Navigating the complexities of property management includes dealing with fair-housing claims, a task that becomes even more challenging when a claim of retaliation is added to the mix. This article aims to provide strategies and insights to help property managers and staff prevent fair-housing retaliation claims, ensuring a harmonious living environment for all residents.

Understanding Retaliation in the Housing Sector

Retaliation occurs when a resident, having filed a fair-housing claim, alleges that they are being mistreated in response to their claim. Retaliatory actions can vary widely but are united by their potential to exacerbate already-sensitive situations. For instance, consider a resident who has filed a fair-housing claim and subsequently submits a maintenance request. Prioritizing this request lower than others out of spite could escalate the situation, demonstrating apparent retaliatory behavior.

It’s crucial to remember that retaliation is unacceptable, regardless of the outcome of the original fair-housing claim. Effective training on fair-housing laws can play a significant role in preventing both the initial claim and any retaliatory actions that might follow.

Best Practices to Promote Prevention of Retaliation Claims

The cornerstone of avoiding retaliation claims lies in maintaining standard operating procedures for all residents without discrimination. Here’s how to approach a situation where a resident, perhaps feeling emboldened by their claim, starts to breach property rules or policies:

Enforce Rules Fairly: Do not disregard rule violations. Every resident must adhere to the property’s policies. The delicate nature of these circumstances may necessitate consulting with a fair-housing attorney to ensure that any actions taken do not seem retaliatory.

Fair-Housing Training: Continuous education for all staff members on fair-housing regulations is essential. This not only helps in avoiding initial claims but also in handling any situations that arise, without crossing into retaliation.

Documentation and Communication: If a complaint does arise, minimize direct interactions between the complainant and involved staff members. Document all interactions meticulously to provide a clear record of your response to the issue.

Proactive Measures to Help Prevent Fair-Housing Complaints

The most effective strategy to avoid fair-housing complaints is to create an environment where residents feel respected and valued. This involves:

– Ongoing Staff Training: Ensuring that all staff members, including property managers, understand fair-housing laws and how to apply them in daily operations.

– Transparent Communication: Maintaining open lines of communication with residents about their rights and how to address grievances.

– Responsive Management: Showing a willingness to address and resolve issues promptly and fairly can prevent many complaints from escalating.

Summary

Property management is indeed a complex field, rife with challenges that demand both tact and diligence. However, by adopting these best practices and dedicating themselves to continuous training, property managers can adeptly navigate the intricacies of resident relations with poise and assurance. This approach not only aims to circumvent potential legal pitfalls but also to cultivate an inclusive and welcoming community atmosphere.

In such an environment, every resident is not only afforded their rights but is also encouraged to engage and contribute, thereby fostering a sense of belonging and mutual respect. The ultimate objective extends beyond merely avoiding disputes; it’s about creating a living space where every individual feels valued, understood, and integral to the community fabric.

About the author:

In 2005, The Fair Housing Institute was founded as a company with one goal: to provide educational and entertaining fair-housing compliance training at an affordable price at the click of a button.

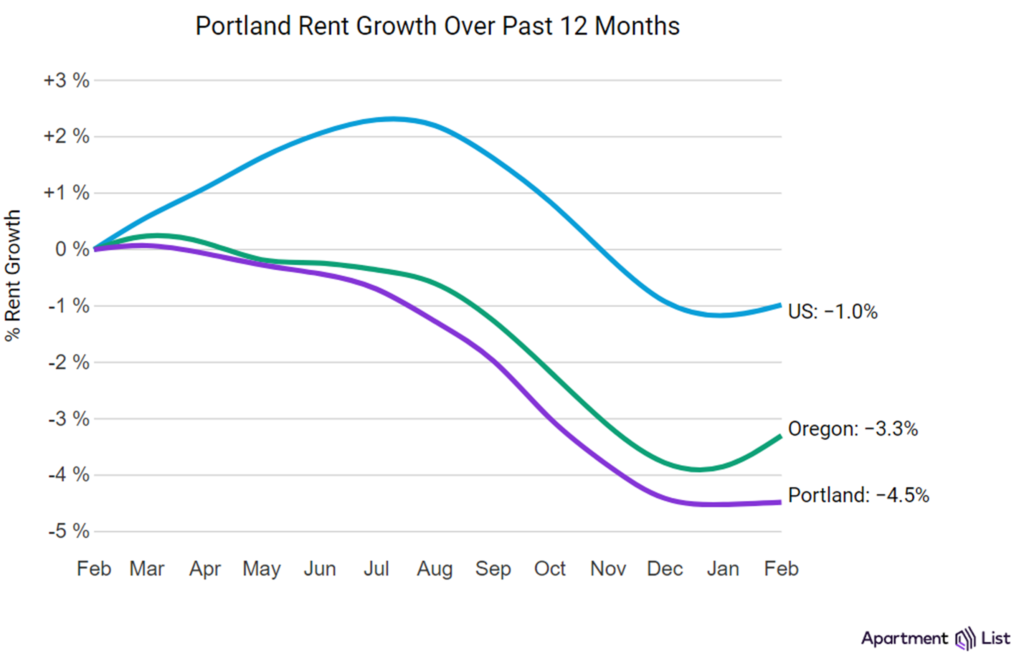

Portland rents continued flat in February for the second month and prices remain down 4.5% in the city year-over-year, according to the March report from Apartment List.

The overall median rent in the city is $1,531, roughly the same as in January.

Portland rent growth in 2024 pacing similar to 2023

Two months into the year, rents in Portland have risen 0.0%. This is a similar rate of growth compared to what the city was experiencing at this point last year: from January to February 202, rents had decreased 0.1%.

Portland is the 38th most expensive large city in the U.S.

Citywide, the median rent currently stands at $1,391 for a 1-bedroom apartment and $1,649 for a 2-bedroom. Across all bedroom sizes (i.e., the entire rental market), the median rent is $1,531. That ranks No. 38 in the nation among the country’s 100 largest cities.

Portland rents are 6.3% lower than the metro-wide median

Across the Portland metro, the median rent is $1,634, meaning that the median price in Portland proper ($1,531) is 6.3% lower than the price across the metro as a whole. Metro-wide annual rent growth stands at -4.0%, above the rate of rent growth within just the city.

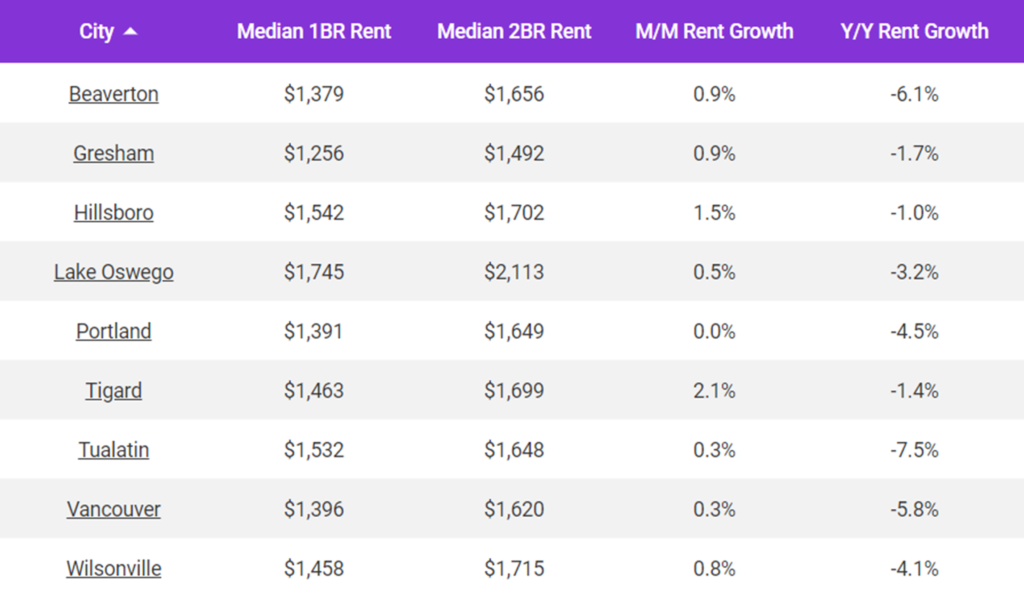

The table below shows the latest rent statistics for nine cities in the Portland metro area that are included in the Apartment List database. Among them, Lake Oswego is the most expensive, with a median rent of $1,993. Gresham is the metro’s most affordable city, with a median rent of $1,472. The metro’s fastest annual rent growth is occurring in Hillsboro (-1.0%), while the slowest is in Tualatin (-7.5%).

The bill, AB 2216, would prohibit banning pets in rentals and allow landlords to ask about pet ownership only after a tenant’s application has been approved, according to reports.

According to its author, Democratic Assembly member Matt Haney, the bill may be the first-in-the-nation law to require landlords to accept pets.

Haney said the intention is to bar property owners from asking about pets on applications, prohibit additional monthly fees for pet owners — or “pet rent” — and limit pet deposits. Haney says isn’t trying to force landlords to accept all pets. Instead, he said his bill will make it easier for pet owners to find an apartment by easing some of the restrictions they face.

The legislation, which is sponsored by the Humane Society of the United States, is aimed at solving a big problem Haney said he sees in the rental world: an overabundance of tenants with pets and a shortage of landlords willing to accept them.

“A two-tiered system that punishes people for having pets, or treats them differently, or has a greater burden on them just for that fact, should not be allowed in the law,” Haney told KQED. “What we see too often is just these blanket prohibitions of pets with no good reason for it, with no required justification for it and no protection of pet owners, who represent the majority of California’s renters, to be able to access housing just like anyone else,” Haney said.

“We never intended to say that landlords can place no restrictions at all,” Haney told POLITICO. “Nobody is going to be forced to take dangerous dogs … of course there’s going to be cases where restrictions make sense.”

Haney’s staff analyzed Zillow apartment listings and found that 20% of San Francisco apartments allowed cats and dogs of all sizes, while 18% of those in Sacramento and 26% in Los Angeles did. Survey research finds that two in three households nationwide own pets, and 72% of renters report that pet-friendly housing is hard to find.

Property owners, however, are already expressing concerns about the proposal. Krista Gulbransen, executive director of the Berkeley Property Owners Association, said her opposition comes down to risk: Pets have the potential to damage property, she said, and limiting owners’ discretion to take on that added risk while stripping them of the pet-deposit safeguard puts them in a terrible position.

“The biggest concern is just not being able to make that determination of risk and make a decision based on that,” Gulbransen said.

“There’s downsides every single time the Legislature does something, then they blame us because rents are going up,” Debra Carlton, executive vice president of state government affairs for the California Apartment Association told Politico. “It’s hard to get stuff built, and then they just regulate us.”

Politico said to be sure, Carlton still isn’t thrilled with all of the provisions of the scaled-back version, either. Not charging monthly for pets means landlords will just raise everyone’s rent to cover potential damages, especially if they can’t hike security deposits without running up against the cap on deposits that a different Haney bill last year instituted.

“Legislators are famous for doing the hard, hard, furthest thing from what they meant to do so that they force us to negotiate and they give us something we might not have wanted anyway,” said Carlton.

While rents are basically the same as they were about 18 months ago in most areas, “The stability on the surface belies a host of changing trends that are keys to determining the direction the market takes from here,” Yardi Matrix writes in the report.

Multifamily rents are creeping up as spring approaches, and many locations saw rents rise slightly in February, according to Yardi Matrix.

Metros in the Northeast and Midwest saw gains to counteract the rent declines in areas that saw strong new apartment inventory coming online.

Yardi Matrix says some of the Sun Belt metros have investors worried about the impact of new apartment unit deliveries.

Highlights of the Yardi Matrix February report

S. multifamily rents rose slightly in February, their first increase in seven months, in a sign that the market is stable. The average U.S. asking rent rose $1 during the month to $1,713, while year-over-year growth was unchanged at 0.6%.

The Northeast and Midwest continue to outperform over the short term, led by New York City. At 5.4%, the Big Apple not only leads major metros in rent growth over the last year but at 0.6% also was the top performer during the month of February.

Single-family rents slipped slightly, but fundamentals remain strong. Average single-family rents in the United States fell $2 in February to $2,133, while year-over-year growth fell 50 basis points to 1.2%. Rent growth was led by Boston, Raleigh and Orange County.

While rents are basically the same as they were about 18 months ago in most areas, “The stability on the surface belies a host of changing trends that are keys to determining the direction the market takes from here,” Yardi Matrix writes in the report.

Newly built apartments coming online are part of the story because, “Demand has remained healthy throughout the period that rents have been flat, as strong absorption was more than matched by an unusually high number of deliveries.”

Occupancy rates slide

“Occupancy rates will likely slide further, particularly in markets with large numbers of units under construction, as we forecast one million units to come online through the end of 2025,” the report says.

The report says the national occupancy rate was 94.5% in February, slightly down from the previous month and down 60 basis points year-over-year. Occupancy rates are either down or flat year-over-year in all but San Francisco (0.1%). Three Matrix top 30 markets are down by 1.0% or more: Atlanta (-1.2%), Indianapolis (-1.2%) and Austin (-1.0%).

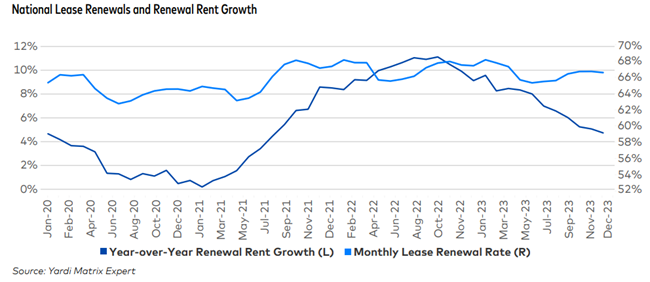

Renewals slow further

Renewal rent growth is slowing, in line with the deceleration in asking rents. Renewal rents, the change for residents that are rolling over existing leases, fell 4.6% nationally year-over-year in January, down 20 basis points from December.

The national lease renewal rate averaged 64.8% in January. This is the first time that the national renewal rate has fallen below 65.0% since July 2021, as the range for the last six months has been between 65.4% and 66.8%.

Yardi Matrix researches and reports on multifamily, office and self-storage properties across the United States, serving the needs of a variety of industry professionals. Yardi Matrix Multifamily provides accurate data on 18+ million units, covering more than 90 percent of the U.S. population. Contact the company at (480) 663-1149.

FTC: ‘Landlords and property managers can’t collude on rental pricing’

The Federal Trade Commission (FTC) and the U.S. Department of Justice have filed a joint legal brief saying price fixing by algorithm is still price fixing, according to a release.

“Landlords and property managers can’t collude on rental pricing. Using new technology to do it doesn’t change that antitrust fundamental. Regardless of the industry you’re in, if your business uses an algorithm to determine prices, a brief filed by the FTC and the Department of Justice offers a helpful guideline for antitrust compliance: Your algorithm can’t do anything that would be illegal if done by a real person,” write Hannah Garden-Monheit and Ken Merber in the FTC release in the business blog.

The legal brief highlights key aspects of competition law important for businesses in every industry:

You can’t use an algorithm to evade the law banning price-fixing agreements, and

An agreement to use shared pricing recommendations, lists, calculations, or algorithms can still be unlawful even where co-conspirators retain some pricing discretion or cheat on the agreement.

The FTC says in the release that “landlords increasingly use algorithms to determine their prices, with landlords reportedly using software like ‘RENTMaximizer’ and similar products to determine rents for tens of millions of apartments across the country.

“Efforts to fight collusion are even more critical given private equity-backed consolidation among landlords and property management companies. The considerable leverage these firms already have over their renters is only exacerbated by potential algorithmic price collusion. Algorithms that recommend prices to numerous competing landlords threaten to remove renters’ ability to vote with their feet and comparison-shop for the best apartment deal around.”

Agreeing to use an algorithm is an agreement

The FTC says “In algorithmic collusion, a pricing algorithm combines competitor data and spits out the suggested ‘maximized’ rent for a unit given local conditions. Such software can allow landlords to collude on pricing by using an algorithm – something the law does not allow in real life.

“When you replace once-independent pricing decisions with a shared algorithm, expect trouble. Competitors using a shared human agent to fix prices? Illegal.

“Doing the same thing but with an agreed-upon, shared algorithm? Still illegal. It’s also irrelevant that the algorithm maker isn’t a direct competitor if you and your competitors each agree to use their product knowing the others are doing the same in concert,” the FTC says in the release.

Price deviations don’t immunize conspirators

“Some things in life might require perfection, but price-fixing arrangements aren’t one of them,” the FTC says in the release.

“Just because a software recommends rather than determines a price doesn’t mean it’s legal. Setting initial starting prices or recommending initial starting prices can be illegal, even if conspirators deviate from recommended prices. And even if some of the conspirators cheat by starting with lower prices than those the algorithm recommended, that doesn’t necessarily change things. Being bad at breaking the law isn’t a defense.”

The rental housing industry is not alone

The FTC release says that the rental housing industry is not alone in using potentially illegal collusive algorithms.

“The Department of Justice has previously secured a guilty plea related to the use of pricing algorithms to fix prices in online resales, and has an ongoing case against sharing of price-related and other sensitive information among meat-processing competitors. Other private cases have been recently brought against hotels and casinos.

“Technology is a promise. Used correctly, it can make our lives healthier, safer, and more efficient. But its efficiency can also be used by bad actors to crush competition or bilk consumers in novel ways. No matter the tool law violators use, the FTC and the Department of Justice stand vigilant on the side of consumers and competition,” the release says.

Several lawsuits have been filed in different states against RealPage, Inc. and other major residential apartment landlords alleging price-fixing and conspiring to illegally raise rents

Hannah Garden-Monheit is director of the FTC’s Office of Policy Planning and Ken Merber is deputy assistant director of the FTC’s Anticompetitive Practices II Division.

One of the most significant multifamily challenges can be a weather event or another type of disaster, and failure to have a strategy in place can create chaos and confusion. The worst mistake any organization can make is to not have any defined emergency plans in place.

While challenges in the multifamily industry are inevitable, owners and operators can implement strategies to stay ahead of the game and overcome their effects.

By Gregory Lozinak

Anyone involved in the multifamily industry has witnessed the unique challenges this sector presents. Multifamily plays a vital role in providing housing solutions for individuals and families, which means the stakes are high, and the industry is not without its hurdles. A lack of preparation can lead to disaster or even tragedy.

One of the most significant challenges can be a weather event or another type of disaster, and failure to have a strategy in place can create chaos and confusion. This can significantly and severely impact the outcome of any emergency. Another hurdle is the changing regulatory environment. Laws and regulations regarding resident rights, fair-housing practices and building codes can vary from state to state and are subject to change on the fly. Staying compliant with these regulations can be a daunting task.

The potential for resident disputes and conflicts, whether it’s complaints, maintenance issues or disagreements over lease terms, is always present. Managing these relationships requires skill, diplomacy and timeliness to maintain a community’s reputation and ensure resident satisfaction. Financial considerations also pose a constant challenge in the industry. Even modest missteps can quickly turn costly and further damage reputation. It’s likely not a matter of “if” properties will face these risks, but rather “when.”

The potential for resident disputes and conflicts, whether it’s complaints, maintenance issues or disagreements over lease terms, is always present.

The Consequences of Missteps

When it comes to disasters, the lack of a solid set of policies and procedures can result in injury, fatalities and greater property damage and related costs. A comprehensive disaster strategy reduces risk and protects lives.

Failure to comply with regulations can result in fines, legal action and potentially more turmoil. Unresolved resident disputes can generate negative reviews, which significantly affects the reputation of a community and harms an onsite team’s ability to generate quality leads. Financially, missteps can lead to legal fees, court settlements and increased insurance premiums, all of which quickly affect net operating income.

It is vital to recognize that the consequences of these missteps extend far beyond the immediate financial impact and can erode the long-term success of a portfolio. Fortunately, owners and operators can take proactive measures to reduce costly risks.

Proactive Measures for Potential Hurdles

The worst mistake any organization can make is to not have any defined emergency plans in place. This is a recipe for disaster in any situation. Taking proactive measures to safeguard properties and protect residents is essential. This is accomplished by implementing a comprehensive risk-management strategy that can minimize the likelihood of encountering hurdles and mitigate the impact when they do arise:

Build a strong foundation of policies: One of the first steps is establishing a solid foundation of policies. These should outline clear guidelines for all activities in the community, including resident communication and team protocols. Well-documented policies set expectations for both residents and teams, reduce the potential for misunderstandings and ensure consistency throughout operations.

Ongoing training for teams and residents: Providing ongoing, regular training sessions helps make certain that everyone is aware of the latest regulations, best practices and procedures for addressing common challenges. By investing in professional development, teams are empowered to navigate hurdles and make informed decisions effectively. Property teams also need to continually train residents on disaster preparedness and the community’s plan for any incidents.

Easy access to policies and procedures: The potential for risk increases if teams find it difficult to locate the required information for any incident or issue they encounter. Policies and procedures should be available electronically and readily accessible from any device. This method also pushes updates company-wide, so associates don’t miss important changes.

Establish a chain of communication: When it comes to disasters, property managers need to be able to establish contact quickly and know who to contact. Creating a chain of communication saves valuable time and makes disaster management more effective. Make sure the established system is clear and all team members know their roles and responsibilities.

Support for compliance and mitigation: It is crucial to have support for compliance and risk mitigation efforts. Regular audits to assess adherence to policies, maintaining open lines of communication to address concerns promptly and partnering with legal and insurance professionals who specialize in multifamily, are helpful steps to boost compliance and assessment. It is also crucial to monitor on-property activity to identify and address potential issues before they escalate.

Strategies for Staying Ahead

While multifamily challenges in the industry are inevitable, owners and operators can implement strategies to stay ahead of the game and overcome their effects:

Embrace technology: Using technology streamlines operations and enhances efficiency in managing policies, procedures and properties. Management software and services can automate many repetitive and high-risk tasks, which can mitigate errors and improve resident satisfaction. Digital communication tools facilitate effective outreach efforts, mitigating potential confusion.

Foster a culture of open communication: Encouraging open communication between associates and management, as well as residents and teams, is essential for identifying and addressing potential issues early on. Establish channels for residents to voice their concerns, whether it’s through online portals or regular meetings. Do the same for employees company-wide. Fostering a culture of open communication creates a supportive environment that minimizes the likelihood of conflicts escalating into major hurdles.

Stay informed and adapt: The regulatory landscape in the multifamily industry is constantly evolving. Stay informed about changes and adjust policies and procedures accordingly. Failure to comply with regulations can carry heavy financial penalties in some cases. After updates to policies, it’s important to follow up with teams to make sure they know and understand the changes.

Employ third-party services: Creating and updating policies and procedures, as well as the related training, can be a monumental task, and mistakes are possible for those unfamiliar with the process. Consider the use of an organization experienced in knowing the changes, crafting the needed policies and keeping employees informed.

By building a strong foundation of policies, providing ongoing training and seeking continued support for compliance and risk mitigation, owners and operators can stay ahead of the game and guard against risks. Embracing technology, fostering open communication and staying informed about industry changes are additional strategies to ensure long-term success. Even the smallest misstep can have significant consequences, so it is essential to prioritize risk management and take the necessary steps to safeguard operations.

About the Author

Gregory Lozinak is the senior vice-president of account management at Grace Hill, joining the team in 2023. Having spent most of his career as a senior operations executive, Greg has a strong track record in commercial and multifamily real estate investment management, delivering above-benchmark investment returns.

Grace Hill provides industry-leading SaaS technology solutions designed to make a positive impact in real estate and improve the lives of people where they work and live. Harnessing years of real estate experience and the understanding that people are better together, Grace Hill helps owners and operators increase property performance, reduce operating risk and grow top talent.

The landscape for green technology is changing. Awareness of highly efficient electric heat pumps has been growing, and heat pump systems have now outsold gas furnaces for two years in a row. We’re witnessing new innovations in solar and storage. And government agencies continue to roll out funds—for weatherization, beneficial electrification, energy storage, etc.—from the Inflation Reduction Act (IRA) and Bipartisan Infrastructure Law (BIL). In addition to improving efficiency and cutting costs, these solutions can increase resilience and stability in the face of extreme temperatures and natural disasters.

IRA and BIL funds can be used to offset project costs to the extent that a holistic green retrofit requires little to no investment from the owner. Some of the new funding is already in circulation, but there is still an opportunity to influence the funds that have yet to be released because the administering agencies are still developing their plans and designing their programs. One consistent pain point for program administrators and service providers is coordinating various funding sources to effectively serve multifamily properties. While there is a great deal of potential and value in this activity, it has historically been hindered by barriers such as:

There are different requirements attached to various funding sources, which can be very burdensome for service providers attempting to coordinate funds while ensuring compliance.

Currently, there is insufficient collaboration within and between agencies, utility companies, etc. to improve the guidance that is available for leveraging multiple financial resources.

Financing institutions that can provide energy financing are too often overlooked partners in the design of projects and programs, even though their networks, existing project pipelines, and/or expertise can be crucial to project execution.

The multifamily community needs to push for increased collaboration, and for programs to leverage the expertise of multifamily specialists. For those that are unsure how to begin, ICAST has created a dedicated webpage that can serve as a starting point for advocacy efforts.

About the author:

Ryan Kristoff is the Vice President of Grant Programs at ICAST, a national nonprofit that designs holistic retrofit solutions for multifamily affordable housing (MFAH). He works with local government, utility, state, and federal partners to create and launch MFAH-focused clean energy programs.

The valley-based SMI Property Management firm has expanded services to the Greater Portland area, according to a release.

Portland-based JPM Real Estate Services has joined Willamette Valley-based, SMI Property Management.

“The friendly merger means that SMI will expand its industry-leading services into the greater Portland area, while maintaining all staff and properties served by JPM.

“We are excited about this new opportunity to provide property owners with our wide-range of management services and to help renters find fair-priced, accessible housing in the greater Portland area,” said Gabe Johansen, President and CEO of SMI Property Management. “We have served Salem and the Willamette Valley for 48 years and are honored to bring our customer-centered services to the diverse communities in greater Portland metro.”

“SMI is poised to expand its first-class level of client care to Portland and the surrounding communities in the first quarter of 2024. The merger brings more than 2,100 units into SMI’s management portfolio. SMI will now manage more than 5,400 multifamily units from Corvallis and Albany through Salem and Keizer up to Portland, Tigard, Beaverton, Gladstone, Canby, and communities in between. SMI also manages approximately 50 commercial office and retail properties in the mid-Willamette Valley.

“One of the keys to success to this growth strategy is adding JPM’s 60 relationship-focused professionals to the SMI team,” said Johansen. “For 20 years, JPM consistently met the needs of their clients by providing accountable and personalized service. I respect their customer-centered approach and am thrilled to have them join SMI,” according to the release.

With the merger with JPM Real Estate Services and their 60 employees, SMI Property Management will now provide jobs and benefits to approximately 160 employees. These jobs are a mix of highly trained portfolio managers, apartment community managers, and skilled maintenance teams.

“Throughout SMI’s 48-year history, it has provided a full-range of management services to property owners – tenant placement, property inspections, regular property maintenance, 24-hour emergency services, rent collection, marketing of vacancies, and financial reporting. SMI collaborates with property owners to prioritize fair pricing, accessibility and equity for current renters and business owners.

“For renters, SMI Property Management works with people who are seeking housing to find a home that matches their location, size, and budget requirements. Upon request, SMI managers collaborate with large employers, government housing authorities, and community services to identify appropriate housing,” according to the release

Visit SMI Property Management to learn more about SMI’s tenant-based and owner-based services or to see a list of vacancies and resources for renters.

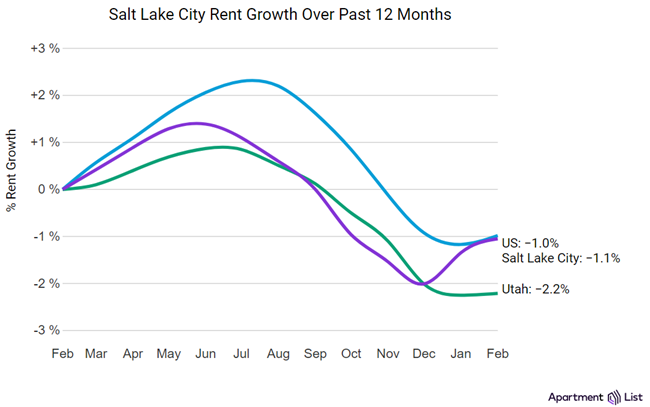

The median rent in Salt Lake City rose by 0.3% over the course of February, according to the March report from Apartment List.

Currently, the overall median rent in the city stands at $1,324, roughly the same as last month. Prices remain down 1.1% year-over-year.

Rent growth in 2024 pacing similar last year

Two months into the year, rents in the city have risen 0.3%. This is a similar rate of growth compared to what the city was experiencing at this point last year: from January to February 2023 rents had increased 0.5%.

Rents are 11.2% lower in city than the metro-wide median

Across the metro area, the median rent is $1,491 meaning that the median price in Salt Lake City proper ($1,324) is 11.2% lower than the price across the metro as a whole. Metro-wide annual rent growth stands at -2.4%, below the rate of rent growth within just the city.

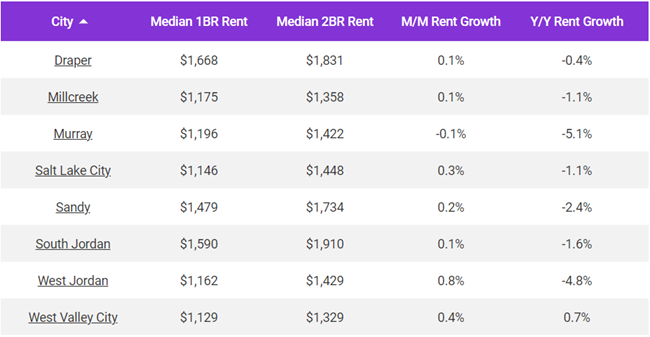

The table below shows the latest rent stats for 8 cities in the metro area that are included in our database. Among them, Draper is currently the most expensive, with a median rent of $1,887. Salt Lake City is the metro’s most affordable city, with a median rent of $1,324. The metro’s fastest annual rent growth is occurring in West Valley City (0.6%) while the slowest is in Murray (-5.1%).

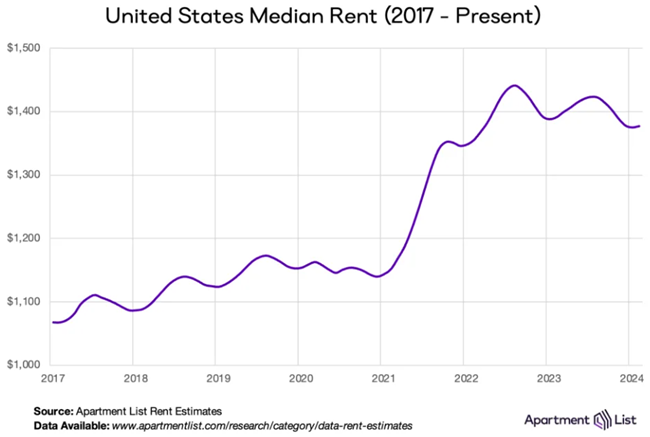

National rent prices finally moved up slightly in February after six months of declines, according to the March report from Apartment List.

“This turnaround is in line with the rental market’s typical seasonal pattern, as we transition into the time of year when moving activity starts to gradually pick back up after bottoming out around the holidays,” the Apartment List Research Team writes in the report.

Rent prices ticked up 0.2 percent in February and currently the nationwide median rent stands at $1,377.

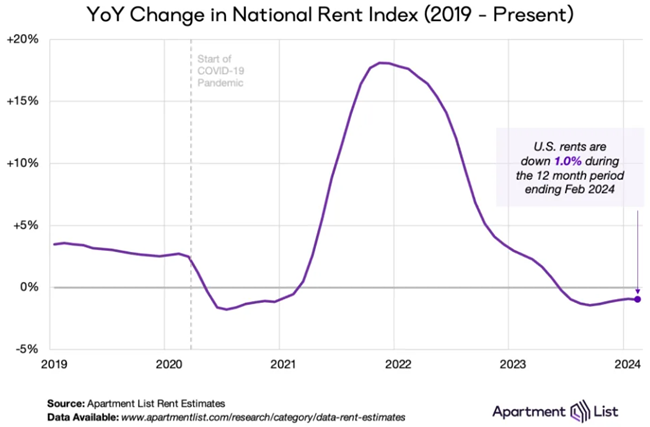

Rent inflation is receding

The Apartment List report says the rental market slowdown in gradually showing up in inflation numbers and has been visible in their reports over the past few months.

While the apartment rental market has cooled and apartments are generally less expensive than a year ago, the national median rent is still more than $200 per month higher than it was just three years ago which has contributed to inflation numbers.

The Wall Street Journal reports in an article that rent costs have been driving inflation numbers for months in official federal data. Prices in other areas may be responding to the Federal Reserve interest rate increases but rent costs are not.

“So, it’s been a bit of a mystery to economists why rent hasn’t followed suit. That’s especially because almost every data source, except the consumer price index kept by the Bureau of Labor Statistics, shows that those costs actually are cooling significantly — or even falling — since growth peaked early last year,” the Wall Street Journal reports.

Part of the problem with measuring rents and inflation the way the government tracks data is that a rental unit is only captured in the government surveys every six months, even if the rent changed during that period. The Bureau of Labor Statistics tracks rents for all tenants, not just those starting new leases — people staying put for a year or more might not see their costs change as rapidly.

But economists and others are not sure why the difference remains so pronounced month after month.

“We’re watching a big mountain of snow melt, and every 10 minutes, we look and there’s still a big pile of snow,” said Igor Popov, chief economist at Apartment List told the Washington Post. “We’re just watching it so carefully it doesn’t feel like we’re seeing much progress.”

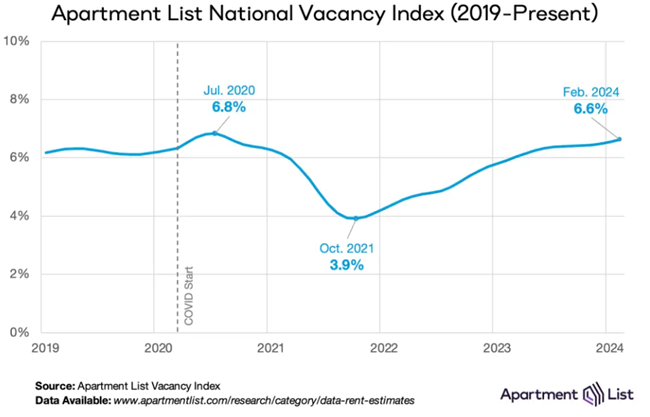

Vacancy continues rising

“On the supply side of the market, our national vacancy index continues trending up and stands today at 6.6 percent. And with this year expected to bring the most new apartment completions in decades, we expect that there will continue to be an abundance of vacant units on the market in the year ahead,” the report says.

What Lies Ahead?

“Historical seasonal patterns suggest that rents will continue trending up for the coming months, but we expect future rent increases to be moderated by a robust construction pipeline delivering new units throughout the year.

“With consumer sentiment about broader macroeconomic conditions beginning to improve, it’s possible that rental demand will also rebound in the year ahead, but likely not to an extent that would outweigh the impact of all the coming supply,” the report says.