Financing the niche with re preferred equity and multifamily financial pivot, stabilization and new acquisitions in commercial real estate

By Gary Williams

Rothchild Capital Solutions of Illinois

“The Age of Disruption” and the title alone suggests the insurmountable obstacles within the commercial real estate development and new acquisition. This article will serve two purposes. One, it will highlight how the distinguishing factors impact the way that developers, sponsors, and lenders approach the negotiation table to discuss key elements of commercial real estate projects along with financing and will discuss obstacles facing developers and sponsors in need of equity and or investment capital and the lack of capital available during covid-19.

“A MEASUREMENT OF RISK AND FINANCING”

It’s true the possibilities are great as real estate owner and or investor however before you take the plunge ahead, you should realize and understand that project leveraged to high followed by sponsor low balance sheet is recipe for disaster.

Now depending on your level of optimism and the appetite you bring to the of hotel development and or acquisition table this transaction will either represent an opportunity to obtain a higher rate of return on your investment, or this may signal you to lower your risk tolerance. As a young man in the very early days of my career “A Wise Man” once told me that Risk comes from three places in the life of any business transaction (a). not knowing and or understanding what you are doing, (b) failing to plan for the unseen, (c) without strategies to mitigate and or exit.

RCS looks at three of the main factors that differentiate a hotel business operation from other commercial real estate business operations and or investments. (a) absence the benefit of long-term cash flow (tenant lease), (b) projects that are leveraged to high with the wrong type of financing and (c) short terms tenants known as Hotel Guest only pay market daily rates that are influenced by several factors out of your control.

RCS PREFERRED EQUITY EUCLID ALGORITHMS

Our first approach to the RE EQUITY fund was to lower the term cost of financing which we accomplished developing a term that allowed stabilization to mature. Secondly, we developed CMT rate structure that lower the cost of financing over the term significantly which is a key element using a preferred equity approach.

MEZZANINE VS. RE PREFERRED EQUITY

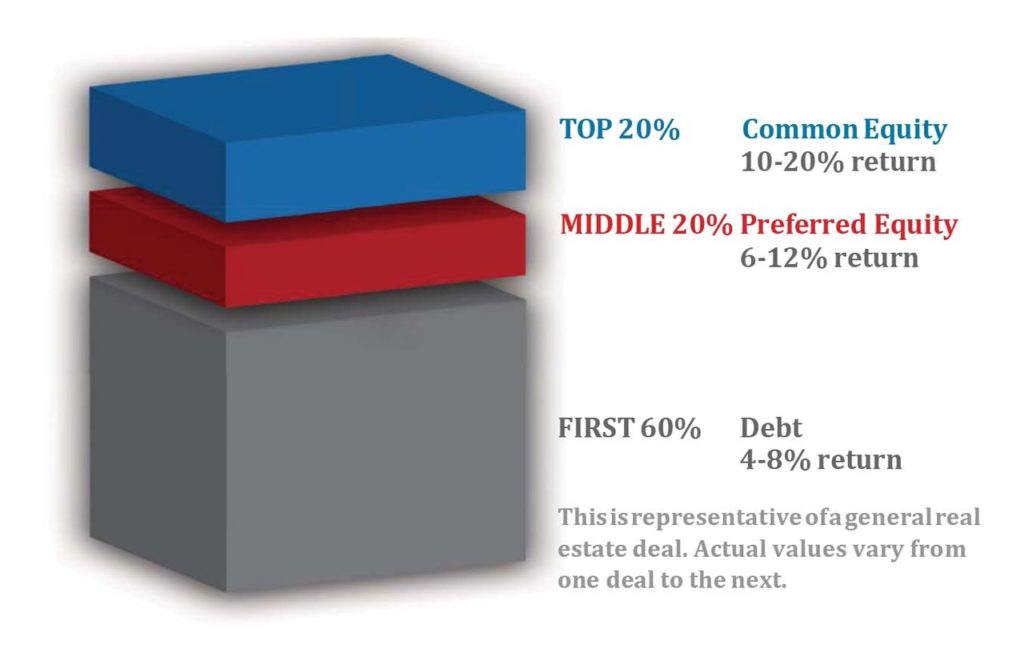

Mezzanine loans and preferred equity investments are used to achieve very high leverage on large commercial projects. Normally conduits, banks, and life companies will not exceed 80% loan-to-value when making commercial mortgage loans. Mezzanine loans and preferred equity investments are stacked on top of big construction loans or big permanent loans to achieve loan-to-cost ratios as high as 95% in most cases. A preferred equity investment is quite different from a mezzanine loan, but it accomplishes almost the exact same thing. The lender makes an investment of equity with a preferred return in the LLC that owns the big commercial project. If the management of the LLC fails to pay the preferred member the promised return, the old management is ousted and the common members of the LLC (the former owners) lose their voting rights, dividends, and right to the distribution of any profit.

THE NORM RE PREFERRED EQUITY

Preferred equity investment in real estate come in various forms and, unlike subordinate or mezzanine loans they are typically documented in the borrower’s organizational (entity) documents. Generally, the deals are structured as an investment from a third party in the real estate owner’s legal entity and or affiliates entities. The exchange on the norm is interest in the real estate direct cash flow and or indirect under a preferred priority return. Such have provision where (i) interest on the investment money paid monthly regardless, (ii) total investment amount paid upon maturity date, (iii) default rate with interest and other penalties assessed against the borrower followed by loss of management and or ownership. This is considered a very HARD approach and structure.

THE NEW WOLF OF WALL STREET REAL ESTATE “ROTHSCHILD RE PREFERRED EQUITY INVESTMENT MODEL

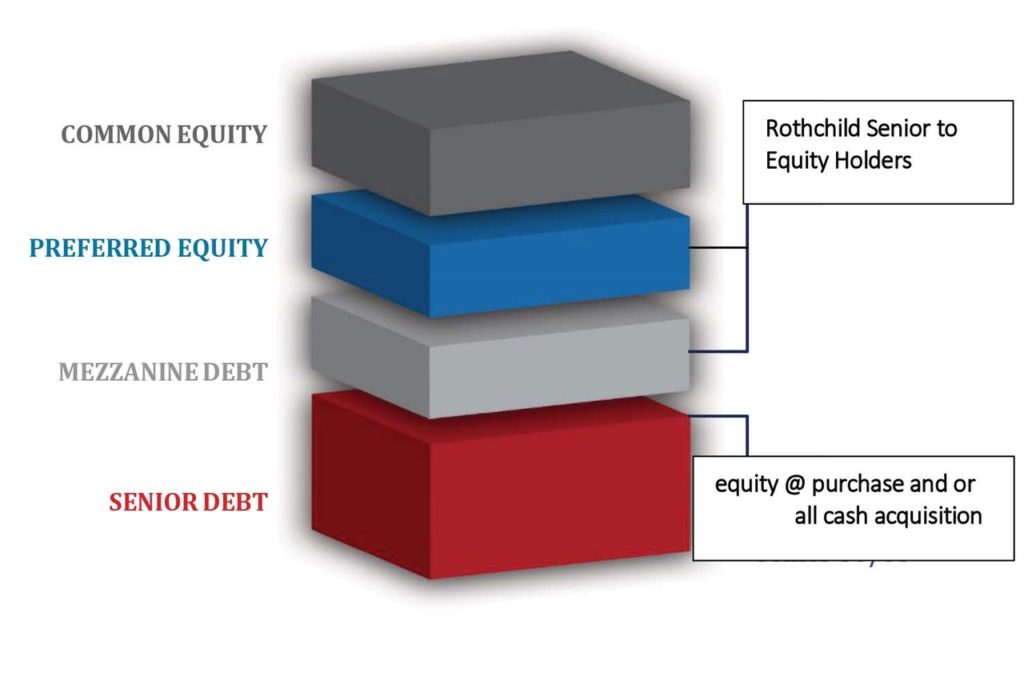

Preferred equity Rothchild Capital a real equity investment into the real property borrowing entity, junior to the development debt lender but senior to the borrowers’ equity, secured and packaged under a new formula into a single asset instrument EJV with far less provisions eliminating all threats of violating the senior lenders loan agreement. Where the legalese will have some standards of DEFAULT NON-COMPLIANCE and CARVEOUTS over all this new and innovative approach is unlike the more traditional model image above use in most real estate preferred equity transactions today. Accordingly, these investment transactions raise many issues and have many concerns and pitfalls for both the senior lender and equity provider which includes transfer of management and controlling interests. The legal term at LaSalle has developed a workable solution in the event of such. Controlling interest can be shared and or third party out and management can be yield by agreement. The transfer of controlling interest will always remain a concern and never go away, in addition there is no “one-size-fits-all” solution. A wise man once told me “Only the Hands of the Diligence will be made rich”. Preferred equity investment is here to stay and will play an important role in filling the gap left by traditional financing. Our current financial and lending environment with the introduction of BASEL III and recent adjustments to HVCRE will required financial practitioners to be much more solution oriented with a high-level efficiency than ever before.

THE RE PREFERRED EQUITY INVESTMENT: THE RCS MODEL

Rothchild Capital Solutions managing partner Shelton has developed a new financial formula for RE Preferred Equity transactions achieving much higher leverage ratios on the capital stack then the traditional model shown above. RE Preferred Equity Group at RCS (the PEI model) Shelton has coined a unique blended structure with elements of Private Equity, Mezz Debt, and Investment Finance.

Rothchild Capital Solutions

Private Niche Lender

Rothchild Capital Solutions of Illinois-708-540-1711

Gary Williams Partner Midwest & Southeast | [email protected]

{kind=link}