state average of 3.1%, but exceeds the national average of 1.3%.

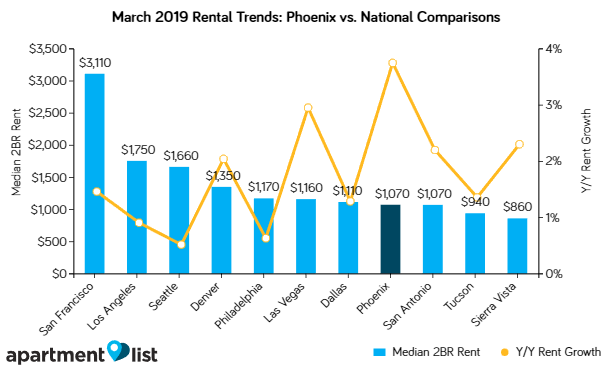

Phoenix rents still more affordable than many cities

As rents have increased moderately in Phoenix, a few similar cities nationwide have also seen rents grow modestly. Phoenix is still more affordable than most comparable cities across the country.

Rents increased slightly in other cities across the state, with Arizona as a whole logging rent growth of 3.1% over the past year. For example, rents have grown by 1.4% in Tucson.

Phoenix’s median two-bedroom rent of $1,070 is below the national average of $1,170. Nationwide, rents have grown by 1.3% over the past year compared to the 3.7% increase in Phoenix.

While Phoenix’s rents rose moderately over the past year, many cities nationwide also saw increases, including Las Vegas (+2.9%), San Antonio (+2.2%), and Denver (+2.0%).

Renters will find more reasonable prices in Phoenix than most other large cities. For example, San Francisco has a median 2BR rent of $3,110, which is more than two-and-a-half times the price in Phoenix.

Methodology

Data from private listing sites, including our own, tends to skew towards luxury apartments, introducing sample bias. In order to address these limitations and provide the most accurate rent estimates available, we now start with reliable median rent statistics from the Census Bureau, then extrapolate forward based on our own rental listing data, using a same-unit analysis similar to Case-Shiller’s approach, which compares only units that are available across both time periods to provide an accurate picture of rent growth in cities across the country.

Apartment List

Apartment List is a growing online apartment rental marketplace on a mission to make finding a home an easy and delightful process.

The changing role of the property manager today requires more and more knowledge of ever-changing local city ordinances, state laws and federal rules.

By John Triplett

When Enrique Jevons started as a property manager years ago, he often acted as both a property manager and a handyman. But the changing role of the property manager today is different, especially in his hometown of Seattle.

As the former head of Jevons Property Management, recently acquired by Mynd Property Management, he sees the role of the property manager in Seattle changing these days. Jevons says the environment makes him feel like he also has to take on some of the responsibilities typically handled by an attorney (he is not an attorney only an advisor), given the constantly shifting government regulatory environment at the city, state and national levels.

Going forward, Jevons’ company will be known as Mynd Property Management, which “brings a best-in-class service to the Washington market in partnership with the Jevons team,” said Doug Brien, (pictured above right) CEO and co-founder of Mynd with Colin Wiel above, in an interview with Rental Housing Journal. Mynd focuses on the “small residential” sector, which includes single-family rentals and multifamily properties with up to 50 units.

“Seattle has been very noteworthy lately in terms of rent growth, investment and new construction of multifamily residences,” said Brien. “We are excited to have a presence there and to be working with Enrique.

Doug Brien, co-founder of Mynd says, ““One of the things that we’re fanatical about, and that’s different about us, is we try to expose as much useful data as possible to our owners.”

“At Mynd, we’re all real estate investors at heart, and Enrique is an investor who knows the Seattle market really well,” Brien said.

How to bring more value to the changing role of the property manager

To address inefficiencies in an industry that has existed for a long time, Mynd co-founders Brien and Colin Wiel, applied technology to property management. Seattle property owners and residents will now benefit from this technology deployed by Mynd, Brien said.

“One of the things that we’re fanatical about, and that’s different about us, is we try to expose as much useful data as possible to our owners, so they can access real-time data, not a statement from 30 days ago, for instance.

“If you have a vacant unit, you can see in real-time how many leads, how many applicants, how many showings it’s had. That tells the story of how your unit’s doing,” Brian said. Plus, owners can pull out their phone and use their mobile app to find out what’s going on with their property.

Property management done the traditional way can be described as a “black box,” said Brien. There’s typically been minimal insight into each property’s performance. An investor receives a financial statement, but has minimal insight into why their property performed in a certain way over the past 30 days.

“What events unfolded that led to this financial outcome that I’m seeing 30 days later? And what can we do to avoid it in the future?”

Typically, an owner has to pick up the phone and track down information, perhaps from multiple sources, Brien continued. It’s especially complicated when a company is managing single-family homes or several small multi-unit buildings spread out across a geographic region, with no onsite staff. “That’s where this black box thing comes from,” Brien said, in explaining how Mynd is different.

Roots as real estate investors led to better property management

“We founded Mynd about three years ago as a kind of offshoot of Waypoint Homes. My partner and I, Colin), founded Waypoint Homes back in 2009 and we were one of the first companies to start buying single-family homes, and ended up buying 17,000 around the U.S. in 13 markets. So, we developed some technology that made the way that we manage really efficient. We were very happy with how that company went and its success on Wall Street.”

According to Brien, one of the keys to success at Waypoint was building systems internally to measure performance. “We have a saying that’s one of our core values, ‘If you don’t measure something, it’s impossible to improve it.’ So, we believe in creating systems and tracking everything we do and measuring it fanatically, and then trying to improve it.

As individual investors, Brien noted, he and Colin wanted to add value to individual investors. “We believe in real estate as an asset class. To me, it’s the best, most attractive asset class there is to invest in.”

Many prospective real estate investors have a hard time taking the first step when it comes to investing, Brien said, because they don’t know how to take care of their property themselves, and they don’t have confidence in property managers. “Traditionally, a lot of property managers are mediocre at best.”

“It doesn’t mean that there aren’t great ones out there. It’s just I’ve been generally unsuccessful finding good property managers, and so we said, ‘You know what? We learned how to do this. And, we believe there’s a need. Plus, we can add value. Let’s do it.’ So, it’s been three years, and we’re up to 4,000 units in various West Coast markets.”

Property management is a people business

Over the years, there’s been a limited amount of innovation in the property management sector, and Mynd has set out to change that. “We are going out and trying to find the best, the brightest and the most talented. That’s a big reason why we partnered with Enrique.

“At the end of the day, no matter how much data or technology you apply to the business, this is a people business. It’s very operationally intensive, and we want to use technology to make great people even more effective in terms of the service we provide. Building a great team and having high-quality people is a huge part of what we do,” Brien said.

Changing role of property management especially in Seattle

Enrique Jevons says, “I know, being an owner, exactly what I’m looking for. Then, being a property manager, I get to see the other side of things, where you’re the middleman between the tenant and the owner.”

Jevons said his background in the hotel industry as a hotel general manager led him to Seattle and the property management business 11 years ago. He also personally owns 71 rental housing units.

In Seattle, Jevons manages nearly 800 units in Washington state. As a result, he is well-equipped to handle the needs of property owners and residents, since he gets to “experience it from both sides,” he said.

“I know, being an owner, exactly what I’m looking for. Then, being a property manager, I get to see the other side of things, where you’re the middleman between the tenant and the owner. It’s a very unique position to be in, and one I enjoy very much,” Jevons said.

What is the biggest stressor for owners and property managers in Seattle now?

“Keeping up with all the different changing legislation,” Jevons said. “And it’s happening really fast, which makes it difficult for the small property owner.”

According to Jevons, most owners of rental properties own one single-family home. Another large segment of investors owns less than four units in Washington State. Small residential owners struggle to keep up with every new city ordinance that passes, every new county ordinance and new state laws. Unfortunately, he remarked, there’s no one single repository where owners can go to for assistance.

“If you go online and do a Google search for City of Seattle rental laws, you’re going to come up with several different sites, none of which has all the city, county, and state laws.

Since each city has its own local ordinances, it’s hard to keep up with which city has what ordinance and how it applies to property owners. There’s no registry for property owners to receive all the information that they need on changes to laws, Jevons said.

Hard for property owners to find information

In my experience, owners don’t intuitively know that they are required to register with the city once they start operating rentals. They also don’t know that they have to procure a business license if they’re renting out a home, even one they inherited.

This uncertain climate makes it difficult for investors to acquire rental properties in the city of Seattle. For instance, there might be an opportunity for an investor to purchase a duplex in Seattle, but if rent-control laws make you question the viability of your investment, then you may decide to pass and purchase property in Texas instead, Jevons said.

Rental housing is a demand-and-supply business

If the City of Seattle becomes too restrictive for property owners, then investors have the choice to sell their property to an owner-occupant. As a result, the rental pool becomes depleted, and investors opt to buy investment properties elsewhere throughout the United States in rental markets that are less restrictive.

“You have this supply-and-demand equation. Trying to artificially regulate the supply of housing doesn’t lessen the demand. The demand is always going to be there,” Jevons said

“What we need to try to do, in my opinion, is make it easier for people to build and purchase rental properties so that we can increase the supply, and therefore make it less expensive for people to rent,” Jevons said.

Brien said Mynd wants to be a trusted partner for real estate investors.

Property manager’s job is to stay on top of regulations

It’s a property manager’s job to stay up-to-date on all of the changes to rent-control laws and city regulations, Brien explained. Mynd’s goal as a company is to “make it simple for investors to invest, and frankly, to also give them choices. We ultimately want be a national property management company.”

Somewhere between 80 and 85 percent of investors invest within a 60-mile radius of where they live because they don’t trust their property manager, Brien said. They don’t trust that things are going to get done, so they drive by and want to see it all the time and check on the condition of their investment. But it’s rare that within 60 miles of where you live happens to be the best place in the U.S. to invest.

To solve this problem, Mynd wants to provide investors with more data so they can make better investment decisions. This gives investors flexibility with respect to their investment decisions. At the same time, we are staying on top of all the changes and regulations in each city, so that owners have an “investment experience that’s pleasant and simple,” Brien said.

At the end of the day, everyone agrees that there’s a housing affordability problem in many cities, Brien said. However, he doesn’t believe the problem should be fully shouldered by property owners. He questions whether it’s fair for a resident who earns $250,000 a year to pay $800 a month in rent, which sometimes occurs in the city of San Francisco.

Changing role of the property manager from handyman to attorney

When asked how the role of property manager has changed over the years, Jevons said it’s evolved from being a handyman and customer service expert to becoming more of “an attorney function.”

Originally, he noted, the role of property manager was to provide great customer service. And, to determine what needed to be fixed at a resident’s property.

Now, it’s more about ensuring that property owners are compliant. Also that the rental agreement adheres to local, state and federal fair-housing laws.

“From a handyman to (almost like) an attorney. That’s how the job has changed.”

“Mynd Property Management is a customer-first, tech-enabled property management firm based in Oakland, Calif. Mynd focuses on the small residential sector, or multifamily and single-family rentals with fewer than 50 units. The company’s team of on-the-ground experts provide a combination of excellent service and efficient technology to boost net operating income (NOI) for property owners, while improving the rental living experience for residents. With management capabilities throughout California and Washington State, Mynd has aggressive plans to expand nationwide in 2019.”

7 issues and answers about renting to felons that landlords and property managers need to know now that Portland is considering placing rules on tenant screening.

By John Triplett

Are “no-felony-ever” lease clauses dead? We decided to ask this question of an expert in the field of investigations and tenant screenings to follow up all debate last year over whether landlords are required to rent to someone with a felony record.

David Pickron, owner of RentPerfect, an investigative screening company in Arizona, says the days of saying “no-felony-ever” are over for landlords unless the felony is a sex offense.

“We really tackled this hard in April and May of 2016 when the U.S. Department of Housing and Urban Development (HUD) first came out with their guidelines,” PIckron said in an interview.

“We also own an employment screening business and the Equal Employment Opportunity Commission (EEOC) came out with this years ago. Recidivism rates say if the (convicted felons) can get a job and find a place to live, then recidivism rates go down. So the government mindset is that it’s in our best interest to get these guys housing and to get these guys back into the employment field.

“The problem is that no one wants to take on that liability. Because on the other side, if they do something, we get sued or we all lose rent. So there is a big fight now between the private markets and the federal government.”

No. 1 – Is the “no-felony-ever” lease clause dead?

“And the whole thinking is they don’t want landlords to have an “ever clause” any more – meaning landlords say they do not ever rent to felons,” Pickron said.

“HUD’s thinking is based on a case from the 1960s. It is a University of Minnesota study that says if you commit a crime, and you do not commit another crime for seven years, then your risk is the same as someone who has never committed a crime before.

“They are hanging their hat on this study, saying, ‘How can you withhold housing from someone who has not committed a crime in seven years if they have the same risk as someone who has never committed a crime?’ “ he said.

David Pickron

“And if you do go and put your criteria at eight years or 10 years, you have to have evidence,” he said. As a landlord or property manager you cannot say, “Oh just because I wanted to,” Pickron said. “You have to have evidence that that reduced your risk. And there are no cases out there. That is why they have taken this 1960s case. It is because there is no other evidence.”

So it is hard for a landlord to do their own thing nowadays, he said.

No. 2 – No to renting to felons if a lifetime sex offender

“What we recommend our clients do is prohibit the lifetime sex offender. We have studies that show you are never cured from that,” he said.

What HUD is saying is that you have to back up your criteria. “And we can back up the sex offender issue with multiple studies that show someone is never cured from a sex offense,” Pickron said.

“The thing is, that doesn’t really change for us. It’s seven years since you have been released from prison or released from probation,” he said, and not when the crime happened.

“So really a murderer who did the crime in 1980 and got out two years ago, he can’t say, ‘Oh my crime was 25 years ago.’ We need to see seven years in society where you did not offend. That is the study that HUD is looking at and we will look at the same thing and say, ‘Ok, you can live here in your eighth year.’”

No. 3 – In society for seven years and no offense? That is OK

The key is WHAT the felon has been doing in society since he or she got out, he said.

“We are not even saying to our clients, ‘Hey it’s seven years since the crime was committed. It’s seven years since they have been back in society. So that takes a lot of those serious crimes out over seven years.

“There are articles where a Congressman came out and said he could not believe the number of criminals that were living in public housing. Our response to him was, ‘Where do you think they are living? They are not living out in the private market,’ “ Pickron said.

No. 4 – HUD rents to criminals in Section 8 housing

“What really shocks you is that HUD, in their own Section 8 housing, has criminals living there. And they are not supposed to be renting to criminals in those housing projects. But they overlook it all the time. They do not even follow their own criteria,” Pickron said.

“Let me tell you how this all played out on the employment end, just to give you an idea.

“They came out on the employment end and said you have to do what they call the ‘green factors.’ If you deny someone employment for a criminal history, you have to prove that it affects your risk. And now you have to look at how long ago the crime was done, how grievous was the crime, have they gotten any kind of rehab or anything to show they are rehabilitated? “

No. 5 – How HUD tries to create law

Since HUD and the EEOC are not legislative bodies, they cannot create law, he said.

“So how they try to create law works this way: They put out this argument, then they find somebody they can play this argument against, such as a big apartment community or employer. Then they take it to court and see what the judge says. If the judge rules for them, then they feel like they have created law without ever going to the legislative branch of the government.”

In the employment example, he said, this is how they get it done.

“So they sue. The EEOC sues Dollar General and BMW in these two cases. BMW settles for $1 million and says they do not want to fight.

Dollar General takes it all the way to the court. What ends up happening in the court is that the judge asks Dollar General, ‘What is your criteria. And they lay out their criteria – how they hire people and how they don’t – and how they make their decisions on whether to hire them. So they get off the stand, and then the Dollar General lawyer calls our federal government representative up on the stand and asks EEOC how they hire and they go through the same kind of hiring process, the same criteria.

“Dollar General looks at the judge and says, ‘How can you say we are discriminatory when the EEOC is doing it the same way? If we are discriminatory, then the EEOC is discriminatory. The judge dismisses the case.

“We have aligned all our clients to the way HUD brings on clients in Section 8 housing,” he said.

No. 6 – We call it a safe haven – do as HUD does

“We are calling it a safe haven. If HUD is doing it and we are doing it, they cannot come after us, you know.

“I saw on the National Association of Residential Property Managers (NARPM) website they had a couple of articles about where landlords had been sued. I got back to their attorney who said, ‘No we cannot find those cases.’

“The problem is it’s just cheaper to pay the fine that fighting it all the way up in the courts,” Pickron said.

No. 7 – “We cannot say ‘no-felony-ever’ anymore unless it’s a sex offender”

“We cannot say ‘never’ rent to a felon unless it is a sex offender,” Pickron said.

“The word ‘ever’ is huge unless it is a sex offender or someone who sells or manufactures methamphetamines.

“We are not that concerned about the HUD stuff because we have been through it on the employment side.

“In a way, it makes everybody look at their policies. And, it makes everyone update their policies.

“There are some landlords out there who just do not know what they are doing. I am a little on HUD’s side on this even though I can’t stand HUD. A landlord who does not know any better may deny somebody because of a crime when they were 18 years old. Now they are older, married, have kids, and make $150,000 a year and landlords are still hanging on to this felony to deny them.

“There is a point where if you have made a one-time mistake, you need to pay for it a little bit, just like credit. But then you need another shot at life. But if you are a continual repeat offender, I get it, you just live a lifestyle like that.

“It makes these landlords look at their policies and say, ‘Is our criteria really benefitting us?’ Because you could lose a lot of good renters too in not renting to a felon from 20 years ago.

“The reality of it is, if I had got caught doing some things when I was a kid I might have a record. But I never got caught so I act like I didn’t do it,” Pickron said.

“I think this is all going to change with the new President. We don’t want to discriminate. We will see if it backs off a little bit or changes when more conservative people get put in those posts. “

About David Pickron:

David Pickron has been a licensed private investigator for over 20 years, specializing in tenant screening for real estate investment owners and property management companies. His company, Rent Perfect, an investigative screening company, helps clients on-board tenants from the initial background check to leasing and payment collection. You can learn more by visiting www.rentperfect.com or calling 1-877-922-2547.

Portland and Seattle were ranked in the top 10 best places to live in the latest U.S. News analysis of the most populous metro areas.

To make the top of the list, a place had to have good value, be a desirable place to live, have a strong job market and a high quality of life.

Portland ranked No. 8

What’s it like to live in Portland, Oregon?

Portland’s population toes the line between an innocent playfulness and a shameless wild side. Naked bicycle rides, a fully costumed adult soapbox derby and Voodoo Doughnuts – a bakery that is known for making one-of-a-kind donuts – are a sampling of ways residents live up to the unofficial city motto: “Keep Portland Weird.” Locals tend to be friendly and laid-back while maintaining a healthy work ethic. This, combined with Portland’s emphasis on self-expression, has created a breeding ground for many independent businesses and startups.

Portland is a well-rounded region with more than just the offbeat shops and events. Museums, art galleries and the oldest public library on the West Coast feed a population with more academic degrees than the national average. The metro area’s loyal sports fans avidly support their NBA basketball team, the Portland Trail Blazers; MLS soccer team, the Portland Timbers; and major junior ice hockey team, the Portland Winterhawks.

Wilderness is also close by. Two mountain ranges and the Pacific Ocean can be reached in an hour or two, while the fertile vineyards of the Willamette Valley lure city dwellers with a thirst for something fresh.

To answer the question on many people’s minds: “No, it doesn’t rain all the time.” Seattle gets less rain annually than Boston, New York City, Philadelphia, Miami and many other major metro areas. The natural beauty of Seattle – it’s surrounded by both mountains and water on two sides – is one of the biggest draws for residents.

The scenery and proximity to nature, perhaps, contribute to Seattle’s inherent attitude: one of calm and patience. Locals are mocked for always allowing others to merge on the freeway, but that attitude extends to everyday life, where coffee shops harbor intellectual discussions, and nightlife is more about chilling with a beer at the bar than wild nights on the dance floor.

For many, living in Seattle has as much to do with what’s outside the city proper as what’s inside. Less than an hour from downtown, residents escape for the day or weekend to wineries, ski resorts, hiking trails and sprawling parks. Seattleites bring that love of nature into the city proper as much as possible, enjoying the city’s parks and tree-lined streets while staying cozy in fleece jackets (practically the local uniform).

The top 10 best places to live cities listed in this year’s ranking were:

Austin

Denver

Colorado Springs

Fayetteville, Ark.

Des Moines

Minneapolis-St. Paul

San Francisco

Portland

Seattle

Raleigh/Durham

Methodology

U.S. News & World Report’s Best Places to Live rankings are intended to help readers make the most informed decisions when choosing where to settle down. The metro areas included in the rankings are evaluated using data from trusted sources like the United States Census Bureau, the Federal Bureau of Investigation, the Department of Labor and U.S. News‘ own internal resources. This data was categorized into five indexes and then evaluated using a methodology determined by Americans’ preferences. The percent weighting for each index follows the answers from a public survey in which people from across the country voted for what they believed was the most important thing to consider when thinking about moving.

Portland photo credit Chris Anson via istockphoto.com

What are true apartment maintenance emergencies vs maintenance requests is this week’s maintenance checkup from Keepe to help guide property managers,

What counts as an apartment maintenance emergency in an apartment property, one that requires immediate action from a property manager and is not just a maintenance request from a tenant?

Any situation that threatens the safety and well-being of tenants.

The five events listed below are cases that would need immediate attention.

Educate tenants on these common – but serious – apartment maintenance emergencies and issues and make a proactive plan on how to deal with these these to ensure safety and to stay ahead of repairs.

No. 1 – Gas Smell

This should be No. 1 on your list. Natural gas is a huge hazard. Educate tenants by letting them know the importance in identifying this issue, and staying away from inhaling potentially poisonous gas. Address this issue over all others because this issue can be fatal.

No. 2 – No Heat or Air Conditioning

A broken heating or cooling system is cause for an emergency. If the HVAC system in your property fails to function, have the issue inspected quickly to ensure tenants stay safe from potential mechanical failures. Know who you are going to call ahead of time to fix this type of issue, and who you can count on to help if this maintenance emergency happens. Be prepared.

No. 3 – Power Out

Whether it’s just inside a unit or outside as well, electrical failure is another important reason to contact a maintenance professional. A power outage can quickly lead to safety issues. Property managers can become liable for power-outage issues surrounding untimely repairs or if the issue occurs frequently.

No. 4 – Plumbing Issue

If it’s more than a small leak, it is an emergency. Issues with plumbing can grow exponentially. In any case, turn the water valve off to ensure no further flooding ensues until a plumber checks out the issue.

No. 5 – Septic Tank Failure

A backed-up septic tank will overflow and allow toxic waste to flow near or even into a property, which is dangerous and damaging. Septic tank failures are extremely important to address immediately. Septic tank failures are also a larger and time-sensitive project to take on, so be sure to enlist an emergency maintenance professional for the job.

As a property manager, your top priority is to keep everyone in your building safe.

A sure way to address maintenance emergency issues is by keeping a list of potential maintenance vendors ready for your or have someone on-call at all times to manage maintenance issues. Regardless of your tactic, be sure to remain aware of these five possible emergencies.

Other recent rental property maintenance Keepe posts you may have missed:

Keepe is an on-demand maintenance solution for property managers and independent landlords. The company makes a network of hundreds of independent contractors and handymen available for maintenance projects at rental properties. Keepe is available in the Greater Seattle area, Greater Phoenix area, San Francisco Bay area, Portland, San Diego and is coming soon to an area near you. Learn more about Keepe at https://www.keepe.com

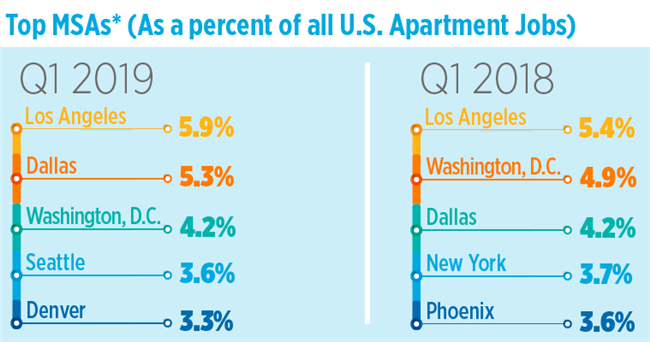

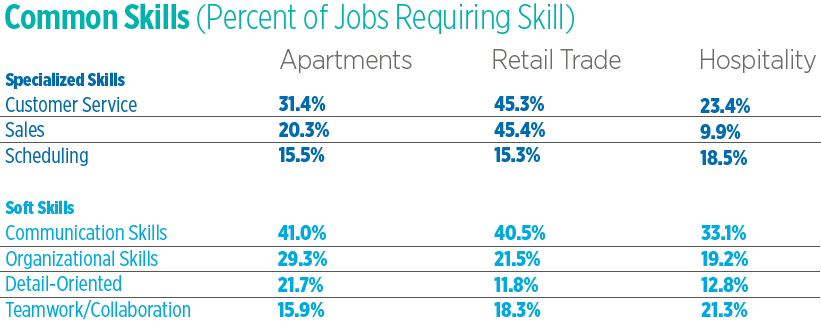

Apartment job talent is in high demand in Seattle as jobs openings in the apartment industry continue to grow.

Job listings for the apartment industry comprised nearly 36 percent of available real estate positions during the first quarter of 2019, well above the average for the past six years and a significant increase from 2018, according to the National Apartment Association Education Institute (NAAEI).

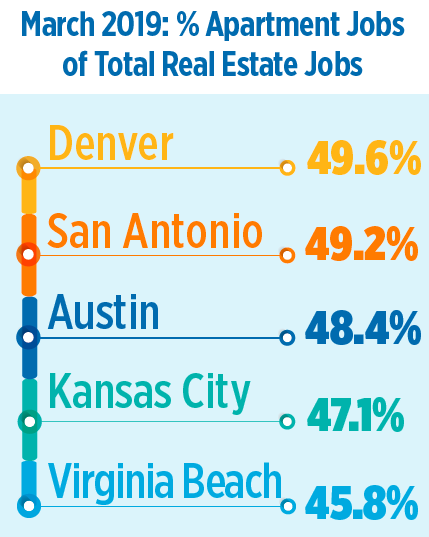

The NAAEI monthly jobs report ranking showed metro Denver on top in terms of the concentration of jobs in apartments versus other property sectors.

Competition for talent in both Denver and Seattle was particularly fierce given the high demand for jobs in the industry as well as in hospitality and retail.

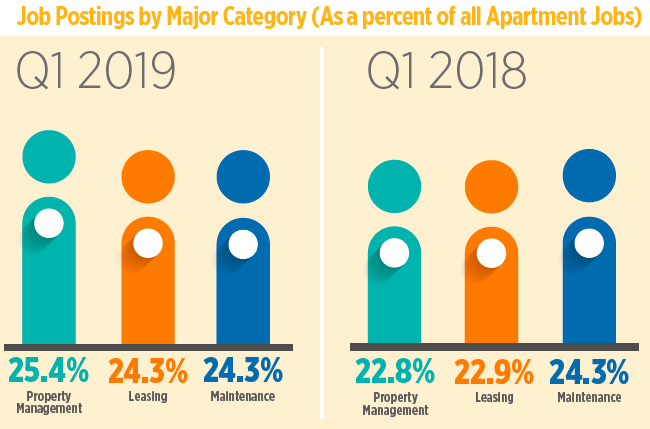

Positions in property management in demand

Positions in property management were in greatest demand during the first quarter with three of the top five job titles involving property management functions.

There were 5,600 job postings for property managers, community managers and assistant property managers combined.

Maintenance jobs in high demand

Maintenance jobs are often cited by industry professionals as some of the most difficult to attract and retain.

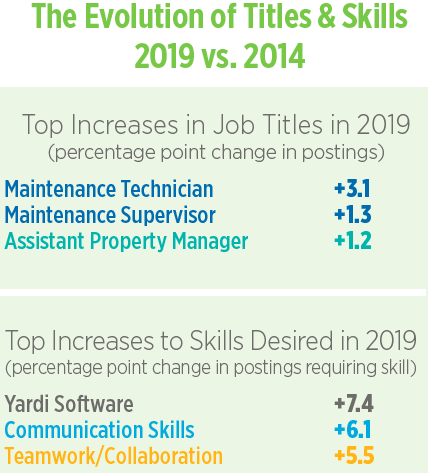

According to CEL & Associates, on-site maintenance jobs had the highest turnover rates, 37.3 percent, in 2017. Over the past five years, the two job titles most in demand, maintenance technician and maintenance supervisor increased their share of apartment jobs by 3.1 and 1.3 percentage points, respectively.

With the exception of the specialized skill of Yardi software (up 7.4 percentage points), changes in skills sets were typically more common among baseline, or soft skills.

Positions requiring strong communication skills and the ability to collaborate increased significantly since 2014.

Competition in Seattle more fierce than other cities

The apartment industry often competes with the hospitality and retail sectors, all of which require strong customer service, communication, and organizational skills.

Competition for talent in Denver and Seattle was likely fiercer than other cities given the location quotients for all three sectors are rated very high.

That means demand for all of these jobs is well above the U.S. average.

National apartment association jobs report background

The jobs report focuses on jobs that are being advertised in the apartment industry as being available, according to Paula Munger, Director, Industry Research and Analysis, for the National Apartment Association’s Education Institute.

“Our education institute is a credentialing body for the apartment industry. They hear often that one of the biggest problems keeping our industry leaders up at night is the difficulty in finding talent, attracting talent and retaining talent,” Munger said. “Labor-market issues are happening in a lot of industries, certainly with the tight labor market we have.”

NAA partnered with Burning Glass Technologies. “They have a labor-job posting database that is proprietary,” she said, and they can “layer on data from the Bureau of Labor Statistics (BLS). We looked at that and thought we could do something that is really going to help the industry and help benchmark job titles and trends as we go forward,” Munger said.

Multifamily rent growth and increases are dominated more and more by secondary and tertiary markets that are producing a disproportionate share of economic and population growth, and where rents are low enough that they can be raised without overly burdening tenants, according to the latest report by Yardi Matrix.

Overall U.S. multifamily rents jumped $4 in March 2019 as market dynamics “continue to be healthy almost everywhere,” said the report.

It was a steady first quarter for multifamily rent growth

While U.S. multifamily rents increased by $4 in March to $1,430, year-over-year growth dropped by 20 basis points to 3.2%, as rent growth was slightly less than the same period in 2018.

Nationally, rents were up 0.4% in the first quarter. The numbers demonstrate consistent growth, although not as strong as other first quarters in recent years. For example, rents grew by at least 0.8% in the first quarter between 2014 and 2016. Still, the market’s consistency remains a point in its favor.

Las Vegas (7.5%), pictured above, and Phoenix (7.2%) continued to top the nation’s growth in March on a year-over-year basis. Rent growth remains strong across the board, with Kansas City and Houston the only metros in our ranking that saw gains below 2.0% in March, according to the report.

Bigger markets still performing well

“To be sure, bigger markets are not performing poorly—not even close. San Francisco (3.9% year-over-year) and Los Angeles (3.4%) are seeing rent growth above the 3.2% national average, and primary metros Boston (3.1%), Chicago (2.7%), and Washington, D.C. (2.5%), are not far below it.

“The dynamics continue to be healthy almost everywhere. That gives investors a choice between potentially higher growth and higher yields in faster-growing, less-liquid markets, or slower, steadier growth in larger, more liquid markets,” Yardi Matrix said in the report.

Multifamily rent growth strong at the start of spring

As rental season comes into full swing, all but one market, Portland, had positive trailing three-month (T-3) rent growth.

Oregon recently passed rent control through the state legislature. While the initial bill allows for rent growth well above the national average, many in the industry are concerned it will lead to more stringent regulation.

Highlights of employment, supply and occupancy trends

February’s weak job growth number and decelerating GDP growth are signs that the expansion is slowing.

In response to those and other developments, the Federal Reserve said it would only hike policy rates once in 2019 and not at all in 2020. Treasury rates dropped sharply as investors worry about weaker growth.

While slower growth is not good for the multifamily market, tenant demand is likely to remain robust and investor demand shows no signs of weakening.

“The Federal Reserve’s decision to put rate increases on hold, coming on the heels of February’s weak job growth and decelerating fourth-quarter GDP, has created concerns about the economy’s health.”

Should the multifamily industry be worried?

“The short answer is no, not yet.

“But at the same time, as growth decelerates, the economy loses some of its ability to absorb negative pressures,” the report said.

About Yardi

Yardi® develops and supports industry-leading investment and property management software for all types and sizes of real estate companies. Established in 1984, Yardi is based in Santa Barbara, Calif., and serves clients worldwide.

Yardi Matrix is the industry’s most comprehensive business development and asset management tool for investment professionals, equity investors, lenders and property managers who underwrite and manage real estate investments in multifamily, industrial, office and self-storage. Email matrix@yardi.com, call 480-663-1149 or visit yardimatrix.com to learn more.

As the weather improves this spring, it is time to consider changing or improving the exterior paint color for your rental property so here is a quick guide in this week’s maintenance checkup from Keepe.

Choosing exterior paint colors can be tricky, especially for a multifamily property where you have to keep in mind the variety of styles your tenants favor.

A paint job is a quick way to upgrade your property’s value and curb appeal.

Tenants will be pleased with the upgrade and that boost in morale will often result in happier tenants.

In this guide, you will find what color of paint to use, how to pick a complementary color, and why you should be painting your property.

How to pick the perfect exterior paint color for your rental property

In general you should stick to timeless finishes and neutral paint colors when choosing the exterior paint color for your rental property.

When you update your exterior with a fresh paint job, be sure to think carefully about what colors you will be using.

In general you should stick to timeless finishes, in other words neutral paint colors.

To appeal to the masses, stick to colors such as beige, grey, cream and tan. Also, make sure your exterior paint varies from the inside of your building.

At the least, be sure to vary the hues outdoors by a couple of shades to ensure your property is offering your tenants an enticing greeting.

Pay attention to how the colors in your building influence the mood of your space to ensure you are providing a welcoming presence. Warmer tones tend to offer people a feeling of security and warmth whereas cooler tones offer calming and inspiring response to people.

When choosing multiple colors for your exterior, consider adopting a complementary color scheme. First, assess what tone you want, warmer or cooler, and stick within your tone when you look for a perfect complimentary finish.

Deciding When to Paint

As a landlord, deciding when to paint your property can be a big decision.

On one hand, it’s important to limit unnecessary expenses, while on the other hand, maintaining a fresh and clean living space is crucial to your business.

Evaluating your property’s current condition should be the first step before deciding to take on paint makeover. Painting your property should be a priority for the following reasons:

To aid wear and tear: Painting your property should be a part of your regular maintenance. Owners should expect to upgrade their exteriors every few years to protect the health of your exterior building and maintain a fresh feel for you and your tenants. A little paint can go a long way in your investment property. Re-paint your property every 5-7 years to please your tenants and maintain optimal property maintenance.

Competitive edge: If your rental property is facing significant competition, a fresh paint job can boost the aesthetic and feel of your property and attract new tenants and keep your investment thriving. Modern accent color to special features of your building such as windows or entry ways can add a special touch to your property.

Painting your rental property should be a part of your regular maintenance

Alternatives to Painting

If you find that your property doesn’t need a fresh coat of paint, consider these easy alternatives to maintain your curb appeal:

A power wash: Review the state of your current exterior paint job. Are there any scuffs or dirt marks building up on the walls? Sometimes a simple power wash can take care of the buildup and leave your exterior refreshed and looking like new. If it’s been less than five years since your last exterior paint job, try this alternative before committing to a new coat of paint.

A partial paint job: If your current paint job is in shape or you don’t want to invest in upgrading your entire exterior at one time, try a partial paint job. Paint the high traffic areas such as the main office, walkway areas, and other spaces outdoors between buildings where tenants reside. You can also stick to freshening up your property by adding a contrasting color to the trims of your building. Remember, new paint doesn’t have to be an all or nothing project.

Take these tips into consideration to help you make the decision on whether or not a paint job is right for you and your property.

Regardless of your reasoning, remember that upgrading the exterior paint job of your residential property can benefit both potential and current tenants.

Ensure your property stays up to date by regularly scheduling property maintenance practices into your routine.

Other recent rental property maintenance Keepe posts you may have missed:

Keepe is an on-demand maintenance solution for property managers and independent landlords. The company makes a network of hundreds of independent contractors and handymen available for maintenance projects at rental properties. Keepe is available in the Greater Seattle area, Greater Phoenix area, San Francisco Bay area, Portland, San Diego and is coming soon to an area near you. Learn more about Keepe at https://www.keepe.com