While economic growth and a strong job market have helped multifamily asking rents grow nationally in August, operators are now facing the rapid expense growth on that side of the ledger, led by mushrooming property-insurance costs, Yardi Matrix says it in its national report for August.

“With rent growth slowing, property owners increasingly must implement strategies to pare expense growth to maintain and grow net income,” the report says.

“After several years of stellar income growth, multifamily is facing headwinds that include not only decelerating rent gains but a rapid uptick in expenses. During the trailing 12-month period ending June 2023, expenses for multifamily properties nationally grew by an average of 9.3%, up 63% from the 5.7% increase during the previous 12 months,” according to Yardi Matrix data.

“During that period, the average property operating expense rose $740 per unit to $8,694, according to Matrix. Costs rose significantly in most categories, led by insurance, which increased by an average of 18.8% in the 12 months ending June 2023, per Matrix. Insurance is rising because of the growing number of significant weather-related events, such as hurricanes, extreme temperatures and wildfires, that have created large insurer payouts, particularly in the Southeast, California and Texas,” the report says.

Highlights of the August report

Asking rent growth in August was concentrated in the renter-by-necessity segment, which increased by 0.1%, while lifestyle rents declined 0.1%. The composition of rent growth reflects a substantial supply increase in some areas, as most deliveries are lifestyle units, which increases competition within the segment.

- Multifamily performance continues to hold up well, as rents and occupancy were relatively flat in August. The average U.S. asking rent rose $1 to $1,728 during the month, while year-over-year growth fell to 1.5%, down 20 basis points from July.

- In the short term, supply growth remains a driving factor in metro-level rent growth. Most metros with the highest year-over-year asking rent growth, such as New York, Chicago, Indianapolis and San Diego, benefit from a weak new supply pipeline.

- Single-family rents (SFR) fell slightly, down $6 nationally to $2,104. Year-over-year, national SFR rent growth fell 70 basis points to 0.5%. SFR demand remains strong overall, but there is some evidence of deceleration in the high-end segment.

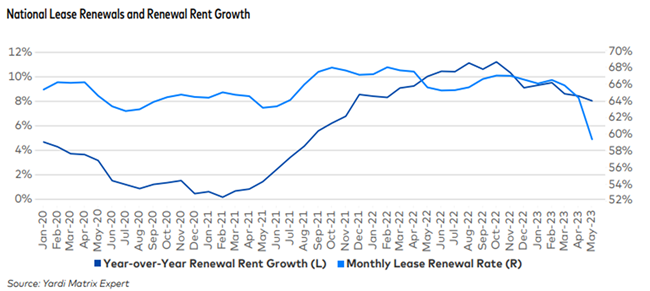

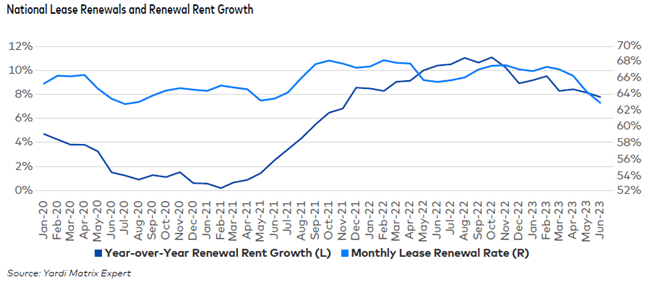

Lease renewal rates continue to slow

Renewal rent growth fell to 7.8% year-over-year as of June, down 40 basis points from May.

Renewal rents, the change for residents that are rolling over existing leases, has slowed since peaking at 11.1% in 4Q 2022 as more tenants get caught up to asking-rent rates. Only a handful of metros continue to see double-digit growth in renewal rents. Miami has had the largest renewal rent growth at 12.4% while San Francisco had the smallest at 1.8%. Growth was between 5.6% and 9.7% year-over-year in 26 of the top 30 markets in the report.

National lease renewal rates were 62.9% in June.

“Renewal rates have been steadily declining since mid-2022, which is attributable to the large amount of new supply that has come online. As new deliveries are made available, occupancy rates decline, which compels properties to offer greater concessions and consequently creates the incentive for more renters to move,” Yardi Matrix says in the report.

Read the full Yardi Matrix report here.

About Yardi Matrix

Yardi Matrix researches and reports on multifamily, office and self-storage properties across the United States, serving the needs of a variety of industry professionals. Yardi Matrix Multifamily provides accurate data on 18+ million units, covering more than 90 percent of the U.S. population. Contact the company at (480) 663-1149.