Landlords are not the enemy and do not want eviction of tenants, so BYU Law and University of Arizona Law have created a new online tenant-landlord communication tool to help deal with the eviction crisis across the country.

The new online tenant-landlord communication tool called Hello Landlord is intended to help with issues that can lead to evictions was created by the two university law schools and a subsidiary of a law firm.

“Eviction is a national crisis, and the ripple effects of an eviction are devastating to families and communities. We went into this challenge knowing that we wanted to design a scalable, bilingual, jurisdiction-agnostic solution that could positively affect widespread change,” said Stacy Butler, director of the UofA’s Innovation for Justice program, in a release.

“For most people, that eviction notice is the last chapter in a much longer story about systems failure. We hope that by spreading the word about this new access-to-justice tool and making Hello Landlord available to as many people in as many states as possible, we can encourage communities to think preventatively about the justice gap.”

The free web-based tool helps tenants communicate with their landlords about issues that can lead to eviction. This nationwide resource is a result of a semester-long collaboration between BYU’s LawX Legal Design Lab and UofA Law’s Innovation for Justice program, which share a commitment to addressing pressing legal service issues with new products and solutions.

Landlords are not the enemy and do not want eviction of tenants

“As we train the next generation of lawyers, we want to instill the notion that going to court is not always the solution,” said Kimball D. Parker, LawX director and president of SixFifty, in a release.

“When it comes to evictions, the adage ‘an ounce of prevention is worth a pound of cure’ certainly applies.

“We found that most landlords don’t want to evict tenants and are receptive to working with those who proactively reach out. The collaboration with the University of Arizona and SixFifty has resulted in an online de-escalation tool that has the potential to help anyone who has missed rent, or is experiencing an issue with the condition of their rental, avoid legal problems,” Parker said.

More than two million evictions in 2016

“We found that most landlords don’t want to evict tenants and are receptive to working with those who proactively reach out,” Parker said.

In 2016, more than two million people in the United States were evicted from their homes. Tucson is a Top 25 evicting city according to Eviction Lab. Less than 20 percent of tenants there appear in eviction proceedings; of those who appear, 90 percent do so without counsel; and 96 percent of cases result in eviction judgments against tenants. Lack of legal representation is also an issue in Utah, with a 15:1 defendant-to-lawyer ratio in the state.

Hello Landlord is available for free at www.hellolandlord.org with English and Spanish language options for tenants to generate a letter about a missed rental payment or a problem with their rental.

Developed by the BYU and UA students, and built on SixFifty’s automation platform, it features simple, guided questions such as “What is your landlord’s first name?” and “Why can’t you pay rent?” The software then generates a letter that clearly and respectfully explains the tenant’s situation and proposes a solution.

Nearly 90 percent of the landlords who have previewed the tool said they would be willing to work with the tenant to resolve the problem if they received a similar letter.

At the beginning of the fall 2018 semester, five LawX and 10 Innovation for Justice legal-design lab students were tasked with utilizing a design- and systems-thinking framework to develop one or more scalable solutions to increase housing stability for tenants in underserved communities by reducing the frequency of eviction. The diverse group of students brought different skills and experiences to the process, including one student who was served with an eviction notice during the semester. Together, the students observed more than 220 eviction court proceedings and spoke with dozens of stakeholders, including judges, landlords, tenants, social services providers, attorneys and journalists. They found that by the time a tenant is served with an eviction notice, the eviction process in both Arizona and Utah is too rapid and rigid to afford an opportunity to stabilize the situation at stake. In many states, there are few legal defenses available to tenants once an eviction lawsuit has been filed.

The students were interested in developing an upstream solution that could increase the likelihood that tenants and landlords would resolve issues that can lead to evictions. Specifically, students were interested in targeting a communication gap they observed between tenants and landlords, in which tenants felt powerless to reach out to landlords when at risk of missing a payment or experiencing a problem with a rental property, and landlords felt that tenants did not reach out to try and resolve payment or rental issues.

Hello Landlord is the second web-based brainchild to come from BYU’s LawX innovation lab, which also created SoloSuit – an award-winning online tool that helps Utahns who cannot afford legal services to respond to debt collection lawsuits.

If you are an apartment owner involved in property management, a property manager yourself or a real estate investor, there are property management questions to ask about how the property is managed from different viewpoints.

Here is a look at 30 questions that touch on the issues no matter what your job, or job title, with your rental property based on blogger Larry Arth’s 30 years in real estate investing.

I have had my share of property management issues, so speaking from a position of strength, allow me to share some diligence that I have uncovered over the years on asking and interviewing property managers.

Understanding this principle I asked myself why anyone who invests part-time would try to manage their own properties.

The reason we have so many bad tenant stories is answered in this discovery.

If it takes 10,000 hours of diligence and passion invested in a discipline to be successful, it is then imperative to have a professional who has the credentials of these 10,000 hours of practice behind them to successfully manage tenants and the landlord business.

We understand that a property manager is to your investment, as your engine is to your car. Without a great finely tuned engine your car does not deliver you your intended outcome which is a safe journey without accident or incident.

Likewise, without a systemized, knowledgeable, experienced property manager, you will never get to your intended outcome which is a safe profitable business operated without incident.

The first questions have to do with finding good tenants. A building with good tenants tends to have fewer maintenance and other issues.

How many vacancies do you have right now? Out of how many total units that you manage?

What is the average length of time it takes to fill a vacancy?

Is that average time getting longer or shorter?

How do you market your rental units?

How do you use the web site to attract new tenants and to keep prospects informed?

What factors would make you reject a prospect?

Would you accept a tenant who met your qualifications in some areas, but not others? Which qualifications are most important to you?

What screening methods do you use?

Property Management Questions – Tenant Management

The next questions relate to tenant management. It’s just as important to keep good tenants as it is to find them.

How do you collect rents?

What is your late rent policy?

What other rules do you set for tenants?

What percentage of tenants do you have to evict?

How does the eviction process work here?

How do your tenants contact you?

Property Management Questions – Maintenance

Which kinds of maintenance jobs are handled in-house?

Which kinds of maintenance jobs are handled in-house?

Which ones do you use an outside handyman for?

Which ones do you use professional contractors for?

How many quotes do you get for jobs?

How expensive does a job have to be for you to contact me before doing it?

What are your rules for contractors being inside occupied rental units?

Who are your preferred contractors?

Property Management Questions – Experience

You want managers to know the local real estate world inside and out.

How long have you been a property manager?

Do you have any certifications?

Does your locality require landlords to have a license or permit to operate a rental and if so what are those fees?

Do you understand the local rules and ordinances to accommodate things such as local licensure requirements and or section 8 requirements?

Do you personally invest in real estate in this area?

Finally, you need to understand your arrangement with the property manager

What is your fee structure?

Are your reports web based if not how do we get them?

Do you require an exclusive arrangement to broker the property?

How much notice will you give before terminating a contract?

Additionally you can always be on the watch out for the easy tell-tales signs of expertise, or lack thereof, things like:

A manager with a messy office.

Managers who are hard to connect with by phone or email.

I always believe that how you do anything is how you do everything.

About the Author:

Larry Arth is a landlord and the founder and CEO of Equity Builders Group, a Florida based Real Estate investment Group. As a 36 year veteran to real estate investing, Larry understands that we are now in a global economy and as times have changed, investment strategies must change as well. Larry is an international recognized consultant and speaker and assists hundreds of investors per year, both foreign and domestic to realize their investment potential. He analyzes locations across the country for economic strength and the locations that yield the largest most sustainable return on investment. Within these locations he seeks out and gathers the best teams to deliver sound, high performing and most importantly sustainable turnkey investment. He works with investors to ride the wave of each area-specific market surge. Larry’s primary focus is offering (Non Listed) safe and sustainable turnkey investments to the passive investor.

Portland City Council members heard testimony from landlords opposed to the proposed $60 per unit fee saying it is nothing but a “tax on renters” and “one more thing being dumped on the backs of landlords.”

Two landlords, Marc and Kathy Rogers, spoke against the proposed fee saying they own an apartment building at 19th and Hawthorn and provide an affordable housing alternative in that area.

Marc Rogers shared information about an email exchange he wanted to keep anonymous with another landlord who said, “I would likely email all my tenants and let them know that due to policies of city council, their rents would be going up by $25 a month.”

Demonizing landlords

“It’s a very polarizing subject and I think it’s easy to look at landlords and demonize them as not caring and interested only in the bottom line,” Rogers said. Then in response to a council question he said, “I think that maybe the use of demonization was not the correct word to use. I think that the policies of council over the last couple of years have been very negative towards landlords.”

Commissioner Chloe Eudaly spoke up to say, “It’s not my intention to demonize landlords. Some of my best friends are landlords.” She also questioned why a landlord would raise rent $25 a month to cover a fee that is $60 a year.

Rogers said that any time the price of a commodity goes up “that’s typically passed on to the end user. If the price of diesel to deliver bread to Fred Meyers goes up, Fred Meyers is going to pass that along for a loaf of bread at their store. And that’s just typically the way businesses work.

“I think sometimes, in my opinion, landlords aren’t necessarily looked at as small businesses. We’re a small business. We’re really not any different than any other mechanic shop or coffee shop or restaurant. We’re small business people. In my opinion the attitude of this council in the last two years has been that we’re in some way not a small business. That we’re something different than that, and that we are not good people,” he said.

Eudaly responded that she was a small business owner of a bookstore for 22 years and said, “Granted, I had a bookstore and books come with a preprinted price on them. Unfortunately, rental units don’t.”

“I want landlords to recognize the fact that they are business owners. We hear from a lot of, especially small landlords, who feel like this is something they do on the side. It’s almost more of a hobby or a supplement. And, they feel some of the regulations are forcing them to professionalize in a way they’re not equipped to do. So I see you as a small business,” Eudaly said. In response to Roger’s friend who said he would raise rent $25 to cover the new fee she said it was “hard for me to take your friends’ comment seriously because that’s just not reasonable.”

Rogers gave some perspective to what is going on in Portland saying “we are commercial Realtors.” He said they deal in smaller properties such as duplexes and fourplexes.

More landlords putting their rentals up for sale

Rogers said two years ago you would be lucky to find a dozen duplexes on the market in close-in zip codes.

“I checked two days ago, there were 61 duplexes on the market” in close in zip codes he said.

“The feedback we get consistently is that the small mom and pops who own the duplexes don’t want to deal with the lower barrier of entry with security deposits, with amortization schedules, with rent control, and the sophistication level for them.

“They’ve decided to get out. So that takes inventory off the market and adds cost,” Rogers said.

Eudaly responded saying, “Well, I don’t think that we can draw a direct correlation between our regulations or policies and changes in the real estate market without adequate data.

“But I will say there’s a plus side to having more housing on the line. I don’t disagree with you at all. And that rental services office will actually help landlords navigate these little changes. So it kind of supports this item,” she said.

Why Not Make The Tenants Pay The Fee Since The Services Are For Them?

Kathy Rogers told the council, ““I think a lot of small landlords feel like all of the costs and fees and complexity are being dumped on the landlord and not shared by the tenant.”

Kathy Rogers added to Marc’s comments saying, “This fee in and of itself may not seem like a huge deal, but I think as Mark alluded to, coming on the heels of everything else that’s been thrown at landlords over the last two years, it feels a lot like the straw that’s breaking the camel’s back.

“And I think a lot of small landlords feel like all of the costs and fees and complexity are being dumped on the landlord and not shared by the tenant,” she said

“If this is to support the rental services commission, which I’ve been in contact with and as far as I can tell about 90% of what they do supports tenants. Why are the tenants not paying the fee,” she asked.

“How about with every lease renewal? The tenant pays the $60 fee. Why is it 100 percent paid by landlords?

She said “all of this has come at us in the last two years, you know, with the mandatory renting relocation assistance, the elimination of no cause notice evictions, rent control, new tenant screening ordinances, which our attorney can’t even figure out and he’s a real estate attorney, plus the security deposit ordinance and the rental registration program. And now this,” she said.

“It’s very difficult to navigate and I will tell you that a lot of small landlords are afraid to rent out their properties. They’re afraid of being sued. They’re afraid of not following the rules. A lot of the single-family and duplexes that are being sold are now being purchased by owner occupants. Those are rental units that are be taken off of the market,” she said.

Hurting the people you are trying to protect

Kathy Rogers said, “We never used to raise our rents every year. We have two now every year on the anniversary, 100 percent of the time we raise our rents to the 100 percent maximum that we’re allowed to do because of the actions taken by the city council. And we never used to do that.

“So I just want you to think about everything you’re throwing at us may be hurting the people you’re trying to protect,” she said.

It’s a Portland thing to do

Marc Rogers also told the council “I’d like to share a story and it might take more than 27 seconds. But for the last 11 years I’ve had somebody living in my building on 19th and Hawthorne for free.

“We pay his utilities and we provide him with a cell phone. Probably $1,000 a month, maybe $12,000 a year. We don’t have a formal agreement. We don’t even have a handshake, but what we have done is he looks out for my interest and I look out for his and I think that’s the right thing to do.

“I think it’s a Portland thing to do and I think that’s what we’ve shown that we’re willing to do and have done for the last 11 years. So that’s really my closing and I would hope that you would reconsider this and maybe take more input,” Rogers told the council.

$60 per unit fee is “just too high”

Jill Warren, who described herself as a mom and pop landlord in Portland for the past 30 years, said she owns 34 units.

“So we will be paying $2,040 a year to support the program. I just think that’s too high, $60 per unit fee,” she said.

Small landlord Jill Warren told the council, “I just think that’s too high.”

Then she added, “I appreciate the previous conversation about the demonization. I feel that some of the mandates that are being brought down by this body actually it hurts our industry.

“For example you don’t want us to factor in the criminal background for a tenant and that’s very dangerous. I just screened an applicant who had 17 pages of felony convictions, including felon in possession of a firearm, theft, burglary, possession of methamphetamine.

“I protect the safety of my tenants. My primary goal is their welfare and their safety. So that’s why I screen. It’s all about screening.

“Also the mandate to pick the first applicant that comes along. I mean that’s not a very intelligent to do that. That’s why we screen. I run a criminal check. I do a background search. I check your credit history and your previous and current landlord referrals. So I just throw that all in a pot, and I stir it up, and that’s how I determine their eligibility,” Warren said.

Commissioner Chloe Eudaly said, ““I can’t allow this forum to be used to spread misinformation about our policy. We are not requiring landlords to not consider a prior convictions. That’s a choice.”

Eudaly then responded to Warren saying, “I can’t allow this forum to be used to spread misinformation about our policy. We are not requiring landlords to not consider a prior convictions. That’s a choice.

“And the first-come first-served as first come first to qualify. We’re not requiring landlords to literally rent their units to the first person that applies. So those are two false statements that you made. And I just want to ask everyone else who comes up here to try to avoid spreading misinformation.”

Portland’s proposed $60 per unit fee 20 times higher than Seattle’s fee

Michael Havlik, deputy executive director of Multifamily NW, told the council, “My association members are dismayed with the current rendition of the proposed rental registration fee. It is yet another layer of tax on housing adding cost to a market already in crisis.

“Not only is the amount proposed excessive at a $60 per unit fee, but offends common sense that the implementation of our registration system will cost millions of dollars each year.”

Michael Havlik, deputy executive director of Multifamily NW, told the council, “My association members are dismayed with the current rendition of the proposed rental registration fee.”

Havlik said in the past he worked for several property management firms and home forward as director of asset management. “I have a passion for housing affordability and rental services and I’ve spent my life dedicated to it all. I have 26 years of experience in property management including conventional multifamily housing, affordable tax credit, public housing, permanent supportive housing as well as special needs housing.”

He said the members of Multifamily NW “make up 40% of Oregon’s rental housing supply and as such we are the leaders in property management and development within the state.

He said for a comparable 200-unit property in Seattle the fee is $575 for $2.88 cents a unit compared to $12,000 for a comparable 200-unit property in Portland.

Ultimately a tax on renters

“In other words, the city of Portland’s rate will be over 20 times the amount of Seattle. We estimate that by year 10 of this fee scheme, the city of Portland will have collected $58 million that will do nothing to create more affordable housing,” Havlik said.

“It’s ultimately a tax on renters. Impacting those most who have lower incomes and do not have the good fortune of living in regulated affordable housing, which receives the special carve out with a housing supply shortage.

“What rational jurisdiction would meet out punitive disincentives to housing providers?

“The city of Portland is creating inequity across all rental housing providers by imposing a fee for the sole purpose of funding multiple duplicative programs already implemented or addressed by other better equipped agencies.

If you’re truly striving to provide solutions to the problem for the lack of affordable housing across the continuum of housing, then you would continue the path outlined by the legislature through house bill 2001 and 2003 which both work to create diverse, inclusive and vibrant housing opportunities throughout our city.

Additionally, the city should reassess its posture towards housing providers It has demonized over the last several years. These providers are a big piece of the solution and you should view our members as willing partners in the goal of making housing more affordable and accessible to all Portlanders.”

Director of Operations for Commerce Properties, Chris Nguyen, said the fee “will be harmful to Portland renters by reducing new development in low- to moderate-priced rental housing, putting upward pressure on housing cost, and reducing the quality of existing rental housing.

Chris Nguyen said the $60 per unit fee could “hire a part-time maintenance technician. Could allow us to replace 23 carpets. Allow us to put appliances in 16 new apartment homes.”

“Now this tax combined with additional state and local legislation introduced over the last few years makes it difficult for housing providers to provide affordable housing and it reduces the incentive to develop new units or keep existing units on the market,” Nguyen said.

Maintenance could suffer due to new fee

Nguyen said the proposed rental fee reduces funds available for maintenance.

“This tax for the company I work for will have a $27,000 annual impact. This fee could hire a part-time maintenance technician. Could allow us to replace 23 carpets. Allow us to put appliances in 16 new apartment homes.

“So this means that many housing providers will have to pay fees with funds that they would have normally used to improve or maintain existing housing.

Testimony in favor of the new fee

Several spoke in favor of the new fee, including Margot Black from Portland Tenants United, a registered lobby organization with the city of Portland who is also a member of the rental services commission.

“I’m here to testify today in support of rental registration fee with some minor reservations. But I’m going to bypass most of my testimony just to respond to a couple of the concerns that I’ve heard come before the council.

“Just so you know, fees are strictly regulated by the state and the landlords of Portland would not be able to explicitly pass this fee on in their lease as a fee. However, I just got a 90 day notice for $150 a month rent increase that will start this November. I’ll be paying $150 every single month. One of the reasons my landlord gave me for that was increased fees by city council,” Black said.

“Frankly as a tenant every time we hear about tenant protections or things that are going to help tenants costing us money and ultimately hurting us, when my rent can already go up by hundreds of dollars a month, I would much rather some of that money be going to the city to provide programs and services for renters than just going in my landlord’s pocket,” Black said.

Mayor said fee has long been a priority of his

Mayor Ted Wheeler introduced the discussion on the fee by saying, “I’m pleased to bring forward the rental registration fee, which is long been a commitment and a priority of mine to help support the office of rental services and establish a system to collect more accurate data of the rental market in Portland.

“In 2017 we set a rental registration requirement for all units in the city of Portland. In the first year of registration, we did not charge a fee. That was deliberate. We wanted to encourage voluntary compliance for landlords, but it’s been clear from the beginning that a fee would need to be established,” the mayor said.

“We asked the revenue division in the Portland Housing Bureau to return to us this year with the established fee. Since 2017 we’ve made consistent progress and increasing the city’s role in landlord tenant law and services, including establishing the rental services office, the Rental Services Commission, adopting local landlord, tenant law, increasing landlord tenant services and increasing training and education services.

“Portland is one of the only cities our size to not have a rental system in place and fees to cover the basic services. We’re behind the curve and this is an imperative first step to allowing us to have a more robust and streamlined support for renters in our community.

“This council has also made it clear the importance for data may data-driven policy making. This fee will support the maintenance of an expanded registration system. Something that I’ll be back in the fall bump to ask for support of this council for funding for the procurement of the expanded system so that we have data not just on the number of units and their location, but accessibility, general unit characteristics and other relevant market data. The recommended fee is in response to the budget note. We included in our adopted budget this fiscal year and it’s reasonable when compared to other cities in the region and across the country,” Wheeler said in his opening statement.

From top left to right clockwise, Kathy Rogers, Mike Havlik, Jill Warren and Chris Nguyen

We’ve been getting a lot of calls in the past few weeks at Keepe about how to fix tenants’ clogged toilets. Here’s some interesting information about toilets, and six unclogging tips from our professionals!

The average person flushes the toilet five to six times each day, adding up to nearly 2,000 flushes per year.

When a toilet stops working, it’s an emergency maintenance situation that needs to be fixed as soon as possible because it creates an immense inconvenience for your tenants.

Toilets account for nearly 30 percent of the water usage in bathrooms, so keeping these essential plumbing fixtures in good condition is a must.

Doing routine maintenance for toilets can go a long way. If you do not catch simple leaks early, you may find the problem months later, when the water bill is $100 more than usual. Some actions as simple as having your maintenance people regularly clean and check for leaks can catch a toilet problem early and save money in the long run.

If a toilet is clogged, the first thing you should try is using a toilet plunger, which can dislodge the clog so it can be flushed through.

If the plunger doesn’t work, try using a toilet auger, which can reach deeper into the plumbing of the toilet in order to dislodge clogs.

6 Tips for Fixing Those Annoying Clogged Toilets

Inspect the toilet’s inner workings every six months.

Never pour a chemical drain cleaner down your toilet; it can cause damage to your plumbing pipes.

Clean your toilet regularly with baking soda, vinegar or mild soap.

Consider what kind of toilet paper you are using; some break down less effectively than others and can cause clogs to happen more often.

If you get brown water backing up into your shower or sink when you flush, call a plumber immediately; these are signs of a more serious issue.

Inspect for leaks using food coloring. Add 6 drops of food coloring to your tank. If your toilet bowl water changes color, you have a leak!

About Keepe:

Keepe is an on-demand maintenance solution for property managers and independent landlords. We make hundreds of independent contractors and handymen available for maintenance projects at rental properties in the Greater Seattle, Greater Phoenix, Greater San Francisco Bay and Greater Portland areas. We’re also expanding. Learn more about Keepe at http://www.keepe.com

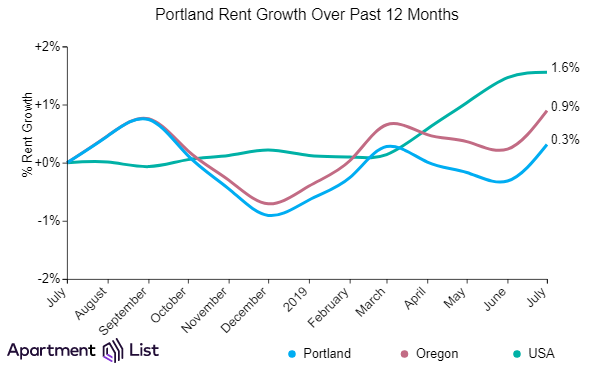

Portland rents have increased 0.6% over the past month after two months of declines, but have been relatively flat at 0.3% in comparison to the same time last year, according to the July report from Apartment List.

Currently, median rents in Portland stand at $1,131 for a one-bedroom apartment and $1,334 for a two-bedroom. Portland’s year-over-year rent growth lags the state average of 0.9%, as well as the national average of 1.6%.

Rents rising across cities in the Portland Metro

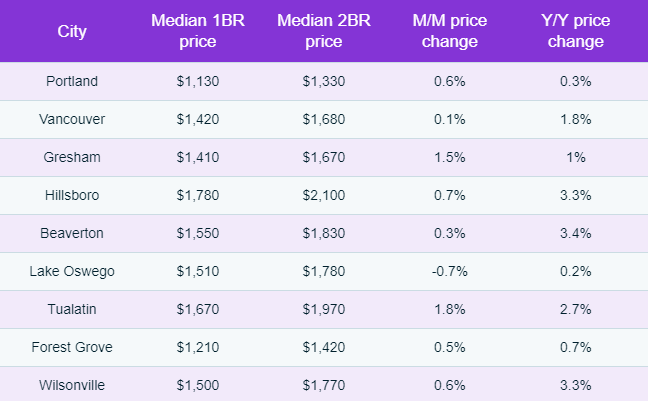

Throughout the past year, rents have remained steady in the city of Portland, but other cities across the entire metro have seen rents increase. Of the largest 10 cities that Apartment List has have data for in the Portland metro, all of them have seen prices rise.

Oregon as a whole logged rent growth of 0.9% over the past year.

Here’s a look at how rents compare across some of the largest cities in the metro.

Looking throughout the metro, Hillsboro is the most expensive of all Portland metro’s major cities, with a median two-bedroom rent of $2,102; of the 10 largest Oregon metro cities that we have data for, all have seen rents rise year-over-year, with Beaverton experiencing the fastest growth (+3.4%).

Hillsboro, Vancouver, and Eugene have all experienced year-over-year growth above the state average (3.3%, 1.8%, and 1.6%, respectively).

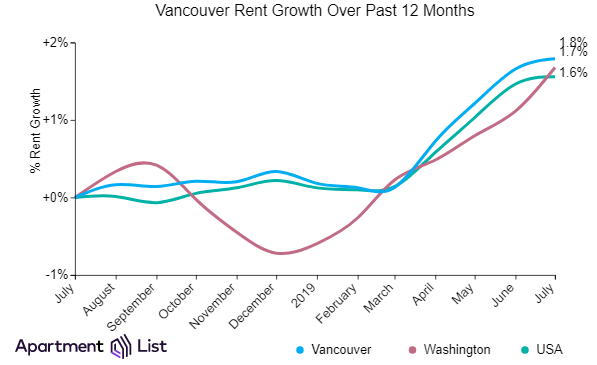

Vancouver rents increased over the past month

Vancouver rents have increased 0.1% over the past month, and are up slightly by 1.8% in comparison to the same time last year.

Currently, median rents in Vancouver stand at $1,420 for a one-bedroom apartment and $1,675 for a two-bedroom. Vancouver’s year-over-year rent growth leads the state average of 1.7%, as well as the national average of 1.6%.

Portland rents more affordable than many comparable cities nationwide

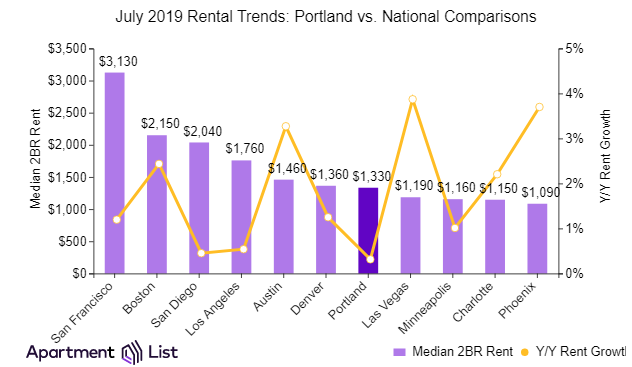

Rent growth in Portland has been relatively stable over the past year – some other large cities have seen more substantial increases. Portland is still more affordable than most similar cities across the country.

Portland’s median two-bedroom rent of $1,334 is above the national average of $1,191. Nationwide, rents have grown by 1.6% over the past year compared to the stagnant growth in Portland.

While rents in Portland remained moderately stable this year, similar cities saw increases, including Las Vegas (+3.9%), Phoenix (+3.7%), and Austin (+3.3%); note that median 2BR rents in these cities go for $1,186, $1,085, and $1,460 respectively.

Renters will find more reasonable prices in Portland than most other large cities. For example, San Francisco has a median 2BR rent of $3,126, which is more than twice the price in Portland.

By Sebastian Moya Associate- Kay Properties and Investments, LLC

The Great Recession probably resulted in a seismic shift in many real estate investor’s risk profiles. In 2007, the primary investment strategy was aimed at residential properties with large amounts of market speculation. These properties were largely financed with debt and when the market collapsed, well we all know the story. In 2019 we are experiencing a 1) very peaky market with 2) compressed cap rates on residential properties 3) throughout secondary markets that are assigned values relative to 4) large growth in that market. This all sounds a little too familiar. There is no need to be Chicken Little in this market as the imminent correction (and it is imminent) will probably not strike investors as starkly as it did in 2008. Multi- family and single-family homes can be worthwhile investments with the right placement of capital. However, there are lessons to be learned about other investment strategies that were pervasive in the years following the recent economic downturn.

Many investors that held onto their real estate or invested in the price-trough from 2008 until now are considering what to do with their properties considering the price peak we are currently experiencing. It is an excellent time to sell, but with cap rate compression across the board it is a difficult time to find the right placement of capital. Investors that are looking for lucrative IRRs may go towards the residential route, which is fair but potentially risky. Other investors that want to weather the ensuing market slowdown have looked towards a less speculative route. Triple Net properties have skyrocketed in the last ten years as a result of this investor desire

Triple Net Property

A piece of property that is usually being leased by a single tenant (i.e., single-tenant net-leased or STNL). The building on that property is typically built to their needs and business model. The tenant typically has contractual obligations in their lease to make monthly rent payments to the property owner over the life of the lease. Higher quality tenants would usually be of a high credit grade, large in scale, and/or is financially robust in a way that will assure they pay their rent consistently.

Why would a company do this?

In an effort for companies to reduce the amount of liabilities on their balance sheet, they choose not to purchase the real estate on which they conduct business. Instead, the companies decide to rent it from real investors who own said properties.

What does Triple Net lease mean?

“Net” helps describes the responsibilities attributed to either the tenant or the landlord. A “single Net” lease hands over more costs and responsibilities to the landlord in exchange for higher rent. The rent may be higher in a Single Net, but the costs vary much more and affect cash flow.

“Triple Net” is a type of lease structure wherein little to no responsibilities are given to the landlord and the variable costs of the property (taxes, insurance, maintenance, etc.) are handled by the tenant.

Triple Net properties have emerged as a pervasive investment strategy over the last decade for many reasons.

Consistent Cash Flow

The lease structure described for NNN properties should allow for dependable cash flow that passes through to investors on a monthly basis. These cash distributions are effective income, and yours to keep. There are little to no costs that bite into your bottom line. This is ideal for the retirement or passive income profile investor.

Triplet Net Lease Guarantees

More often than not, the tenant will guarantee payment of rent throughout an established period of time. A typical rent period exists between seven and fifteen years. In shorter leases, tenants will incentivize investors with “rent bumps” that could increase their net operating income by 1- 2% each year. If a tenant vacates the building, or “goes dark,” they would be liable to pay the remaining term. The tenants are varying degrees of credit quality as ranked by the large ratings agencies or backed by large franchisees. This is not a total guarantee, however. Any business can go bankrupt or fail to meet its obligations for any number of reasons. It is important to understand your tenants’ profile and backing before entering into a contract with them. Triple Net Properties provide the opportunity to invest money into real estate and benefit from potential appreciation on property, while playing it relatively safe with a consistent cash flow from their asset. But at the end of the day, this is still real estate we are talking about. There are

many risks and obstacles and investor should we weary about.

Inflation Risk

Triple Net lease buildings can act as a sort of “one-trick pony.” You know what you are getting for how long and how much, but your property could end up being stagnant in cash flow or relative value. The longer the lease that is negotiated with a tenant, the less they are willing to pay. This means the likelihood of “rent bumps” goes down or does not exist. You are effectively trading a longer “guaranteed” income for less cash to your bottom line. If inflation increase on average one percent a year, then without significant cash flow escalations you may be losing money on your cash investment. This is why it is important to analyze a lease structure when you are looking for a tenant and negotiate rents and lease terms appropriately.

Tenant Risk

Although a tenant may be guaranteed on the triplet net lease, there is always the possibility that they default on their payments or go dark. If they default on their payments this is really the worst case scenario. Your cash flow stops completely, and the value of your building potentially decreases immensely. With Triple Net leases, the value is inherently tied to the tenant filling the property and paying rent. The cash flow is what would entice potential investors to buy the property from you. Even if the building goes dark and cash flows are rolling in, there is no exit strategy when the lease terminates. Again, the building’s value is inherently tied to the tenant that provides cash flow to it.

Re-Tenant Risk

The leases on these properties are structured for extensions, or “options.” This means tenants can exercise a clause in the lease that would add more time to their rental period. However, this usually involves a lot of negotiation with a large company that has many units across the country. Since your property value is tied to the tenant, and the tenant knows this all too well, they will try to strong arm you into paying tenant improvements or adjusting the lease to their benefit. If you don’t play ball, there is a chance they will relocate or simply vacate upon termination of the lease. In reality, a lot of these large companies don’t care to negotiate at all and may move before the lease is up. Then it is potentially the job of the investor to commit capital towards finding a new tenant through brokerage, advertising, attorney fees when negotiating the lease, and other costs.

Operations

Although this property is a relatively cost-free venture, you are still in charge of managing the property. If there is a power outage, you are in charge of finding a solution. If it hails, you may have to repair the roof. The tenant might reimburse you for the costs, but ultimately it is the investor’s obligation to take care of the building. Those looking for a completely hands-off investment may be turned off by this.

Investment Risk

The ultimate risk in investing in Triple Net lease properties is that you are investing in a venture that costs hundreds of thousands of dollars, if not millions, into one investment. As any person that has remote financial knowledge will tell you, diversification is key when investing. Putting all your eggs in one basket is scary It is a large risk in any real estate venture, but with triple-net properties it is nonetheless a substantial factor to recognize. So, there are many ways to look at triple net properties. The benefits are unique to most real estate assets. The risks are also diverse and require astute attention when considering them as an investment opportunity. It seems that the risks can outweigh the benefits in many ways. How would someone who is looking to exercise passive investments mitigate the risks mentioned above. Let’s talk about Delaware Statutory Trusts. The tools that a Delaware Statutory Trust can give you to smooth out some of the obstacles you would encounter when investing in triple net properties while emphasizing the positive points.

Delaware Statutory Trust (DST)

DSTs are a financial structure that allows for investors who are looking to invest in real estate to diversify their opportunities into different properties. It is a shared ownership structure wherein an investor puts in a piece of capital for a property instead of the entire backing. DSTs are passive investments, which means that all management responsibilities are removed from investors and income is passed through. This is meant to be a refresher on DSTs and if you are interested in learning more we recommend you visit our website www.kpi1031.com or speak to one of our representatives. In a DST structure, your eggs are not all in one basket. Chunks of capital can be distributed to different assets. Amongst the types of properties that can utilized in this structure are triple net properties. There are several advantages to investing in triple nets through DSTs that help absorb some of the risks you may encounter when investing in one on your own.

Sponsor Companies – an important concept to understand when it comes to DSTs are their sponsor companies. Sponsor companies are the entities that underwrite, acquire, and manage properties for investors. These large entities manage billions of dollars in real estate and have years of experience under their belt that help investors make educated DST investments. They are a huge advantage when it comes to investing as will be demonstrated.

Negotiation

One of the primary ways to mitigate risks when investing in triple net lease properties is the way in which the lease between the tenant and the investor is negotiated. In a situation wherein an investor is investing in a property on their own or perhaps in a small group of investors (such as an LLC, LP), negotiating a lease will be difficult. Large tenants that are creditworthy and therefore increase the value of a potential property also have more negotiating leverage. These large companies negotiate leases all the time in ways that may affect rent bumps, which means an investor could be exposed to inflation risks. The tenant improvements they require in order to stay, or their capacity to leave overnight are also pieces of a lease that can be negotiated and need to be considered. DST properties are managed and negotiated by sponsor companies that have years of experience and immense deal flow that allows them to get more at the negotiating table than the average investor could.

Operations

In a DST structure, investors will experience a more realized passive investment. Instead of worrying about management of the property or fretting about tenant demands, sponsor companies take care of all operations and management concerns. Investors are given monthly or quarterly updates about any changes to the properties, but there are no hands-on requirements asked of anyone participating in a DST. Diversification Of the benefits offered by DSTs, arguably the most helpful is the diversification that they can provide. When you are investing into DSTs, it is possible to split a chunk of capital into pieces and distribute said capital amongst several properties. For example, you can invest one hundred thousand in a FedEx property in Seattle, and three hundred thousand in a triple net Walgreens in Phoenix. The point is that you are not placing all of your capital into one place. If your property in Seattle “goes dark,” for some reason, you are not at a total loss because you still have your investment in Phoenix. Hedging your investment and receiving a blended return on those investments protects you from more risks. This is especially useful in triple net properties where tenants can be finicky. Protecting yourself from risk is something rarely afforded in the world of real estate.

Through DSTs, the benefits of triple net properties are realized while spreading the risks out through negotiation, operation, and diversification advantages. At the end of the day, we are talking about real estate. Any property can have a bad run or sail smoothly throughout an ownership period. Anyone interested in DSTS should consult their CPA or attorney about their specific situation. DSTs are not for everyone, but they can provide an alternative way to invest in triple net properties if that is your interest.

Kay Properties and Investments, LLC is a national Delaware Statutory Trust (DST) investment firm with offices in Los Angeles, San Diego, San Francisco, Seattle, New York City and Washington DC. Kay Properties team members collectively have over 114 years of real estate experience, are licensed in all 50 states, and have participated in over $7 Billion of DST real estate. Our clients have the ability to participate in private, exclusively available, DST properties as well as those presented to the wider DST marketplace; with the exception of those that fail our due-diligence process. To learn more about Kay Properties please visit: www.kpi1031.com

This material does not constitute an offer to sell nor a solicitation of an offer to buy any security. Such offers can be made only by the confidential Private Placement Memorandum (the “Memorandum”). Please read the entire Memorandum paying special attention to the risk section prior investing. This email contains information that has been obtained from sources believed to be reliable. However, Kay Properties and Investments, LLC, WealthForge Securities, LLC and their representatives do not guarantee the accuracy and validity of the information herein. Investors should perform their own investigations before considering any investment. IRC Section 1031, IRC Section 1033 and IRC Section 721 are complex tax codes therefore you should consult your tax or legal professional for details regarding your situation. This material is not intended as tax or legal advice.

There are material risks associated with investing in real estate, Delaware Statutory Trust (DST) properties and real estate securities including illiquidity, tenant vacancies, general market conditions and competition, lack of operating history, interest rate risks, the risk of new supply coming to market and softening rental rates, general risks of owning/operating commercial and multifamily properties, short term leases associated with multi-family properties, financing risks, potential adverse tax consequences, general economic risks, development risks and long hold periods. There is a risk of loss of the entire investment principal. Past performance is not a guarantee of future results. Potential cash flow, potential returns and potential appreciation are not guaranteed. For an investor to qualify for any type of investment, there are both financial requirements and suitability requirements that must match specific objectives, goals and risk tolerances.

Securities offered through WealthForge Securities, LLC. Member FINRA/SIPC. Kay Properties and Investments, LLC and WealthForge Securities, LLC are separate entities

There are reasons why you do not want to move in everyone who applies, obviously, but what safeguards are you putting in place with your lease offers? Read what an expert with 25+ years in marketing communications experience with Fortune 500 and entrepreneurial companies has to say about this topic.

By Ellen Calmas

It’s pretty obvious that occupancy drives revenue, and leasing (among other things) drives occupancy.

What’s less obvious is that there are times it makes more sense to let a prospective lease walk away.

Property owners and managers spend millions of dollars annually screening prospective residents to gain better insights into their ability to afford, retain and adhere to the specifications of a lease.

Screening results in a rejection, an acceptance without conditions, a conditional lease offer, or a lease offer with mandatory requirements. The conditional and mandatory categories typically include safeguards for timely rent delivery and/or protection against future inability or unwillingness to pay rent on time.

Herein lies the rub in that the prospective resident who agrees to extra conditions upfront – no matter how relatively easy or onerous – is typically the resident who wants to perform reliably. Yet sometimes things work out and other times they don’t. That’s why safeguards are tied to lease offers in the first place – to protect the property company.

So what’s the implication when a prospective resident declines a conditional or mandatory lease offer?

A few options come to mind:

The prospect can’t afford what’s being asked

The prospect doesn’t want to move in with the lease offer terms

The prospect doesn’t want pay rent on time

Pick any one of the above and you’re better off letting that prospect walk away. Yet with upwards of 35-45 percent of all lease acceptances falling into a conditional or mandatory category, it makes sense to have alternatives built into your lease offers to help protect a community’s bottom line that also contribute to increased leasing velocity.

NPS Rent Assurance does just that as an alternative to a higher security deposit that enables prospective residents to better afford move in costs while demonstrating their commitment to deliver rent reliably throughout the life of a lease.

Residents who enroll in our rent budgeting program linking rent to payroll tend to stay in their apartment homes over 550 days, or twice the industry average, so things work by design. On the flip side, the prospect who walks away from a lease offer that includes rent budgeting flunks a secondary, less obvious layer of screening that illustrates either their financial insecurity or their future intention to fall down on their lease.

Stated differently: prospects typically enroll in our program unless they really don’t want to put structure in place to assure their rent will be paid on time – and that’s not a resident you want to move in. Period, full stop.

Ellen Calmas is co-founder and executive vice president of Neighborhood Pay Services, LLC / NPS Rent Assurance and brings 25+ years marketing communications experience with Fortune 500 and entrepreneurial companies to her role in strategic planning and marketing and sales support. She is also responsible for brand positioning, outbound marketing and digital networking as well as coordination of partner programs. Ellen has held senior management positions for marketing communications firms serving such clients as GlaxoWellcome, Bausch & Lomb, Avon Products, Heinz USA, AT&T, The House of Seagram, among others. She actively supports numerous health, civic and arts organizations throughout the Boston area and currently holds board positions for Silent Spring Institute, a leading research and advocacy group dedicated to identifying links between women’s health and the environment. She received her B.S. from the Roy H. Park School of Communications at Ithaca College. She can be reached at 617.209.3048 ext 104.

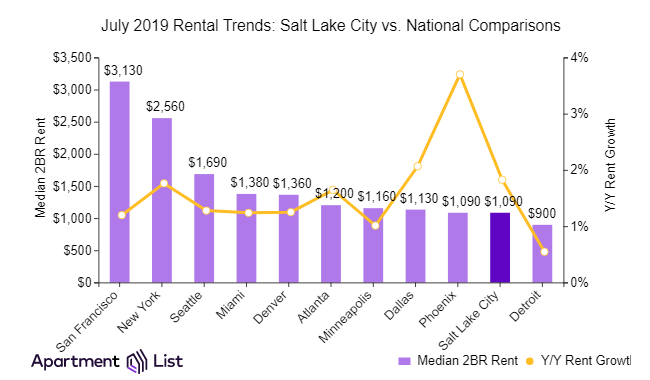

Salt Lake City rents have remained flat over the past month, however, they are up slightly by 1.8% year-over-year, according to the August report from Apartment List.

Currently, median rent stands at $875 for a one-bedroom apartment and $1,085 for a two-bedroom.

Salt Lake City’s year-over-year rent growth leads the state average of 1.7%, as well as the national average of 1.6%.

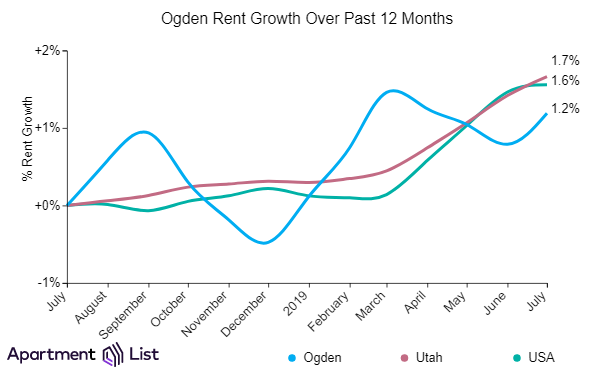

Ogden rents increased significantly over the past month

Ogden rents have increased 0.4% over the past month, and are up slightly by 1.2% in comparison to the same time last year.

Currently, median rents in Ogden stand at $695 for a one-bedroom apartment and $891 for a two-bedroom. Ogden’s year-over-year rent growth lags the state average of 1.7%, as well as the national average of 1.6%.

Salt Lake City rents more affordable than many large cities nationwide

As rents have increased slightly in Salt Lake City, a few large cities nationwide have also seen moderate rent growth. Salt Lake City is still more affordable than most large cities across the country.

Salt Lake City’s median two-bedroom rent of $1,085 is below the national average of $1,191. Nationwide, rents have grown by 1.6% over the past year compared to the 1.8% rise in Salt Lake City.

While Salt Lake rents rose slightly over the past year, many cities nationwide also saw increases, including Phoenix (+3.7%), Dallas (+2.1%), and New York (+1.8%).

Renters will find more reasonable prices in Salt Lake City than most large cities. For example, San Francisco has a median 2BR rent of $3,126, which is more than two-and-a-half times the price in Salt Lake City.

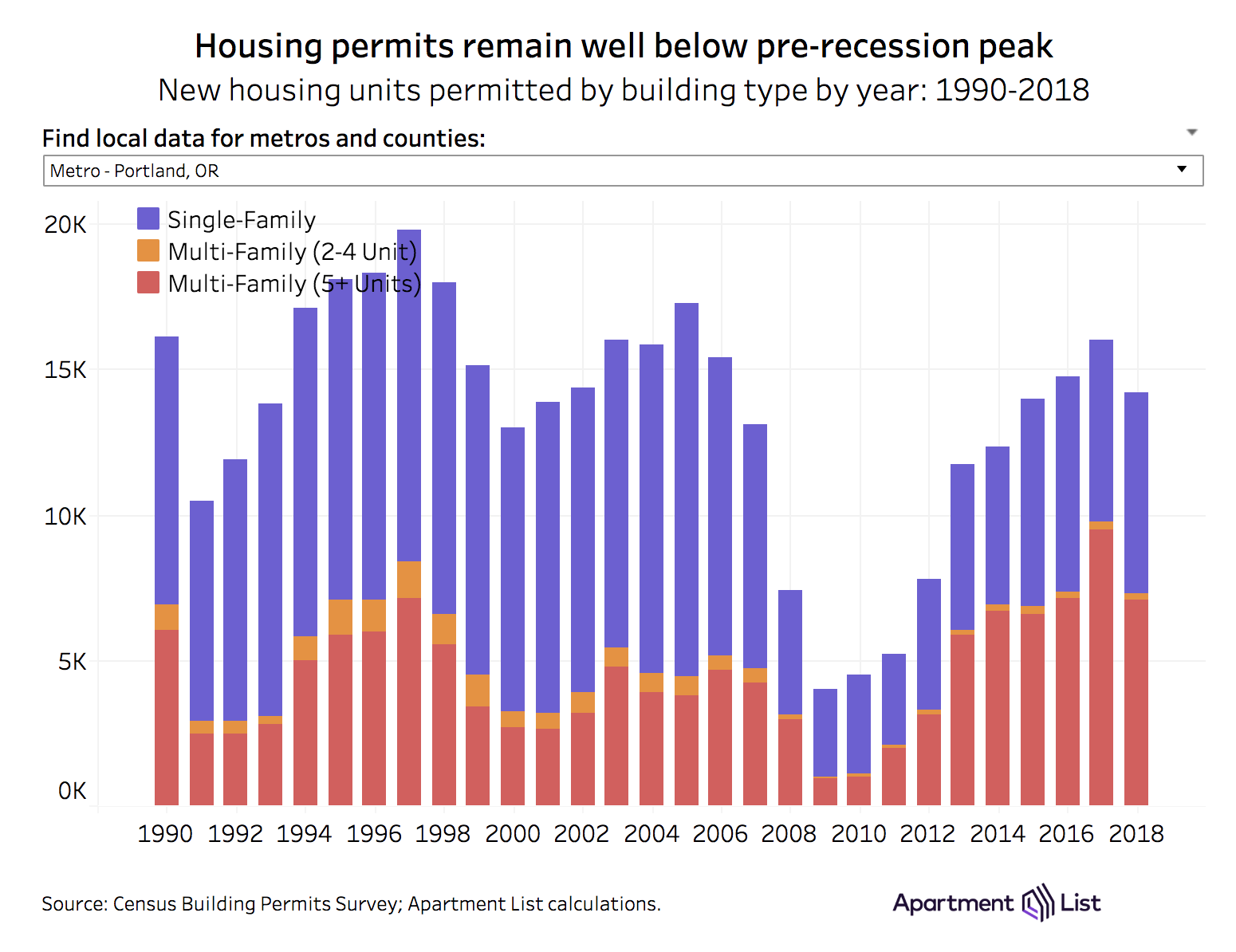

A new report shows that approved housing construction and development nationally remains 38 percent below its pre-recession peak, according to Apartment List. Stagnant single-family home construction and a select group of coastal markets are to blame. Meanwhile multifamily apartment buildings are increasing in size.

Smaller metros and booming multifamily construction, on the other hand, are picking up the slack.

Portland housing construction analysis

An average of 4.4 new housing units per 1,000 residents were permitted in Portland from 2008 to 2018. The rate of permitting activity ranks #12 among the nation’s 50 largest metros.

Over the same period, Portland added 6.7 jobs per 1,000 residents, ranking #13. This implies that 1.5 jobs were added for every new housing unit in the metro, a level which indicates a balance between supply and demand for new housing.

Since 2006, multifamily units have accounted for 46% of housing permits in Portland, compared to 32% in the pre-recession period from 1990-2005. Nationally, the multi-family permit share increased from 23.4% in the pre-recession period to 33.9% in more recent years.

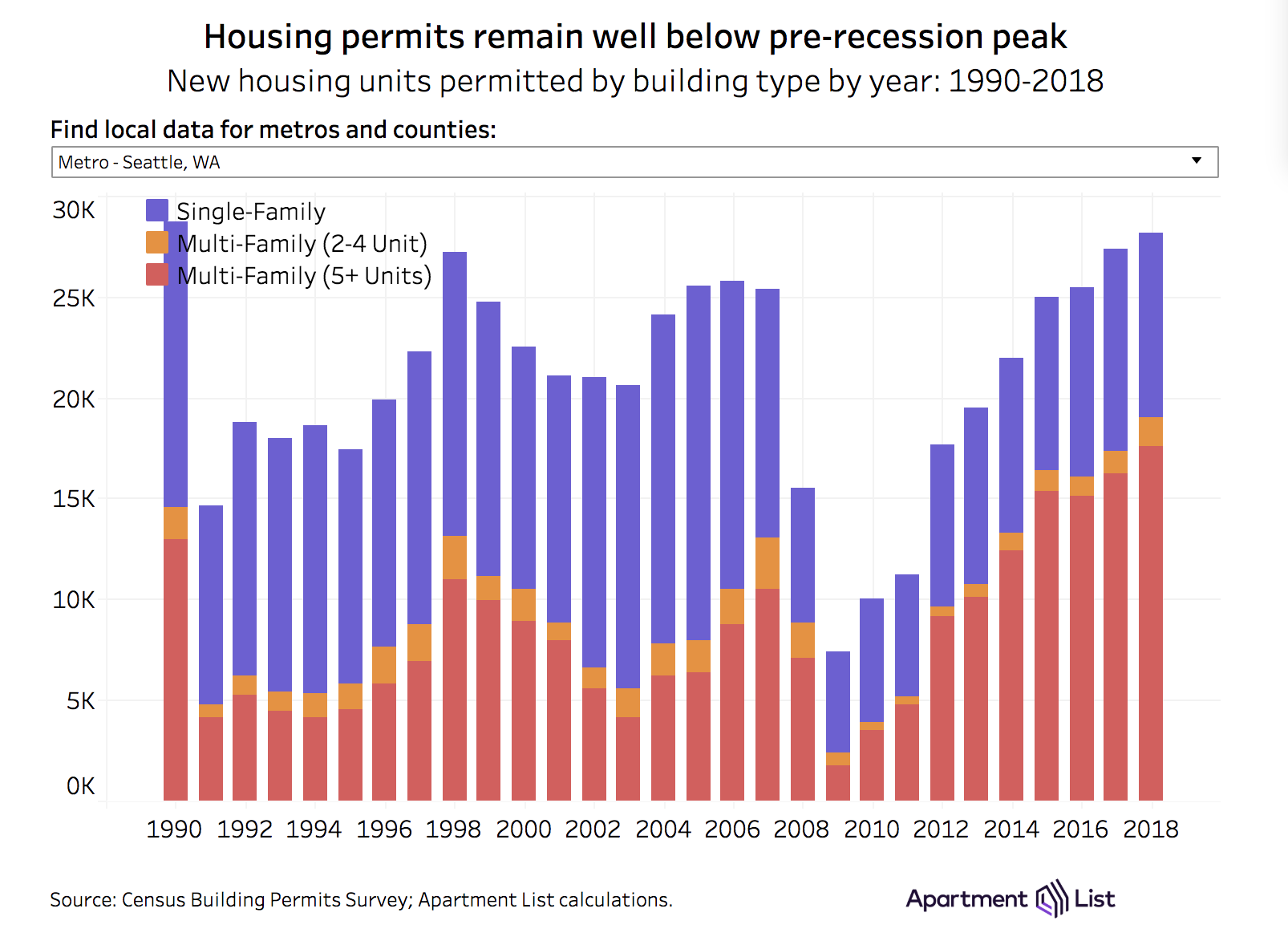

Seattle housing construction analysis

An average of 5.2 new housing units per 1,000 residents were permitted in Seattle from 2008 to 2018. The rate of permitting activity ranks #9 among the nation’s 50 largest metros.

Over the same period, Seattle added 7.4 jobs per 1,000 residents, ranking #12. This implies that 1.4 jobs were added for every new housing unit in the metro, a level which indicates a balance between supply and demand for new housing.

Since 2006, multifamily units have accounted for 56% of housing permits in Seattle, compared to 38% in the pre-recession period from 1990-2005. Nationally, the multi-family permit share increased from 23.4% in the pre-recession period to 33.9% in more recent years.

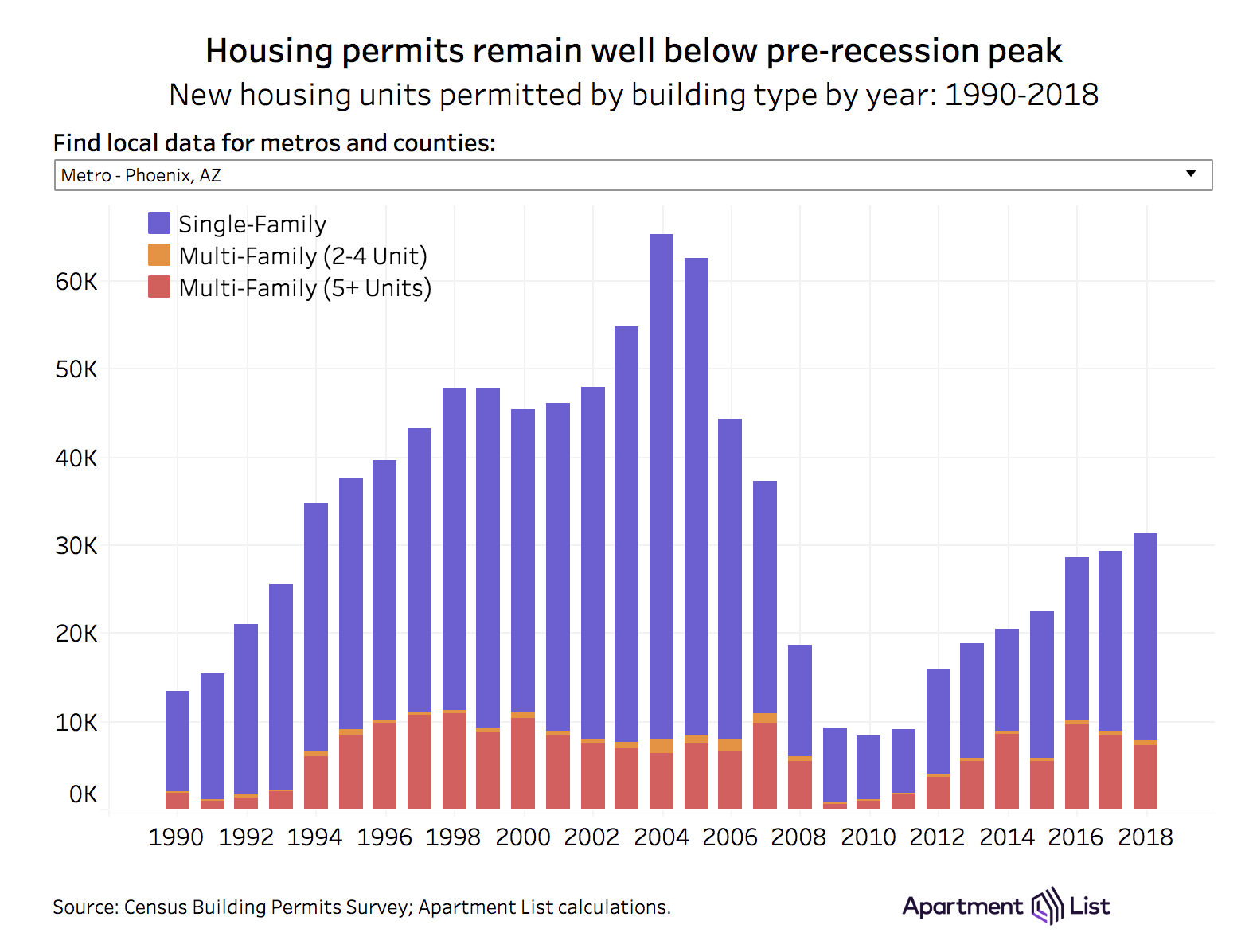

Phoenix housing construction analysis

An average of 4.2 new housing units per 1,000 residents was permitted in Phoenix from 2008 to 2018. The rate of permitting activity ranks #14 among the nation’s 50 largest metros.

Over the same period, Phoenix added 5.1 jobs per 1,000 residents, ranking #21. This implies that 1.2 jobs were added for every new housing unit in the metro, a level that indicates a balance between supply and demand for new housing.

Since 2006, multifamily units have accounted for 27 percent of housing permits in Phoenix, compared to 18 percent in the pre-recession period from 1990-2005. Nationally, the multifamily permit share increased from 23.4 percent in the pre-recession period to 33.9 percent in more recent years.

Single-family construction lags while multifamily has rebounded

Apartment List economist Chris Salviati writes in the report that housing affordability has emerged as a key issue in national politics, as millions of American households struggle with their housing costs. That said, housing and labor markets are inherently local, and distinct trends are playing out in different regions of the county.

In many of the nation’s largest coastal metros, acute housing shortages have led to rapid increases in housing costs. However, many smaller metros are actually adding more than enough new housing to keep pace with job growth, indicating that affordability issues in these regions may be driven more by a lack of well-paid jobs than by a shortage of housing.

“In order to better understand these issues, we analyzed data from the Census and Bureau of Labor Statistics to better understand how much new housing is being built and where. We study how that new housing supply lines up with job growth for counties and metro areas across the U.S., and discuss how these findings fit within the broader conversation around housing affordability across America,” Salviati writes in the report here.

In the recovery years that followed, multi-family housing construction rebounded fairly quickly, driven by a trend toward urbanization that increased demand for housing in and around city centers. The number of multi-family units permitted surpassed its pre-recession peak in 2015 and has since maintained that pace.

Meanwhile, construction of single-family homes has recovered much more slowly — the number of single-family housing units permitted in 2018 was barely half the number permitted in 2005. Consequently, multifamily units have made up a much greater share of new housing in the post-recession period. From 1990 to 2005, multi-family units made up 23.4 percent of all residential building permits issued, while from 2006 to 2018, that share increased to 33.9 percent.

Despite the boom in apartment construction, multi-family housing has not been able to fully compensate for the lack of new single-family construction. The total number of residential housing units permitted in 2018 was roughly the same as the number permitted in 1994, when the country’s population was 20 percent less than it is today. While multi-family housing may be better suited to meet the demand for walkable, transit-oriented neighborhoods, local zoning codes severely limit the locations where multi-family housing can be built. Consequently, the slowdown in single-family construction has contributed to a tightening of starter home inventory, which may be preventing some prospective millennial homebuyers from purchasing homes.

Multifamily share increasing fastest in the places where it was already high

The increase in the share of residential building permits comprised of multifamily units is a trend that holds true not just at the national level, but in each of the nation’s 25 largest metro areas.

While the multifamily category made up a greater share of new housing in all of the 25 largest metros, the size of the increase varies dramatically. The biggest jumps in the multifamily share have occurred in the nation’s densest metros, places that had already been building a significant amount of multifamily. The New York City metro experienced the biggest jump. In the pre-recession years from 1990 to 2005, multi-family comprised 44.8 percent of all building permits issued in the New York City metro — then the second-highest share among the 25 largest metros. In the mostly post-recession years from 2006 to 2018, that share spiked to 76.3.

“We see similarly large increases in other dense coastal metros, with Boston, San Francisco, Philadelphia, and San Diego rounding out the top five list for metros with the largest increases in the multifamily permit share. Notably, Philadelphia is the only metro among those five that has built enough new housing over the past decade to keep pace with job growth, according to our jobs-per-permit metric, and as a result has seen relative stability in their housing market,” Salviati writes in the report.

Phoenix is one of the metros building sufficient new housing to keep pace with jobs

There is a subset of metro areas that are thriving economically and building sufficient new housing to keep pace with job growth.

This group is primarily comprised of Sun Belt metros such as Phoenix, Dallas, Atlanta, and Charlotte. Notably, single-family is still the dominant type of new housing being built in these metros, and while the multifamily share is on the rise in these regions, the increases are much more muted than those observed in the dense coastal metros discussed above.

In Phoenix, for example, single-family accounted for nearly three-in-four new housing units permitted from 2006 to 2018. It seems that the metros most effectively meeting the demand for new housing are still primarily doing so by continuing to sprawl, despite an increasing demand for dense, walkable neighborhoods that prioritize sustainability.

In new multifamily construction, the ‘missing middle’ is still missing

These disparate patterns of residential development are playing out at a time when single-family housing has begun to face unprecedented criticism from both housing experts and policy makers. For the latter half of the 20th century, suburban single-family homes were synonymous with the popular understanding of the “American Dream.”

In recent years, however, a more nuanced view has emerged, which acknowledges that single-family zoning policies were often inextricably linked to redlining practices that served to explicitly enforce patterns of residential racial segregation. Single-family zoning also impedes the development of dense multifamily housing units, which can be an important source of market-rate affordable housing. Furthermore, denser cities are significantly more sustainable, and growing our cities with more dense development can play an important role in combating climate change.

Consequently, policy makers across the country are making efforts to enable multifamily development in areas that were previously reserved for single-family homes.

In 2018, an ambitious set of zoning reforms known as Minneapolis 2040 upzoned half of that city’s land in a way that aims to explicitly address patterns of racial and economic inequality. The city of Seattle also recently eliminated single-family zoning in a subset of its neighborhoods, and a statewide upzoning bill in Oregon has passed. In California, where the housing shortage is most acute, the upzoning bill SB 50 is currently stalled in the state senate, awaiting a vote next year.

Many of the zoning reforms described above strive to remove barriers to building a type of housing that has been referred to as the “missing middle.”

This type of housing — two- to four-unit buildings, accessory dwelling units, townhouses, and low-rise apartment buildings — can play an important role in increasing density and creating walkable neighborhoods, without affecting neighborhood character is the same way as mid- and high-rise apartment buildings. Despite the benefits of this type of housing, the multifamily housing that has been built in recent years increasingly takes the form of large apartment complexes.

Multifamily apartment buildings are increasing in size

We find that two- to four-unit properties made up just 3.0 percent of all housing units permitted in 2018. That share has been on a downward trajectory since 1990, when duplexes, triplexes, and fourplexes comprised 4.9 percent of residential permits. Two- to four-unit properties account for 8.0 percent of the nation’s total housing stock, indicating that this type of construction was far more prevalent in the past. Meanwhile, buildings with five or more units accounted for 91.6 percent of multifamily units permitted in 2018, and the average size of these properties has been steadily increasing. In 1990, the average number of units in buildings with five or more units was 13.6, but by 2018 that average building size more than doubled to 28.7, the report says.

While these large multifamily developments are an important form of new housing supply, they are usually confined to locations in and around the downtown areas of major cities.

Due to high construction costs — for land, labor, materials, and regulatory costs — developers build larger properties at luxury price points in order to achieve economies of scale and ensure that projects prove profitable. Zoning reform can remove bureaucratic hurdles to allow denser development in varying forms throughout a metro area.

Conclusion

“As millions of Americans struggle with housing costs, the issue has come to take center stage in both national and local politics. A number of 2020 Democratic frontrunners have issued policy platforms that address housing affordability, while cities and states across the country have begun to debate and enact fundamental reforms to their zoning codes,” Salviati writes.

“Much of this debate has centered on the need for dense, transit-oriented development in our nation’s cities. Dense housing plays an important role in maintaining inclusive housing affordability and cities developed in this manner are also significantly more environmentally sustainable.

“While we find that proportionally more multifamily housing has been built in recent years, the metros where it is most prevalent tend to be the coastal superstar cities that have struggled to build enough new housing overall.

“Meanwhile, fast-growing Sun Belt metros have continued to rely on single-family homes to maintain sufficient housing supply. These contrasting trends emphasize that decisions around what type of housing gets built and where are crucial to determining the future of America’s cities,” Salviati says in the report.

Chris Salviati is a housing economist at Apartment List, where he conducts research on economic trends in the housing market. Chris previously worked as a research assistant at the Federal Reserve and an economic consultant, and he has BA and MA degrees in economics from Boston University.