Salt Lake City rents have increased 1.0 percent over the past month according to the latest report from Apartment List.

Rents in the city have increased slightly by 0.7 percent year-over-year.

Currently, median rents in Salt Lake City are $927 for a one-bedroom apartment and $1,185 for a two-bedroom.

This is the second straight month that the city has seen rent increases after a decline in December of last year. Salt Lake City’s year-over-year rent growth lags the state average of 3.1 percent, but exceeds the national average of -0.8 percent.

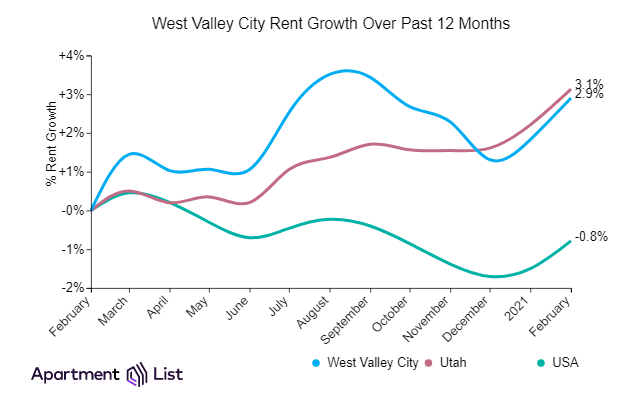

West Valley City rents also increase sharply

West Valley City rents have increased 1.1% percent over the past month, and are up moderately by 2.9 percent in comparison to the same time last year.

Currently, median rents in West Valley City are $1,056 for a one-bedroom apartment and $1,245 for a two-bedroom.

This is the second straight month that the city has seen rent increases after a decline in December of last year.

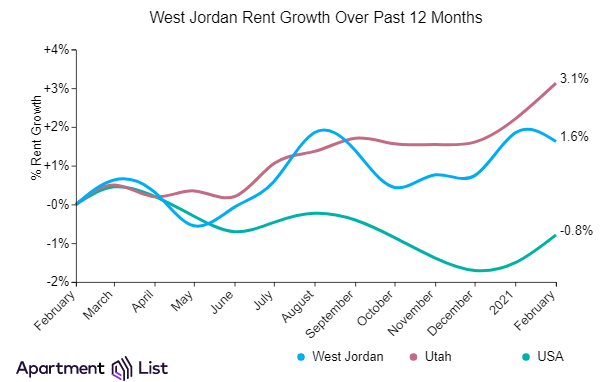

West Jordan rents declined slightly over the past month

West Jordan rents have declined 0.2 percent in February.

However rents are up by 1.6 percent year-over-year.

Currently, median rents in West Jordan are $1,156 for a one-bedroom apartment and $1,408 for a two-bedroom.

Apartment rents trending up nationally

“This month’s data represents the clearest indication yet that rent prices are rebounding in markets across the country,” Apartment List said in the report. “For comparison, in the previous three years, the average month-over-month rent growth in February was 0.3 percent. In other words, the month’s increase was more than double the prior-year average for this time of year.

“The data continue to exhibit significant regional variation, but the days of plummeting rents in pricey coastal markets appear to be coming to an end, with cities such as San Francisco and Seattle experiencing positive month-over-month growth for the first time since the start of the pandemic.”

The national rent index is up by 0.7 percent month-over-month, representing the second straight month of positive rent price growth and the largest monthly increase since June 2019 when the market was in the middle of the summer boom, according to the Apartment List national monthly report.

“This month’s data represents the clearest indication yet that rent prices are rebounding in markets across the country,” Apartment List said in the report. “For comparison, in the previous three years, the average month-over-month rent growth in February was 0.3 percent. In other words, the month’s increase was more than double the prior-year average for this time of year.

“The data continue to exhibit significant regional variation, but the days of plummeting rents in pricey coastal markets appear to be coming to an end, with cities such as San Francisco and Seattle experiencing positive month-over-month growth for the first time since the start of the pandemic.”

The rent index report says the latest month appears to be the month where steep rent declines are bottoming out, but booming markets are continuing to see prices climb, such as many of the mid-sized markets that have seen rents grow rapidly through the pandemic, showing that there’s still steam left in the current boom.

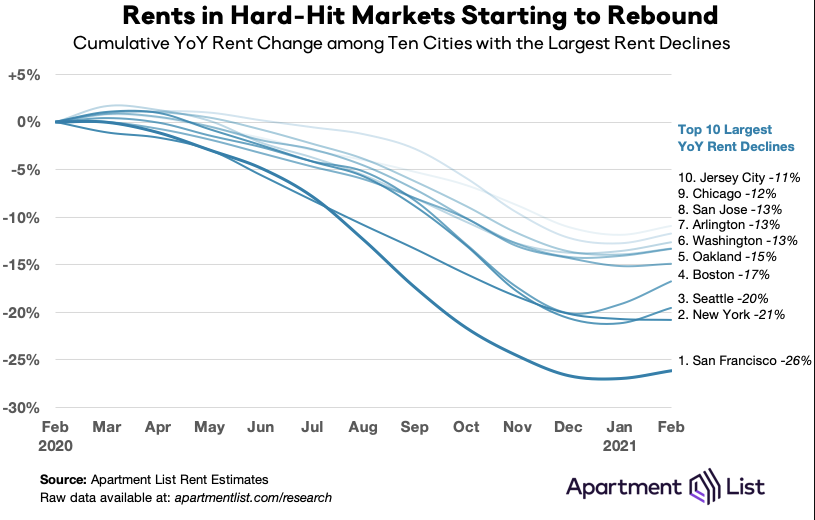

Big Cities with Sharp Rent Declines Show Positive Growth

Nine of the 10 cities with the sharpest year-over-year rent declines experienced positive rent price growth this month, the Apartment List rent index report shows.

For five of these cities, this was the first monthly increase since the start of the pandemic, while the other four are continuing a trend that began last month. In Boston, rents jumped by 3 percent month-over-month, the largest increase among the nation’s 100 largest cities. New York City is the only market on this list where rents continued to fall this month, but even there, the decline was just 0.1 percent, compared to an average monthly decline of 2.4 percent in the preceding nine months.

Rent Index Conclusion

“Since the start of the COVID-19 pandemic, we have witnessed significant disruptions to rental markets across the country. Social distancing and remote work changed what people want in a home, while many renters were thrust into immediate and unexpected financial hardship as layoffs and furloughs rippled through the economy.

“These sudden changes to budgets and preferences led to a convergence in rental prices across the U.S. – the most expensive markets saw rents fall rapidly while a number of more affordable mid-sized cities experienced accelerating rent growth.

“This month’s data indicates that the markets where rents have been falling rapidly have reached a turning point. The booming markets are still seeing prices rise, but in many cases, that growth is flattening somewhat. While remote work and economic fallout of the pandemic will undoubtedly continue to impact local rental markets going forward, the way that these trends continue to play out may now start to become more nuanced and gradual,” Apartment List said in the report

The Landlord Compensation Fund is now accepting applications in Oregon to assist landlords with the massive amounts of unpaid rent that currently exist.

Regular readers of this series likely noted last month’s mention of the Landlord Compensation Fund, a key piece of the recent House Bill 4401. As that article was drafted, the Landlord Compensation fund had not yet materialized. Shortly after it was published, the wheels began to turn. As of this article’s drafting, the Landlord Compensation Fund is now accepting applications to assist landlords with the massive amounts of unpaid rent that currently exist.

It is important to note that landlords are not automatically eligible for the fund. Landlords must submit completed Declarations of Financial Hardship forms, procured directly from the tenants, who owe rent for any or all months since April 2020. This presents challenges related to getting the forms from some tenants who either (a) refuse to communicate, (b) do not believe they owe rent, or (c) do not believe they should have to assist the landlord in getting the rent they owe. In these instances, landlords now have options.

First, HB 4401 allows for a balance-due notice, with which the landlord must include both the declaration form and the notice of tenants’ rights form, in order to comply with the statutory requirements. While a balance-due notice is not a requirement for unpaid rent to remain due and owing, it creates a viable method for landlords to get the declaration form in front of tenants and perhaps jump-start the conversation.

While many landlords use this approach, it is important to note that landlords should be cautious in their communications with their tenants. There is no statutory definition or form for what constitutes a balance-due notice. That ambiguity provides an opportunity for tenants to argue that certain written communications to the tenant may qualify as a de facto balance-due notice. If a landlord does not include the declaration form and notice of tenants’ rights with that innocuous communication—because they may not believe it to be required—potential issues could result.

Landlord compensation fund and tenants who refuse

The other option provided for in HB 4401 for tenants who simply refuse to provide the declaration form is the service of 10-day non-payment-of-rent notices. While landlords should consult legal counsel to assist in the crafting of these notices, it is imperative to note that these notices, when served, must also include the declaration form and notice of tenants’ rights. Once the tenant is served with the notice, they can return the declaration form, at which time (a) the landlord must cease their eviction process, and (b) the tenant’s grace period and emergency period are extended through June 30, 2021. In other words, if the form is returned, they will have until June 30, 2021 to repay the landlord and cannot be evicted through that date, but the landlord now has their declaration form, with which they can apply to the fund.

If the tenant still refuses to return the form, a landlord could file an eviction action with their non-payment notice. The summons of any eviction filed must include the declaration form and notice of tenants’ rights, as per HB 4401. The failure to do so renders the landlord’s eviction action defective, extends the grace period and emergency period by law, and presents exposure. However, the required inclusion of this form provides the tenant another opportunity to return it to the landlord to access the fund and avoid eviction and payment.

Oregon landlord compensation fund downsides

It is also important to keep in mind the downsides to the Landlord Compensation Fund in Oregon.

Oregon has unveiled a scoring system to determine how funding is distributed, prioritizing smaller landlords with the largest amount of unpaid rent. Landlords also cannot evict tenants without cause or for non-payment through the pendency of the distribution application, a time frame which is currently unknown. This could interfere with a landlord’s plans to potentially sell the property or have a family member move in. Oregon landlords must also provide the state with any documents they request related to the application. Finally, 20 percent of the tenant’s unpaid balance must be forgiven.

Landlords are not required to engage in the compensation fund. Once the moratoriums lift, landlords could technically sue their tenants for the unpaid amounts. However, if your tenant has been affected by COVID-19, the fund may be a landlord’s one opportunity to recover some of those amounts, provided the funding meets the need. Given the scope of the need, that is unlikely to be the case.

Bradley Kraus, Portland attorney

Brad Kraus is a partner at Warren Allen LLP. His primary practice area is landlord/tenant law, but he also assists clients with various litigation matters, probate matters, real estate disputes, and family-law matters. A native of New Ulm, Minnesota, he continues to root for Minnesota sports teams in his free time. You can reach him via email [email protected] or 503-255-8795.

Ask the attorney is a new feature we are starting with month with attorney Bradley S. Kraus over how to terminate a lease. If you have a question for him, please feel out the form below.

Ask Attorney Brad:

I have tenants on a month-to-month occupancy. They have been there two years.

Since the pandemic began, they have told me that they do not have to pay the rent or late fees and I cannot do anything about it. They have paid the rent late, up until February, which they will not pay.

Meanwhile, they have obtained cats and several chickens. They refuse to complete the pet agreement or pay the pet fee.

They signed a no-smoking addendum that covers the entire property, but continue to smoke outside the home (this will be difficult to prove). If I sit outside to take a picture I’ll be breaking the law for harassment.

They requested to have someone else move into the home with them, which I denied. They claim they have not done this, but there are now four cars there on a daily basis (they claim that all are theirs). Yet all four cars are gone each morning when I drive by on my way to the office.

I believe they have moved in their grown child, husband, and two children, but I can’t prove it.

I have served them with notice regarding unauthorized pets, smoking and unauthorized occupants; the only thing they admit to is the chickens.

Do I have enough to terminate a lease with cause, considering I can’t prove smoking or unauthorized occupants?

– Yvonne

Dear Yvonne:

There are a lot of items worth addressing in your prompt. I’ll try to cover all of them.

First, while it’s true that during the emergency period as set forth in applicable law that late fees could not be charged, that emergency period may or may not currently apply to you. For example, if your tenants have turned in a declaration of financial hardship, it would. If they have not, you may be able to charge them late fees for their late payments in 2021.

With regard to the rest of the items you describe, these are all potential defaults of the rental agreement, and the language of your rental agreement will control that. If you have a solid rental agreement, which contains prohibitions against unauthorized pets without landlord consent, smoking, unauthorized occupants or . . . chickens, you may have rights. Having a seasoned attorney evaluate the same will be important to determine whether or not you have rights on that point.

As to your final question, whether or not you have enough evidence to explore whether you can terminate a lease depends on your proof.

Remember, if your termination notice is challenged, you have the burden of proving those defaults. That means bringing in witnesses to testify based upon personal knowledge about those items. For things like smoking and unauthorized occupants, it may prove challenging. If the tenants admitted to having unauthorized chickens, that admission may be used against them.

In short, you may know that the tenants are violating the rental agreement. But in court, it’s not about what you know . . . it’s what you can prove.

Sincerely,

Brad Kraus

Brad Kraus is a partner at Warren Allen LLP. His primary practice area is landlord/tenant law, but he also assists clients with various litigation matters, probate matters, real estate disputes, and family-law matters. A native of New Ulm, Minnesota, he continues to root for Minnesota sports teams in his free time.

Ask Attorney Brad

Please enter your rental housing management question below for Ask Attorney Brad Kraus. Unfortunately he cannot answer questions from tenants.

Here are 5 ways manufactured-housing communities, especially in hard-hit California, can reduce wildfire threats.

By Matthew Davies

Following years of wildfire devastation that destroyed 8,100 dwellings, many California homeowners are facing a new threat: a lack of affordable and adequate home-insurance coverage.

The Camp Fire that spread through Paradise, California in 2018 caused more than $9 billion in losses to insured property. In response, insurers refused to renew insurance policies for 235,250 homes in 2019, a 31 percent increase from the previous year. In zip codes with a moderate to very high fire risk, the rate of non-renewals jumped to 61 percent.

This move prompted Insurance Commissioner Ricardo Lara to issue a moratorium on insurance non-renewals in December 2019. That moratorium still exists today, giving needed protections to homeowners at risk of losing coverage. But what happens when manufactured homes, which don’t legally require insurance, are damaged by fire?

As the owner and operator of a manufactured-housing community, here are five things you can do to help homeowners in your communities prepare for natural disasters like wildfires.

1. Require insurance for all residences in your community in the lease agreement

Though insuring a manufactured or tiny home is not required by law, some property management companies require homeowners to insure their homes whether they occupy or rent them. Most mortgages require insurance, though some manufactured homeowners may own their home outright, meaning they may opt out of coverage unless it is required by their community. Tiny homes, while more affordable than their larger, site-built counterparts, still cost an average of $60,000, making them an investment worth protecting.

2. Understand what is and isn’t covered

When it comes to natural disasters, some companies exclude different types of damage – like fire or flood damage – in certain high-risk regions, so it’s important to confirm wildfire coverage. Standard residential insurance policies will cover damage from fire and smoke, including:

Damage to the dwelling structure and additional structures;

Landscaping and backyard items;

Reimbursement for the cost of temporary housing, such as a hotel or apartment if the home is deemed unlivable during repairs;

Removal of debris;

Upgrades intended to bring the home up to current building-code standards; and

Personal property.

3. Include tree and brush removal in your manufactured community’s routine maintenance plan

Or also require that residents remove or reduce fire hazards from the property in the lease.

Wildfires can spread quickly through brush and limbs, so whenever possible, create what foresters call “defensible space” around the homes in your community. This includes clearing away brush, trees, long grasses, and bushes adjacent to the home; lopping off low tree limbs; and removing leaves from gutters.

Since 2005, California has required homeowners who live in high-risk areas to maintain a 100-foot defensible space – that is, free of flammable materials such as brush and vegetation – around their homes. Since 2008, California law also requires new homes to be constructed with fire-resistant materials such as dual-pane windows, fire-resistant roofing, and enclosed eaves. While this amount of space may not be feasible in manufactured-housing communities, you can still take steps to ensure that fire hazards are kept as far away from dwellings as possible.

Find a list of other tips on making homes wildfire-ready here.

California’s Mobilehome Parks Act requires every park to have a representative accessible by phone or in person to respond to emergencies.

4. Establish an evacuation plan

Create an evacuation plan that takes into consideration the density of the park and the age and mobility of residents. The plan should include emergency-contact lists and a list of residents with special needs or disabilities who may need assistance in an emergency. A template evacuation plan can be found here.

Further, California’s Mobilehome Parks Act requires every park to have a representative accessible by phone or in person to respond to emergencies. In parks with more than 50 units, a representative should reside onsite. Finally, when feasible, having two exits from busy parks can prevent bottlenecks in the event of an evacuation during a wildfire threat.

5. Research before you buy

Before you invest in a new community, assess the site’s wildfire threat risk. You can view maps and zip-code listings of areas with the highest wildfire risk exposure on the HUD website. If a property is surrounded by forest or seated on a slope where a wildfire is likely to run, it’s particularly important to do your due diligence.

Scientists anticipate the danger of wildfires will increase as the climate changes, leaving millions of homes in heavily forested areas of the western United States vulnerable. The time to act is now.

About the Author: Matthew Davies is the founder of Stockton, CA-based Harmony Communities, which owns and operates thirty-eight manufactured-housing communities in the western United States. An investor and community-development professional working for affordable housing solutions, Davies’ goal is to help bring the opportunity for homeownership to people in his home state who otherwise could not afford to buy a home.

This week the question for Ask Landlord Hank is about a hoarder and whether an eviction can happen during covid-19. Remember Hank is not an attorney and is not giving legal advice so check your local ordinances.

Dear Landlord Hank:

How can I evict a hoarder during COVID-19?

–Valerie

Dear Landlord Valerie:

If your tenant is truly a hoarder, then they may be protected under the Fair Housing Act, as hoarding is considered a mental disorder that is recognized by the American Psychiatric Association.

So you won’t be able to evict for hoarding.

Also, you need to be able to tell the difference between hoarding and being a slob and poor housekeeper.

Hoarding normally goes way beyond being messy and disorganized and having too much stuff. Often there is only a narrow walkway to get through the property as you wind through mountains of items.

Are entry and exits blocked, are items blocking ventilation, or have food items began attracting rats and vermin?

If the tenant has been paying rent, there may be an eviction moratorium as well.

Please contact a local attorney who deals in landlord/tenant law to see where you stand and what options you have with a hoarder.

If you truly think the property condition is a safety hazard, try for photo documentation, then contact your local fire department and health department for guidance.

Be respectful of your tenant, and don’t threaten them. That will only make matters worse.

Sincerely,

Hank Rossi

Landlord Hank says, “If your tenant is truly a hoarder, then they may be protected under the Fair Housing Act, as hoarding is considered a mental disorder that is recognized by the American Psychiatric Association. So you won’t be able to evict for hoarding.”

Ask Landlord Hank Your Question

Ask veteran landlord and property manager Hank Rossi your questions from tenant screening to leases to pets and more! He provides answers each week to landlords.

The Environmental Protection Agency increasing focus on recycling of bulk materials, so camera technology helps apartment communities document waste diversion rates to impress investors, meet corporate goals, satisfy mandates.

By Paul Bergeron

Commercial and residential real estate companies continue to direct more focus on waste diversion, paying attention to recyclable materials that might not fit their local collection criteria for recycling or donation such as small electronics, clothing, toys, housewares and even furniture.

With the Environmental Protection Agency (EPA) and local mandates in many major markets calling for reduced waste diversion, smart cities are rethinking what is sent to landfills and are looking for solutions on how to reuse and recycle as much as possible. Bulk-item pickup can prove costly and involve inconsistent pick-ups by waste collectors.

Reusing and repurposing these materials can prevent the waste of potentially useful materials and reduce the consumption of fresh raw materials, thereby reducing energy usage, air pollution and water pollution from landfills.

Multifamily and retail property owners are seeking efficient ways in which to manage this process, including properly documenting their diversion to satisfy the growing list of environmentally friendly policies that their company, residents and tenants desire – and to make their operations more attractive to investors.

Utilizing innovative waste management strategies can be a surprisingly effective way to address these complex issues all at once. For example, cities with “zero waste” programs in place are working diligently toward their goals, too, however, major problems are encountered with curbside dumping and illegal dumpster deposits at apartments.

A Look Inside the Dumpster

Technology is taking a leading role with helping to solve this. CheckSammy is a national service with localized, regular pick-ups that more cities are turning to. Using monthly subscription-based pricing, CheckSammy can identify, sort, document, pick-up and repurpose part of the estimated $975 per North American household per year that holds on to reusable items or resorts to curbside and bin dumping due to no convenient means of donating. This includes items such as clothing, small electronics, linens, books, toys, sports equipment, kitchenware or any reusable household item.

This consumer bad habit is detrimental for apartment operators who face unit clean-outs from residents who move, or worse, are evicted, and leave bulk materials such as furniture behind. Retail stores and offices face similar dilemmas, having few options on how to dispose of materials in an environmentally friendly manner.

“CheckSammy helps by contributing the missing piece in the process,” company CEO and Co-Founder Sam Scoten says.

Working with cities in all 50 states, his company is one to identify the gaps in apartment companies’ progress to Zero Waste and design a program that meets their specific needs and goals.

CheckSammy uses its proprietary app that guides its fleet of drivers as they service the sustainability bins filled daily with their clients’ residents and retailers’ textiles, hard goods, E-waste and non-reusables. The app provides time-stamped data to capture sustainability and audit-ready data.

The app can also be used to capture data for third party waste and recycle haulers. Property management waste-hauling costs are rising, so property managers need to be more efficient. The best way to achieve that is through technology that automates tasks and frees time and money for property managers to focus on day-to-day operations and increasing revenue.

“For residential and commercial property operators, knowing what is in the dumpster on a daily basis really helps because it helps to create the waste meter,” says Mary Nitschke at RealPage, which in partnership with Compology launched an artificial intelligence, camera-based waste management solution in September. “With energy, for example you know from the meter how many kwh are being used, which makes reporting simpler. That kwh can be converted to BTUs so buildings that use gas for heating can be accurately benchmarked against apartment buildings that use electric heating.

“But with waste, operators can’t be certain what’s in the receptacle unless they know that the bin is half-full, three-quarters full, or 8 percent full at pick up? Does it contain all glass bottles, dirty diapers or a preponderance of non-collapsed cardboard, which gives the eye the sense that it’s full?”

Nitschke concurs that to determine that, imagery becomes the key. Using the proper camera is like having someone willingly watching and tracking each and every Dumpster on a daily basis so you identify and solve for that itemization and get to a true diversion. A time- and date-stamped photo becomes the proof of what is in the Dumpster,” she says.

Waste Monitoring in High Demand

Boston-based apartment operator GID has a waste management strategy in place to reduce waste to landfill. Its long-term reduction target includes increasing the portfolio diversion rate to 50 percent by 2027. Currently it is at 28 percent total diversion rate, or 56 percent of the way toward the target, according to its Head of ESG & Corporate Programs, Philip Carmody. Its current national portfolio includes 37,000 residential units and 5.5 million square feet of commercial space, spanning 18 states.

UDR, a leading multifamily REIT, uses its Environmental Management System (EMS) to govern its approach to evaluating the potential economic benefits of sustainable investments and monitors ongoing asset performance. Investment decisions are based on two primary factors, financial return and the expected impact to the environment.

These are appropriately weighted to align with its objectives of improving operating margin, lowering controllable expense growth, reducing our carbon footprint, and remaining cognizant of the expectations of our stakeholders and the markets we operate in, the company says.

Its EMS is designed to collect and categorize energy, water, and waste data in a timely manner. During the past 12 months, it has invested in and implemented numerous technological advances that have helped it to better analyze these data, including predictive analytics, mobile applications, utility smart meters, and interrelated computing sensors to more efficiently monitor equipment operations.

UDR consistently interacts with its waste partners to optimize weekly pick-ups, increase recycling and reduce carbon emissions to help the environment. In 2019, this work reduced trash waste by an estimated 337 metric tons and increased recycling by 4 metric tons in its same-store portfolio.

In addition, UDR utilizes trash monitoring services that reduce carbon emissions through automated, on-demand pick-ups, thus eliminating unnecessary services.

The company’s most recent data (2019) show that it increased the number of trash monitors at our properties by 24 percent.

Key Benchmarks For Waste Diversion

Today’s waste diversion programs require audits – and proper documentation is needed to help it all add up. The same can be said for property owners who are seeking certifications such as points-based LEED designations or other standards.

Likewise, the mission of GRESB, formerly the Global Real Estate Sustainability Benchmark, is to assess and benchmark the Environmental, Social and Governance (ESG) and other related performance of real assets, providing standardized and validated data to the capital markets. GRESB doesn’t like estimation and has challenged the multifamily industry to do better. Many investors are requiring GRESB participation for commercial and multifamily properties in the United States.

The USGB has now created a True Certification for Waste. It creates diversion by using formulas to identify material types, how full the bin is, and the frequency of pick-up to develop the diversion tonnages. The challenge of this standard is that the type of material must be known. Sonar sensors can register how full the dumpster, but cannot account for material type. Neither can scales account for what is making up that weight. The photo is the proof of content. The camera is the meter.

Throughout the year, CheckSammy Commercial compiles data on these buildings and presents a sustainability report showcasing the metrics and volumes re-directed from landfills. This avoids the errors that can come by relying solely on often inconsistent billing statements.

“CheckSammy helps by contributing the missing piece in the process,” company CEO and Co-Founder Sam Scoten says.

“Whether it’s a downtown high rise or a retail store in a mall, we offer businesses a way to track and report sustainability efforts for all its used consumer goods,” Scoten says.

EPA Sees the Need

Local ordinances about waste diversion are growing and are changing rapidly as greater emphasis on sustainability is viewed favorably by society, Scoten says. “It is very important to be able to report for recycling diversion because it is required and varies based on locality in markets such as Dallas and Austin, among others,” he adds.

The EPA has a tool for reporting waste diversion and some believe that this type of tool ultimately becomes more prevalent.

Craig Haglund, Program Manager, EPA’s Energy Star, speaks of the importance of tracking energy consumption and how his customers are driving a new, stronger focus on waste materials.

“Portfolio Manager® has long been used by commercial real estate firms as a tool to track, manage, and reduce energy consumption across their portfolios,” Haglund says. “Waste tracking has been added to the platform in recent years in response to the industry’s desire to cover broader sustainability management programs.

“We often say you can’t manage what you don’t measure, and this is especially true for waste since it can be challenging to get a handle on the quantity of waste and its various streams. Enabling better tracking of waste allows real estate owners and managers to reduce their impact on the environment, enhance their local communities, and improve their bottom line through more efficient management.”

Haglund adds, that investors “see organizational sustainability efforts not only as the right thing to do; but as an overall sign of good management.”

On the altruistic side, CheckSammy helps its commercial clients tackle the growing problem of used consumer goods generated by commercial properties by collecting and re-directing used and new office supplies – that might have been sent to a landfill — to new homes through their portfolio of non-profit and for-profit entities.

“We also encourage our clients to ask their tenants to bring in used clothing, shoes and accessories to help achieve and surpass their companies’ sustainability efforts,” Scoten says.

About the author:

Paul Bergeron has been reporting on the apartment industry since 2002 and served 20 years as Editor in Chief for National Apartment Association’s UNITS magazine. He currently is Editor of his LinkedIn media platform Thought Leadership Today and can be reached at [email protected].

Individuals who are investing in real estate through a 1031 exchange – or investing after-tax dollars – will need to consider investing either in property that has a mortgage or property that has no long-term financing (debt-free).

For clients in a 1031 exchange (per the current IRS code), a property with debt may need to replace the debt obligation in order to fulfill the 1031 equal or greater purchase price requirement.

We have found through the years that investors may not actually understand the various debt structures that they are investing in and that each loan may have different terms and agreements. There are pros and cons of debt.

Cash Flow

Often times, cash flow can potentially be higher when you use a debt within your investment strategy. High cash flow can be very attractive to investors, but high cash flow is only attractive until it is not… and this is where investors need to understand how a higher cash flow is being achieved and the risks associated with it.

We typically have seen sponsors use interest-only financing in order to get a higher potential cash flow, risking the large balloon mortgage payment that will be due. There would be no principle paydown in the loan and investors could potentially be stuck with a large loan balance that they will need to replace in their future 1031 exchange.

Cross-Collateralized Loan Obligations

Within the DST marketplace you will find that there are DSTs that have a single asset and there are DSTs that can contain upwards of 20+ properties.

It is important to understand the loan structure when considering investing in a DST with multiple properties that has a debt component. There are two types of debt structures that can be on a portfolio:

Each property within the portfolio has its own loan, or

All the properties are connected under one loan, otherwise known as a “cross-collateralized loan.”

A cross-collateralized loan is considered more risky, as it can potentially put a lot of restrictions on cash flow for investors and substantially limit the sponsor’s ability to sell the portfolio on behalf of investors. The DSTs might have multiple properties, providing diversification for investors, but if all the properties are under one loan this does not necessarily provide the diversification that most investors think they are getting.

For instance, there could be clauses within the loan that can significantly affect an investment, such as when a certain amount of properties stop paying rent or go bankrupt, the lender can call the loan or do a cash-flow sweep (meaning that because of one portion of the portfolio is having problems, the entire investment is at risk).

Credit-rating clauses allow a lender to sweep cash flow for a period of time should a certain tenant or a percentage of tenants’ credit ratings drop. For example, you could have a portfolio of net-lease corporate back properties that do not go out of business and do not stop paying rent, but maybe there is a recession or something else affecting the corporate level of your tenant that temporarily drops their credit rating. This gives the ability for the lender to lock all the current cash flow in the lender’s lock box, taking away an investor’s current cash flow.

We also have seen sponsors place a few properties within the portfolio that are not officially investment grade-tenants per Moody’s Standards and Poor’s ratings, and this is misleading to investors, as a non-investment-grade tenant can have a significant default risk.

Lastly, when you have a portfolio of properties under one loan it can potentially limit the ability to sell the portfolio, as in most cases you will need to sell all the properties at the same time. What if a buyer only wants to buy a portion of the properties because they do not like three of the 20 properties included? The sponsor may be forced to reduce the price to make it more attractive to that buyer.

Some sponsors have a strategy of a 721-exchange, which has its own sets of pros and cons.

If a portfolio is debt-free or not cross-collateralized, it can provide more potential exit strategies for the sponsor.

In short, investors that have the ability to stay debt-free can mitigate risks that a loan can bring on a property and its exit strategies. If investors need to take on debt or are comfortable with the risks of debt it is important to understand the pros and cons of the different debt structures available.

Kay Properties is a national Delaware Statutory Trust (DST) investment firm. The kpi1031.com platform provides access to the marketplace of DSTs from over 25 different sponsor companies, custom DSTs only available to Kay clients, independent advice on DST sponsor companies, full due diligence and vetting on each DST (typically 20-40 DSTs) and DST secondary market. Kay Properties team members collectively have over 115 years of real estate experience, are licensed in all 50 states, and have participated in over 15 Billion of DST 1031 investments.

Whether an auction is in-person or online, the goal is still the same: To acquire the piece of real estate at a fraction of the price. A common misconception is that it will take too long for your self-directed IRA (SDIRA) custodian to provide you with the proof of funds necessary to lock-in the winning bid. That is entirely untrue! There are three ways you can accomplish this part of the investment, but it is up to you to decide which method works best for you.

In the first method, communication is key. Typically, auctions are scheduled far enough in advance that you can make your SDIRA custodian aware of your intentions to participate on that specific date. The speed at which you will obtain your proof of funds will depend on the process of your SDIRA custodian. For example, at Preferred Trust Company we are able to process an investor’s direction to invest and provide a cashier’s check on behalf of the IRA within 24 hours (cashier’s check can either be picked up at our office or sent via overnight mail). If you do not win the bid, the cashier’s check must be returned to your custodian within 10 days of the auction.

Your second option is to establish an IRA-owned LLC with checkbook control, also known as a checkbook IRA. This means that you will have direct access to your qualified funds through the LLC’s bank account, essentially removing your custodian as the intermediary of processing your investments. It is important to note that even though you are not working directly with your self-directed IRA custodian, you are still responsible for reporting your investment activity to your custodian. For example, Preferred Trust requires that investors with checkbook IRAs submit monthly bank statements from the checking account, along with any documentation related to investment purchases transactions.

Although not encouraged, if you are in a time crunch, your third option would be to take a personal distribution from the IRA. Depending on your age (under 59½ or over 59½) and the type of account you are investing with (tax-deferred or tax-free), a distribution could be considered a taxable event. To avoid the taxable event, you need to provide proof of purchase to the custodian within 60 days of the initial distribution. The transaction will then be reclassified as an earnest money deposit at the close of the investment purchase. If you do not win the bid, the funds need to be returned to your custodian within 60 days of the initial distribution, or you may risk facing the IRS penalty and tax consequences, depending on your age and the IRA account type.

About the author:

Stephanie Fryar is the Content Creator for Preferred Trust Company. All content she produces is to help educate savvy investors and current clients about self-directed IRAs. Stephanie specializes in original content and market research related to alternative investments, but more specifically, real estate investments.

About Preferred Trust Company

Preferred Trust Company sets the standard for quick processing times, fewer transaction fees, personalized customer service, and the highest standard of compliance. Preferred Trust is currently waiving the establishment fee and first year administration fee for all new Self-Directed IRA accounts through December 31st, 2021. Click Here to learn more about this offer or call 888.990.7892 today!

An unfortunate reality of property management is the inevitability of dealing with slow-pay and no-pay tenants. Even though a tenant may pass your initial creditworthiness processes at application time, it’s impossible to predict if circumstances or intentions will change and the tenant will become a problem payor. When that happens, you have a couple of options.

Sure, letters, increasingly serious notices, personal visits, and stern phone calls are always the first steps to collecting, but what happens when those don’t work? Many property managers turn to collection agencies, but more and more are opting to report delinquent-payment histories to the big credit agencies using credit-reporting services like Datalinx.

Some property-management organizations assume that reporting tenants to credit bureaus isn’t an option for them; either they think their reports will be too small to be accepted, don’t think they qualify as creditors, or simply don’t know where to start. Companies like Datalinx acknowledged these issues, and since 2001 has been refining the process to make reporting to the big credit bureaus easy and affordable, which in turn makes this a very powerful and effective solution.

Do They Care About Credit?

For some consumers, credit scores are simply not an issue. Either they have no need to apply for credit, or they have simply decimated their credit score to what they think is a point of no return. Fortunately, those types of tenants probably wouldn’t have made it through your application process to begin with.

However, most people do care about their credit, and understand the impact a negative item will have on their future. Today, credit-card companies, banks, and free credit-monitoring apps provide credit scores to customers on a regular basis, indicating that more and more consumers are concerned about protecting their record.

Sometimes, simply notifying the customer that you now report missed or late payments to the four major credit bureaus will motivate them to pay on time. It certainly never hurts to remind them of your ability to report this information. Often tenants are under the false impression that rent payments are not reportable for credit-bureau purposes. However, services like Datalinx now offer property owners and managers the ability to report all payment histories, whether positive or negative. Informing your tenants that reporting tenants to credit bureaus is your practice and intention can make a big difference in the timeliness of payments, dues, and more.

Reporting tenants to credit bureaus and long-term effects

One of the questions consumers are most curious about when it comes to credit reporting is how long information—especially negative information—will remain on their reports. No one wants one missed payment or short-term collection account to negatively impact personal credit decisions for decades. Unfortunately, some tenants don’t give you any other option than to turn to alternative measures for recovering debt.

Generally speaking, negative information remains on a consumer’s credit report for about seven years according to Equifax, one of the major credit bureaus. Negative items can include late or missed payments, accounts that have been sent to collections agencies, situations when payments have not been paid as agreed, liens, or even bankruptcies. Seven years can be a very long time, especially when an individual applies for auto loans, new rental agreements, mortgages, or even certain jobs.

Each of these negative items not only will be listed as a red flag on a full credit report but will also drastically decrease an individual’s credit score. While some employers or organizations will listen to a consumer’s explanations or consider subsequent repayments of these debts, most simply cannot bend the rules to accept a score or report outside their established credit parameters.

As a property manager, adding this knowledge to your arsenal helps you not only educate past-due customers as to the long-term effects of their payment behaviors, but also helps you prepare new tenants with the consequences of late payments to your organization. In this case, knowledge is definitely power.

Why not consider a collection agency?

A professional collections firm is certainly an option to consider, but when considering cost and long-term impact, there are significant differences between collections and credit reporting. With a collections agency, the property owner or manager pays the agency a set fee or percentage of the amount collected from the tenant. The account is subsequently charged-off the books of the property owner or manager as a loss.

What does this mean for the consumer? First, the collection agency will report the account to the credit bureaus, and the debt will appear as a collection on the tenant’s credit report, instantly affecting their credit score. And, of course, this will be a negative item on the credit report for seven years from the date of the first missed payment. If the tenant makes payments to the collection agency and pays the balance in full (usually including a fee from the collection agency), the agency will report this information as well. Paying a collections account may have a lesser impact on a credit score, but the item will still be reflected on the report.

There is another important, but often overlooked, aspect of this process. When an account is reported to the bureaus as a collection, it can never be anything but that—a collection. Datalinx recommends another alternative: consider foregoing the collection agency and reporting the past-due account to the bureaus as delinquent, especially in cases where you believe the relationship with the tenant is repairable.

Why? A delinquent, or late, payment has a less negative impact on a tenant’s credit report than a collection, especially when the delinquent account is subsequently paid in full. Offering this option to a tenant also gives you as the property owner or manager leverage to urge the tenant to pay to avoid a much more detrimental impact on their credit. You lose that leverage when you turn over an account to a collections agency.

Credit is King…or Perhaps the Ace

With a credit reporting service like Datalinx in your rental or leasing toolbox, you hold the proverbial ace in the hole when it comes to persuading your tenants to pay on time. For those who care about their credit score, reports of consistent, on-time payments is an unexpected bonus to help them increase credit scores and build a solid, long-term history. This may be the impetus needed to nudge those on-the-fence individuals to pay closer to their due date instead of waiting until the last possible minute. And for the others, your Datalinx account allows you to report negative items while maintaining leverage to collect past-due funds—without paying fees to a collection agency.

Please visit our website at www.datalinxllc.com, or contact us at [email protected] or (425) 780-4530 if you have any questions or need our assistance.