Rent control laws are contributing to a shortage of affordable housing, according to economists.

When rent caps are imposed, developers build fewer new rental units, the supply of available housing declines and housing costs increase. Instead of rent control, policymakers should focus on supply-side solutions: reforming their local zoning code and providing tax incentives for developers to bring new units online, economists say.

Ryan Bourne, chair for the public understanding of economics at the Cato Institute’s Center for Economic Studies, said economists overwhelmingly agree that imposing rent control tends to reduce the amount and quality of affordable housing and explained why in an interview with FOX Business.

“Capping rents at a time when you know demand for property is growing strongly creates a situation where you have a shortage of rental accommodation relative to demand, so it creates shortages,” Bourne said. “And to the extent they create shortages, that can actually kind of raise the underlying market rents because if you kept rents below market rates, a lot of landlords will decide to convert their properties to condos or sell them for owner occupation.”

“So quite often,” he added, “it makes the kind of underlying market rate of property actually more expensive, rather than less expensive.”

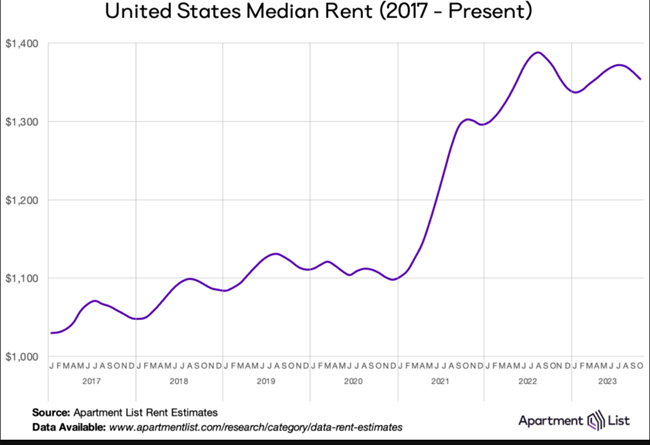

Despite warnings from economists, rent control is becoming more and more popular.

Oregon led the charge in 2019 when the state imposed a cap on older units, and California followed suit in 2020. Since then, municipalities in Illinois, Colorado, Massachusetts and elsewhere are considering similar moves.

The Housing Solutions Coalition provided this update on the status of rent control around the country.

RENT CONTROL UPDATES

MINNESOTA: Rent Control Continues to Chill Development in St. Paul: The ramifications of rent control are continuing to be felt in St. Paul as the planned construction of 2,000 market-rate units remains on hold. The developer stated that the pause results from an inability to find financing after St. Paul voters passed a rent control ballot measure in 2021. The project, which was planned years before the ballot measure, was slated to include a variety of housing options, including row homes, apartments, senior living and custom home lots. – MinnPost

ILLINOIS: State Lawmakers Push to Allow Rent Control in Illinois: State lawmakers kicked off a six-day legislative session over the next three weeks to consider bills recently vetoed by Governor J.B. Pritzker. Among the legislative proposals under consideration this session is HB 4104, a bill to allow local governments to enact rent control. If the bill passes, any Illinois municipality could hold a local referendum to exempt itself from the state’s existing preemption against rent control. – The State Journal Register

MAINE: Portland Voters Could Loosen the City’s Rent Control Ordinance: In Portland, Maine, voters will decide whether landlords will be allowed to set rents of their choosing between tenancies. As it stands, the city’s rent control ordinance does not allow for so-called “vacancy decontrol.” Thus, even between tenancies, landlords may not raise rents by more than a prescribed amount. But if the ballot initiative, Question A, is approved by Portland voters this November, then landlords would be allowed charge market rates to new tenants. – FOX 23

MARYLAND: Prince George’s County May Make Temporary Rent Control Permanent: This past February, Prince George’s County, Maryland, capped rent increases for one year at three percent. This policy was billed as a temporary, emergency measure. But now county officials are considering capping rent increases permanently. The uncertainty surrounding this policy has chilled housing investment in the county. Greg Reaves of Mosaic Development Partners warns that until these questions are resolved, many builders will look elsewhere to bring new units online. – Bisnow

MARYLAND: Rent Control Could be Coming Soon to Howard County: Howard County, Maryland, is struggling to keep housing costs low. To address the issue, the Howard County Executive, Calvin Ball, outlined a plan called the Housing Opportunity Meant for Everyone (HOME) plan. Regrettably, in addition to policy changes that would allow more housing construction, Ball’s plan includes a proposal to enact rent control. – The Baltimore Sun