Seattle’s multifamily market continues to show strong fundamentals, exceeding national averages for most indicators, according to the summer report from Yardi Matrix.

Along with a healthy economy and robust population growth, the metro is recording impressive investment activity and steady apartment absorption despite a strong development pipeline, the report says.

“Although developers remain extremely busy, absorption is keeping up and there is little risk of overbuilding,” Yardi Matrix says in the report.

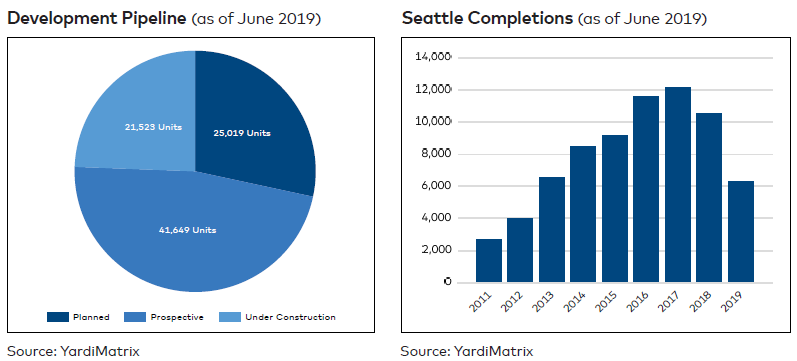

There were more than 21,500 units under construction as of June, with 8,131 expected to come online by December, in addition to the 6,314 apartments delivered in this year’s first two quarters. And although development is slated to hit another cycle peak, we expect the average Seattle rent to advance 3.9 percent in 2019.

Seattle’s multifamily market rent trends

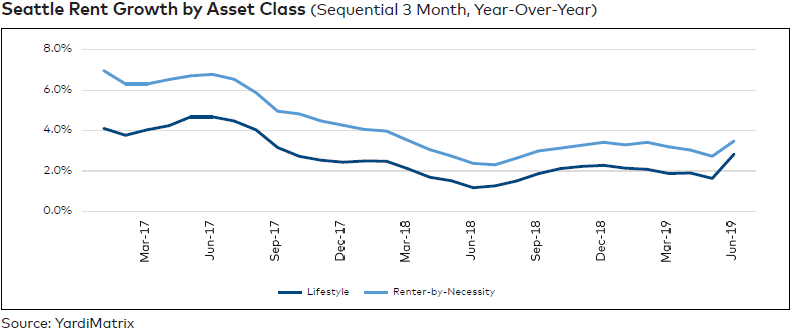

The average Seattle rent was up 3.1 percent year-over-year through June, 20 basis points below the national figure. The average rate stood at $1,920, well above the $1,465 U.S. average. At 1.3 percent as of June, Seattle recorded the highest rent hike among all major U.S. metros on a trailing three-month basis, reflecting refreshed strength despite a lingering development boom.

- Demand for working-class renter-by-necessity units continued to be robust, with rents in the class advancing 3.5 percent year-over-year through June, to $1,602. Meanwhile, the average lifestyle rent rose 2.8 percent, to $2,210. In the 12 months ending in May, the occupancy rate in lifestyle assets actually rose 10 basis points to 95.3 percent, while occupancy in RBN assets dropped 10 basis points, to 95.9 percent.

- Areas that used to be relatively affordable recorded some of the strongest hikes: Beacon Hill (10.4 percent), Factoria (8.1 percent), Woodinville/Totem Lake (6.9 percent). Bellevue–West ($2,674) and Belltown ($2,636) remained the most expensive, leading the 13-submarket list with average rents above the $2,000 mark.

- Despite continued strong supply, the overall occupancy rate in stabilized properties stood at 95.6 percent as of May, down just 10 basis points over 12 months. With demand expected to match supply across most submarkets, we expect the average Seattle rent to advance 3.9 percent this year.

Seattle multifamily supply

There were 21,523 units under construction across the metro as of June, with more than 8,000 expected to come online by year-end for a new cycle peak. Boosted by the metro’s expansion, developers added almost 50,000 units across nearly 300 projects since the beginning of 2015, three quarters of which are in upscale assets.

- Seattle’s construction boom showed no signs of stopping going into 2019 and developers brought online more than 6,300 units in the first half of the year. And while construction continues to focus on upscale product, the city’s economy is generating jobs across the board. This, in turn, is likely to put further pressure on low-income households.

- Although development is spread across the map, four submarkets accounted for more than 40 percent of all units under way as of June: Belltown (3,018 units), Redmond (2,580), Central (1,393) and First Hill (1,155). Belltown is also home to the metro’s largest projects under construction: Onni Real Estate’s 1120 Denny Way and Westbank Projects Corp.’s partially affordable 1200 Steward Street. The two upcoming communities total 2,178 units.

To learn more about Yardi® Matrix and subscribing, please visit www.yardimatrix.com or call Ron Brock, Jr.,

at 480-663-1149 x2404.

Related Story: Still ‘Room to Run’ In This Multifamily Growth Cycle Despite Looming Concerns

{kind=link}