Washington State legislation to boost housing construction and affordability along with prohibiting large investor entities from acquiring additional single-family homes.

By Aaron Kirk Douglas

Washington’s 2026 legislative session is in full swing with a strong focus on housing as lawmakers introduced a slate of bills to boost housing construction and affordability.

Notably, one proposal (SB 6026) would override local zoning to allow residential development in areas currently limited to commercial use – a big shift to open up more land for apartments or condos.

Other bills would pour new funding into affordable housing (including a $225 million Housing Trust Fund boost championed by Gov. Ferguson) and streamline development rules (for example, easing requirements for mixed-use projects and encouraging innovative building methods).

Private sector push for building housing

This pro-housing agenda has support from the private sector: top Amazon and Microsoft executives penned a Seattle Times op-ed urging lawmakers to cut red tape and “build our way out” of the housing crisis, backing ideas like SB 6026 and quicker permitting processes[.

In other news, Washington’s new law capping rent increases at 5% for manufactured home park tenants is facing pushback. A state landlords’ group filed a lawsuit this week calling the cap unconstitutional and claiming it deprives park owners of fair revenue with no emergency exceptions. The Attorney General is confident the law will be upheld, but the case will be an important test for rent control measures in the state.

Here are the details:

SB 5496 – Would prohibit large investor entities (those owning >25 single-family homes) from acquiring additional houses, with exceptions for nonprofits or if adding units (to curb bulk home purchases by institutional buyers).

SB 5647 – Expands the Real Estate Excise Tax exemption for self-help affordable housing programs (e.g. Habitat for Humanity-style projects) to all affordable homeownership facilitators.

SB 6026 – (Governor-requested) Bars cities/counties >30,000 people from excluding residential development in areas zoned for commercial or mixed-use; also forbids requiring ground-floor commercial space in mixed-use zones as a condition of housing development.

SB 6027 – Requires at least 60% of local housing & related services sales tax revenues be dedicated to constructing or acquiring affordable housing, behavioral health facilities, or related operations.

SB 6028 – Creates a state revolving loan fund (via Dept. of Commerce) to finance mixed-income affordable housing developments, with a portion of each project’s units permanently reserved for low-income households.

SB 6069 – Mandates that cities allow supportive, transitional, and emergency housing (and shelters) in any zoning district inside urban growth areas (except industrial zones), preventing local zoning from blocking these housing types.

About the author:

Aaron Kirk Douglas

Aaron Kirk Douglas is a multifaceted storyteller and market analyst. His career spans journalism, creative nonfiction, filmmaking, and real estate research. He serves as Director of Market Intelligence at HFO Investment Real Estate/GREA, the Pacific Northwest’s leading multifamily brokerage.

Coworking has replaced the traditional apartment business center as 75% say access to coworking spaces directly influences their decision to renew their lease.

By Becky McLaughlin

For years, the business center was treated as a baseline amenity in multifamily communities. It represented productivity, access and modern living. Today, many of those spaces sit unused, built around assumptions about work that no longer hold true.

Zillow’s 2024 analysis of 5.6 million U.S. rental listings highlights just how much expectations have changed. Apartments that continue to promote business centers receive 24% fewer saves and 27% fewer shares per day. Properties that highlight coworking spaces, on the other hand, see a markedly different response, with 16% more saves and 23% more shares.

That contrast reflects more than a naming preference. It points to a structural change in how residents integrate work into their daily lives and how shared spaces either align with that reality or fall behind it.

In a market where vacancy is elevated and rent growth is tightening, amenity decisions carry more weight than they did just a few years ago. Owners and operators are increasingly evaluating not just whether a space exists, but whether it actively contributes to renewals, occupancy, and long-term perceived value.

Why the business center lost relevance

Well before remote and hybrid work became mainstream, residents were already carrying their offices with them. Laptops, smartphones and tablets became everyday essentials, untethering work from a single room or piece of equipment.

As work became portable, fixed locations lost relevance. With 75% of employed adults now working remotely at least some of the time, and hybrid job postings up 60% over the past two years, demand for traditional workrooms has rapidly declined.

Work now happens wherever it makes sense. At a kitchen table. In a bedroom. Outdoors. For property owners, that reality changes the equation. A static business center no longer influences satisfaction or retention, because it was never designed to support this kind of flexibility. As a result, residents rarely factor it into leasing decisions.

Security concerns further limit usage. Shared printers and copiers, a core feature of business centers, have developed a reputation for storing and selling data. And when personally identifiable information has to flow through shared desktop computers, it’s not just an IT headache, it’s a liability, especially as data-privacy legislation continues to become more stringent.

Residents concerned about security will obviously avoid these spaces entirely, and in a competitive market where every square inch matters, that hesitation can be detrimental to a property’s appeal. As of October 2025, U.S. multifamily vacancy sits at 7.2%, the highest level in Apartment List’s index since 2017.

Rent growth is only projected to reach 2.6% by year’s end. In this environment, underperforming spaces do more than sit unused. They weaken perceived value and put pressure on revenue.

How residents approach work today

Residents no longer work in one place for eight hours straight. They move through a property depending on the task. Video calls happen in private soundproof pods. Deep focus shifts to quiet lounges. Short check-ins happen near a coffee bar.

The expectations are not excessive, but they are precise. Comfortable seating near natural light. Soundproof areas for important calls. Power outlets within easy reach. When those fundamentals are in place, people stay longer and return more often.

WithMe, Inc.’s recent resident survey found that 28% of residents use shared spaces for work either exclusively or alongside their apartment, while another 22% divide their time evenly between the two. More importantly, 75% say access to coworking spaces directly influences their decision to renew their lease.

Supporting a mobile workforce

If residents move throughout the property while working, the infrastructure must support that movement.

Wi-Fi coverage can’t stop at the leasing office. It needs to extend across coworking areas, common spaces and outdoor zones. When connectivity is inconsistent, residents will simply go elsewhere.

Daily use amenities matter more than ever. Technology-powered office essentials, like self-serve printing and on-demand premium coffee, can create consistent engagement without increasing operational strain. These features become part of daily routines because they solve real, recurring needs.

Variety in the space matters as well. Small collaboration spaces for two to four people consistently see stronger usage than oversized conference rooms. Individual focus areas need privacy, soundproofing and seating that supports full workdays. Conference rooms still serve a purpose, but they are no longer the focal point. Adaptability now carries more weight than scale.

When evaluating whether a coworking space is actually performing, owners should be asking a few simple questions. Does it support multiple work modes throughout the day? Is it easy for residents to move in and out without disruption? And does it rely on amenities people genuinely use, not just ones that photograph well?

In tight markets, properties that perform best are the ones designed around how residents work today, not how workspaces were imagined in 2010.

Moving beyond the business center

Business centers made sense when shared equipment was unavoidable and high-speed internet was not guaranteed. That era has passed.

Today’s residents value flexibility, mobility and spaces they actually use. Removing a business center is not about eliminating work support. It is about aligning amenities with modern lifestyles.

Every square foot must justify its presence. When it no longer does, it is time to rethink how that space is used. The most resilient properties treat shared space as an evolving asset, not a fixed line item.

About the author:

Becky McLaughlin is the senior vice president of revenue at WithMe, Inc. She has more than 20 years of experience and has led marketing teams in healthcare, technology, and insurance. Becky earned her Bachelor of Science from Syracuse University’s Newhouse School of Communications.

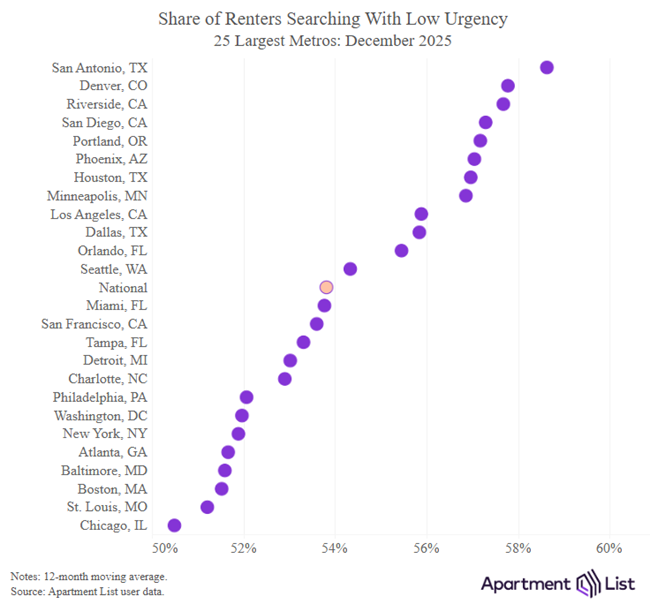

The share of renters who were “just looking” or “in no hurry” in find a place peaked in 2025, according to a new report from Apartment List.

Renters were taking their time because of high vacancy rates in some markets, plus soft conditions due to a surge of new multifamily units hitting the market.

“Given this backdrop, it’s perhaps unsurprising that renters are increasingly taking their time and considering their options,” writes Chris Salviati, chief economist for Apartment List, in the report.

The Apartment List Economics team looked at the aggregate level responses to the question: “How important is your move-in date?” Responses were collected on a 1-4 scale.

“I’m just looking” – Average 93 days from registration to planned move-in

“I want to move but am in no hurry” – Average 84 days from registration to planned move-in

“I need to move but can be flexible” – Average 59 days from registration to planned move-in

“I’ve got to move!” – Average 45 days from registration to planned move-in.

On average, low-urgency renters start their apartment search about three months before their projected move-in date. High-urgency renters, on the other hand, are planning to move in about 1.5 months. High-urgency renters tend to set higher budgets as well, knowing they have less flexibility when searching for their next home.

Renter urgency varies dependably with the seasonality of the market.

Changes late in 2025

However, the share of renters searching with low urgency fell in the last three months of 2025, dipping from 54.4 percent in September to 53.8 percent in December.

In early 2026 rents are still falling, and the national vacancy rate is still increasing.

“In other words, our core indicators are not yet showing any shift in the soft conditions that have characterized the rental market for the past few years. But the construction boom is now past its peak, and the number of new units hitting the market has slowed considerably.

“With fewer options and deals available from new properties in their lease-up phases, renters may be starting to feel just a bit more pressure; the recent increase in urgency could be a leading indicator for tightening conditions to come later this year,” Salviati writes in the report.

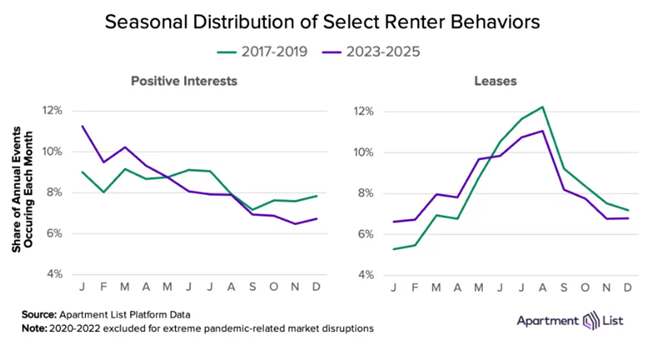

The rental market’s traditional seasonality is flattening and its timing is changing, according to a new report from Apartment List.

In the past, most people moved in the springs and summers, while the fall and winter months typically saw the opposite. Rents tended to follow the seasonal upticks and downturns depending on the activity in the market among those looking for new homes.

Highlights of the report:

The rental market has long been governed by a clear seasonal pattern: the greatest share of units turn over during the summer months, with peak rent growth occurring in tandem.

In recent years, we’ve begun to see a flattening of these sharp seasonal swings – peak rent growth is occurring earlier in the year and leases are less concentrated in the summer.

These shifts are due to a combination of factors including (1) the persistent impact of a one-time shock to the timing of moves due to the pandemic in 2020; (2) an intentional shift by multifamily operators to spread out lease renewal dates; and (3) a supply rich environment offering renters more optionality and flexibility in their moves.

School weather and holiday influence

This seasonality results from three practical factors: school, weather, and holidays. The summer is more favorable for all three:

If you are a student or have young children, you don’t need to juggle school schedules

Weather is generally more temperate

Moving expenses aren’t being eaten up by holiday spending

Renters who have the flexibility and means to relocate during the winter have generally found lower prices and more wiggle room for negotiating lease terms.

However, since 2022, rental activity is more evenly distributed throughout the calendar year, annual rent declines exceed annual rent increases, and peak rent growth has moved up earlier in the year.

Renters are starting and finishing their searches earlier

Equipped with remote work, better technology, and a favorable supply-demand balance, renters are becoming more patient and more willing to seek out an off-season move for a better deal. Apartment List researchers say, “We see this directly in the actions renters take on our platform, specifically interests and leases.”

An interest occurs when a user adds a property to their shortlist of potential new homes on the website. A lease refers to the move-in date for renters who do in fact sign that lease. The chart below shows average monthly rent change during two three-year periods: 2017-2019 (green) and 2023-2025 (purple) and the distribution of interests and leases throughout the calendar year, again split between the three years before and after the pandemic.

“Rather than being evenly distributed, we see interests concentrated in the first half of the year, and leases are concentrated during the summer. This is consistent with our baseline understanding of seasonality: the typical renter begins their search early in the calendar year (by expressing interests) and finishes it in mid-late summer (by signing a new lease).

“But starting in 2023, interests have become more front-loaded, with more than 30 percent taking place in the first quarter of the year. Meanwhile, the share of interests occurring in the second half of the year is well below where it used to be pre-pandemic. Leases, while still concentrated in the summer, have also shifted earlier. Compared to pre-2020, more move-ins today are happening between January and May.”

Local market dynamics can also affect this seasonality trend.

Are the shifts in rental seasonality here to stay?

Seasonality is changing due to a combination of factors, some temporary and some lasting.

Today’s supply-rich rental market, for example, will inevitably pass as the construction industry slows down. This will shift some negotiating power back from renters to landlords, and limit the steep winter price drops we’re currently seeing in builder-friendly markets such as Austin and Denver.

“But other factors have more permanence, like remote work, which gives renters more flexibility in choosing when and where to move. And perhaps more importantly, it appears some multifamily operators value a more evenly-distributed timing of lease renewals, and are actively pursuing it. It will be crucial to see in the coming years if these renter and operator behaviors continue to flatten seasonal swings, even as the market heats up,” writes Rob Warnock, senior research associate at Apartment List, where he examines trends in the housing and rental markets.

Open letter to City of Portland City Council and Mayor Keith Wilson

Re: City Council Doc. 2025-478 ($20.7M in unspent Rental Services Office funds).

Public hearing: Wed., Jan. 21, 6 p.m.

Dear Chair and Councilors,

I’m a Portland resident and an apartment owner. I support the Council’s direction to spend the roughly $20.7 million in unspent Rental Services Office funds on rent assistance, eviction prevention, and renter stabilization. Keeping people housed is humane—and cheaper than dealing with homelessness after the fact.

I also want to raise a transparency issue that matters to both renters and housing providers. Portland created the Residential Rental Registration Program to build a reliable inventory of rental units and provide regular updates. Owners report unit addresses annually. That should give Portland a clear count of rentals—and how the supply changes over time.

I don’t see Portland consistently delivering that promise to the public. The city can publish aggregated trend reporting without disclosing confidential details. We should be able to answer, year after year:

Are we gaining or losing rental units?

Are units leaving through condo conversions or sales into owner occupancy?

Are regulations and operating costs shrinking the rental inventory?

Are tenant protections working without reducing supply?

I support tenant services and stabilization. I’m not objecting to how you propose to spend these funds. I’m asking Council and the Mayor to recommit to the registry’s original purpose by publishing an annual “Rental Inventory Snapshot” showing registered long-term rental units, net change from the prior year, and changes by housing type and neighborhood.

Housing providers pay the fee, and those costs often show up in rents over time. Renters deserve both: meaningful help when they need it and clear reporting on whether Portland’s rental supply is stable, growing, or shrinking.

Respectfully,

Aaron Kirk Douglas

About the author:

Aaron Kirk Douglas

Aaron Kirk Douglas is a multifaceted storyteller and market analyst. His career spans journalism, creative nonfiction, filmmaking, and real estate research. He serves as Director of Market Intelligence at HFO Investment Real Estate/GREA, the Pacific Northwest’s leading multifamily brokerage.

The slippery slope of steering when customer service crosses the line in property management trying to be helpful or to “make things easier” for a prospect.

By Fair Housing Institute

In property management, strong customer service is often praised as the key to successful leasing and resident retention. Leasing professionals are encouraged to be personable, attentive, and helpful in guiding prospects through the decision-making process. However, it is in these well-meaning interactions that one of the most common and costly fair housing risks can emerge: steering.

Steering rarely begins as an intentional act of discrimination. More often, it develops gradually, rooted in a desire to be helpful or to “make things easier” for a prospect. Understanding how customer service instincts can quietly turn into compliance issues is critical for housing providers seeking to operate ethically and in compliance with the law.

How Everyday Conversations Lead to Steering

Steering often occurs in casual, conversational moments. A leasing professional may recommend a specific building, floor plan, or area of a community based on assumptions about a prospect’s lifestyle, family size, age, or perceived needs. While the intent may be to enhance the customer experience, these assumptions can unintentionally limit choices and create unequal access to housing opportunities.

The ethical issue is not the information being shared, but how it is framed and why it is offered. When suggestions are driven by who a prospect is rather than what is available, customer service shifts into decision-making on behalf of the prospect. This is where the slope becomes slippery. Even subtle nudges, repeated over time, can establish patterns that expose a property management company to fair housing complaints.

Focusing on the Property, Not the Person

Ethical leasing practices require a deliberate shift in focus. Customer service should center on providing complete, accurate, and consistent information about the property itself. Features, amenities, pricing, availability, and policies should be presented uniformly, allowing prospects to decide what best fits their needs.

This approach protects both prospects and leasing professionals. By avoiding personalized recommendations based on perceived characteristics, housing providers reduce the risk of steering while still delivering a professional and respectful leasing experience. Letting prospects lead the decision-making process is not a lack of service; it is a safeguard that reinforces fairness and compliance.

Customer Service with Clear Boundaries

Strong customer service does not require bending rules or tailoring decisions based on assumptions about a prospect or resident. It requires clarity, consistency, and professionalism, especially in leasing interactions where steering risks are highest.

Steering-focused training should include practical examples such as how to respond when a prospect asks, “Where do families usually live?” or “Which building is quieter?” without making assumptions or narrowing choices. Role-based scenarios that show how to present all available units, redirect subjective questions back to objective property features, and allow prospects to self-select are especially effective.

When staff are trained to recognize how everyday phrasing, tone, or informal recommendations can influence housing decisions, they are far better equipped to deliver strong customer service while maintaining clear ethical and compliance boundaries.

Protecting Trust and Compliance

Steering remains one of the most subtle yet serious risks in property management, precisely because it can emerge from well-intentioned customer service. Recognizing this slippery slope allows housing providers to remain helpful and engaging while ensuring that access to housing choices is never influenced by assumptions or personal characteristics.

Ethical property management is not about reducing service or sacrificing personability. It is about delivering equal customer service—where every prospect and resident receives the same information, the same range of options, and the same level of professionalism. That consistency is what supports fair housing compliance, builds long-term trust, and defines true excellence in the property management profession.

About the author and an offer for the New Year.

In 2005, The Fair Housing Institute was founded as a company with one goal: to provide educational and entertaining fair-housing compliance training at an affordable price at the click of a button.

Updated Fair Housing Training Resources for 2026

Thank you for your continued membership and support. To better support you and your company, we actively seek partnerships with reputable organizations in the housing industry. For the past year, we have partnered with The Fair Housing Institute (FHI), who have provided valuable fair housing insights through blog articles.

As a benefit of your continued membership, FHI is offering all our members an exclusive 20% discount on all their online, on-demand fair housing training courses for 2026.

FHI is one of the largest and most reputable fair housing training providers nationally. They have just released their updated 2026 course catalog, the industry’s largest collection of online courses. These courses, written by two fair housing attorneys, cover essential topics like criminal history screening, assistance animals, and reasonable accommodations. Many are available in both English and Spanish.

Even if you have an existing training provider for 2026 compliance, we wanted to make this valuable option available to you as a thank you for being part of our community.

Use the discount Coupon Code: RHJ26t o access your 20% savings. Click below to learn more about FHI and their course offerings:

U.S. advertised rents slipped again in December, producing the weakest quarter in years and wiping out gains made during the first half of 2025, Yardi Matrix says in its year-end report.

Multifamily rents pretty much ended the year where they started with the weak finish to 2025.

Regional disparities that defined recent years persisted through 2025. Rent growth remained concentrated in coastal markets and the Midwest, while the weakest performance was largely confined to the Sun Belt, where elevated new supply continues to weigh on pricing.

That is not stopping investors from increasing transaction volume and paying up for multifamily properties. Demand is strong, but counteracted by pricing uncertainty. High-growth secondary markets led by Dallas, Seattle and Phoenix attracted the most investor dollars in 2025.

Highlights of the report:

2025 ended on a down note for multifamily, as a weak finish to 2025 late-year performance wiped out all the gains from earlier in the year. The average U.S. advertised rent fell $5 to $1,737 in December, with year-over-year growth dropping 20 basis points to 0.0%.

Years without growth are rare. The last one with no average national advertised rent recorded was the 2020 pandemic year. Before that, the last one without a national rent increase was the recovery from the global financial crisis in 2010. We expect modest increases in 2026.

Single-family build-to-rent units are maintaining strong occupancy, but advertised rates are weakening as well. The average BTR advertised rent declined by $4 in December to $2,180, while the year-over-year growth rate fell to -1.0%.

“Fourth-quarter performance marked the weakest showing since the global financial crisis, raising concerns about near-term multifamily demand,” the report says.

“Looking ahead, despite ongoing economic uncertainty, stronger GDP growth in the fourth quarter points to improving momentum. Greater stability in 2026 could help lift consumer confidence and support a gradual rebound in rental demand.”

As Los Angeles braces for rising eviction pressure this winter and the potential loss of federal housing funds that could push thousands back into homelessness, county leaders are moving toward a decision that has major implications for housing stability in 2026.

In the first quarter of 2026, the L.A. County Board of Supervisors is expected to consider a pet-inclusive housing ordinance, following the 2025 release of a county feasibility study.

By evaluating ways to remove barriers for renters with pets, the study lays critical groundwork for a forthcoming 2026 ordinance to codify pet-inclusive housing policies, an effort championed by Supervisor Hilda Solis. The ordinance offers Los Angeles County an opportunity to lead with compassion and common sense, ensuring families can stay housed and remain intact while recognizing the needs of housing providers.

At a moment when more than 14,500 formerly homeless households are at risk of displacement, expanding housing access for renters who have pets is a critical part of the solution.

Pets are a major, overlooked factor of housing instability. Although most rentals claim to allow pets, restrictive breed and weight limits and excessive fees frequently force renters into impossible choices.

Los Angeles ranks among the worst major cities for pet-inclusive housing access, with just 64% of properties allowing pets, and only 5% without breed and weight restrictions.

Michelson Center for Public Policy is working with county leaders to ensure the ordinance reflects real-world housing providers’ concerns while providing pet-owning renters with options beyond losing their housing or surrendering their pets to LA’s already overcrowded shelters.

“Los Angeles County’s decision to explore pet-inclusive housing is an important step toward equity and housing stability. Supervisor Solis and County leaders are taking meaningful action by recognizing that pets are part of the family, and housing policies should reflect that reality. We are confident that with thoughtful collaboration, the County can develop a balanced approach that works for both renters and housing providers and creates a true win for everyone,” said Jennifer Naitaki, Policy Director, Michelson Center for Public Policy.

Why resident feedback is key for leasing, living and renewals with targeted, short-term pulse surveys and frequent check-ins.

By Carla Alicea

Grace Hill

Every transformation begins with a few voices. In the multifamily industry, that voice belongs to a community’s residents, and it’s important to listen at the right moments. Resident surveys have evolved dramatically, going beyond the “set it and forget it” mindset to a more dynamic ecosystem. The long-standing annual survey is no longer sufficient to support the resident experience.

Think of timing resident feedback like you would a conversation in a new relationship. It’s not healthy to wait an entire year to make sure everything is going well. For the relationship to thrive, it needs regular check-ins. This is the same approach that multifamily needs to take with its residents. Creating genuine connections drives satisfaction and retention.

Pulse and Moment-Based Surveys Are Must-Have Additions

Annual surveys remain essential for benchmarking and serve as the north star for understanding a community’s overall health. They’re valuable for comparative data and long-term trend analysis. However, these resident feedback surveys are like a photograph, and communities need a system that’s more like a live feed.

This is where shorter, targeted “pulse” and “moment-based” surveys are essential. These frequent check-ins capture feedback when experiences are fresh and emotions are authentic. They serve as strategic touchpoints that help communities stay ahead of emerging trends and issues, rather than discovering problems months after they’ve taken root. Pulse surveys are periodic “health” checks on resident sentiment. Moment-based surveys are triggered during specific events along the renter journey, such as move-in or renewal.

The move-in experience is a good example of the effectiveness of moment-based surveys. A resident’s first 30 days can shape their entire relationship with the community.

Waiting for an annual resident feedback survey to gather insights into their onboarding experience means missing the opportunity to set the tone for long-term success, celebrate wins or address issues. Some of the most important moments for surveys include move-in, maintenance, renewal and move-out.

Communities may also want to introduce pulse surveys between their annuals to check in on trend directions, as well as send out ad hoc surveys after making meaningful operational changes, such as the introduction of a new policy or proposed amenity.

The Shift from Reactive to Proactive

Almost all property managers have experienced the pain of discovering a maintenance issue through an angry, one-star review or learning about a policy issue via a non-renewal notice. Real-time feedback enables onsite teams to act quickly, improving resident satisfaction before it declines.

A proactive approach transforms teams from firefighters to architects of exceptional resident experiences. Catching resident feedback at critical moments—after a maintenance request, after amenity use, or during renewal discussions—gives teams the power to address concerns while they’re still manageable, or to gauge what’s working well.

The beauty of this moment-based feedback lies in its specificity and timeliness. Instead of asking a resident to recall a maintenance experience from six months prior, teams can capture their thoughts within days. In addition, human memory is notoriously unreliable, especially over time. The proactive immediacy of pulse surveys gives more accurate data and more actionable insights.

Turning Data Into Direction

When survey insights are unified across touchpoints, like maintenance response times or renewal likelihood, property managers gain a 360° view of resident experience and can connect feedback directly to measurable outcomes.

This connectivity in data streams reveals powerful correlations that drive strategic, data-based decision-making.

For example, at move-in, “Value for Amount Paid” is one of the strongest levers behind overall satisfaction. When heading into renewal, “Management’s ability to resolve problems” becomes the make-or-break driver.

From there, trend reporting adds context over time, helping teams spot shifts early and make proactive adjustments before minor issues grow into major problems. Frequent analysis can also bring to the surface patterns that might otherwise go unnoticed, like seasonal fluctuations in satisfaction or how new policies influence resident sentiment.

Advanced analytics, including AI-powered analysis of open-ended responses, can uncover themes that traditional metrics might miss. If residents mention communication, AI can assess whether they are praising a team’s responsiveness or expressing frustration with it.

Building Long-Term Trust

Regular communication through resident feedback surveys not only solves today’s problems but also shows residents that their voices shape the community’s future. The ongoing dialog builds something that’s invaluable—trust.

This develops when residents see their feedback translated into action. Trust grows when teams communicate changes transparently, acknowledging both successes and areas for improvement. It flourishes when residents feel heard, valued, and respected as partners in creating a thriving, exceptional community.

Owners and operators may want to implement a “You Asked, We Listened” communication strategy across their portfolios, and onsite teams should regularly share how resident feedback influenced improvements. This transparency demonstrates a commitment to continuous enhancement and encourages ongoing feedback in a survey ecosystem.

Other Critical Factors of Pulse Surveys

The above covers the benefits of implementing a system of pulse or moment-based survey, but there are other factors that need consideration for a successful system of resdient feedback:

Response Rates – Reliable data typically comes from response rates of 10%-20% for resident surveys and 7%-10% for prospect surveys. Shorter surveys don’t automatically yield better response rates. This is less about survey design and more about creating a culture where feedback is encouraged and truly matters. Communities can improve their response through effective promotion and consistent communication.

Psychological Safety – Residents need to feel confident that their honest feedback won’t result in any negative consequences. This means that onsite teams need training in responding to criticism with gratitude rather than taking a defensive stance. They should always demonstrate that residents’ input drives action and positive change.

Sentiment Influences Metrics – Always remember that the correlation between resident sentiment and operational metrics is undeniable. Timely and personable communication significantly impacts renewal, referrals and reputation. Open lines of communication and responsiveness to feedback foster a sense of belonging among residents.

Multifamily can continue with traditional approaches that provide limited insights, or it can embrace a system that transforms how communities understand and serve residents.

Owners and operators can improve leasing, the resident experience, and renewals by listening with greater intention, responding more quickly and acting more decisively based on data. Residents are ready to share their experiences—is multifamily ready to listen?

About the author:

Carla J. Alicea is a customer-focused research and analytics professional with nearly 30 years of multifamily industry experience, specializing in resident and employee insights. Her work focuses on how perceptions and behaviors across both audiences shape trust, satisfaction, and performance. She is senior product manager, research and analytics, at Grace Hill. Grace Hill provides technology-enabled performance solutions that help owners and operators of realestate properties increase property performance, reduce operating risk and grow top talent.

Management company awards rent-free holiday to residents fighting health issues, financial hardship and loss of loved ones.

By Paul Bergeron

BH Management company has awarded 220 residents and households a rent-free holiday for this past December as a way of giving back to residents.

Launched in 2023, BH’s rent-free holidays program helps bring relief to residents who need it most by covering their December rent and expenses. In the first year, BH Management helped eight deserving residents, and in 2024, that number rose to 138.

Among the residents who won awards this year were those fighting health issues, financial hardships, emotional struggles, and the loss of loved ones.

For each resident selected for a rent-free holiday, BH teams presented winning residents with oversized checks, balloons, confetti, and flowers.

A BH community manager in Texas nominated long-term residents facing challenges, noting their resilience and commitment to the community despite their hardships. “This program serves as a gesture that their community stands behind them during tough times,” said the community manager.

This effort has affected the lives of many deserving residents during a time of year that can sometimes feel burdensome and overwhelming.

“Making happy moments and giving back to our communities is at the core of what we do at BH, and rent-free holidays has become one of our favorite ways to do that over the past three years,” BH CEO Joanna Zabriskie said. “We’re grateful to have caring employees and client partners who stepped up to make this our best year yet.”

Katie Vanderveen, Vice President of Asset Management at Pensam, shared her thoughts on the program, saying, “This initiative is such a powerful example of the impact Pensam and BH are making in the lives of residents. It’s not just about covering rent; it’s about giving families peace of mind, hope, and a chance to truly enjoy the holiday season.”

Zabriskie, added, “Giving back and making happy moments for our residents are part of the fabric of BH’s culture, and we are truly grateful for Pensam’s partnership in bringing the ‘Rent-Free Holidays’ program to life for the second year in a row.”

About Pensam:

Pensam is one of the country’s largest private real estate investors and capital providers specializing in the vibrant U.S. multihousing sector.

About the author:

Paul Bergeron is a freelance writer who covers rental housing issues.