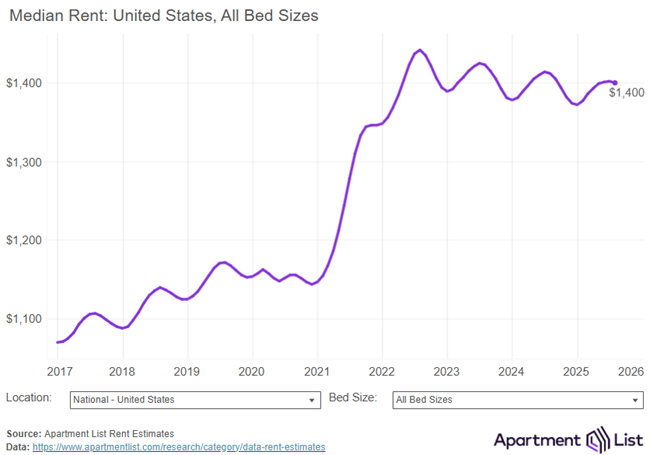

Rents dipped 0.2% in August, the first month-over-month rent decline nationally, according to the September report from Apartment List.

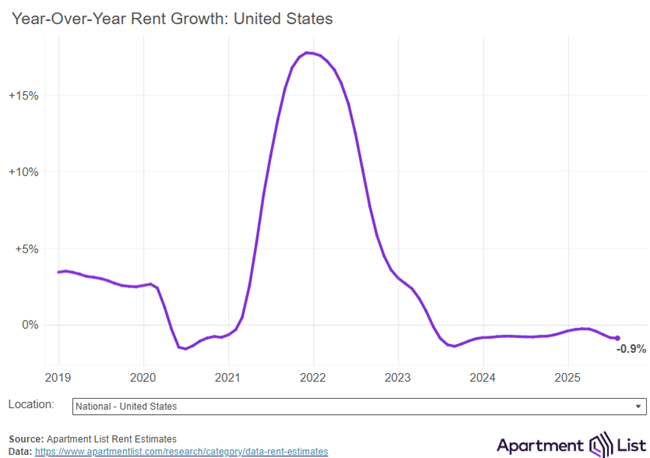

Rents are now down 0.9% year-over-year.

This marks the end of the busy season for moving activity, and it’s likely that rent prices nationally will continue to decline through the fall and winter, when fewer renters are typically looking for apartments, according to the report’s research team.

“Monthly rent growth peaked at +0.6 percent in March this year, and then began to gradually trend down during the peak moving months, when rent growth is normally fastest.

“The flip to negative month-over-month growth has also come a bit earlier than what we saw in pre-pandemic years, although this is now the third straight year that prices have begun to dip in August,” the report says.

Highlights of the rent report:

- After the August decline, national median rent stands at $1,400.

- Year-over-year rent growth has ticked further negative for four consecutive months and is now at its lowest level since December 2023.

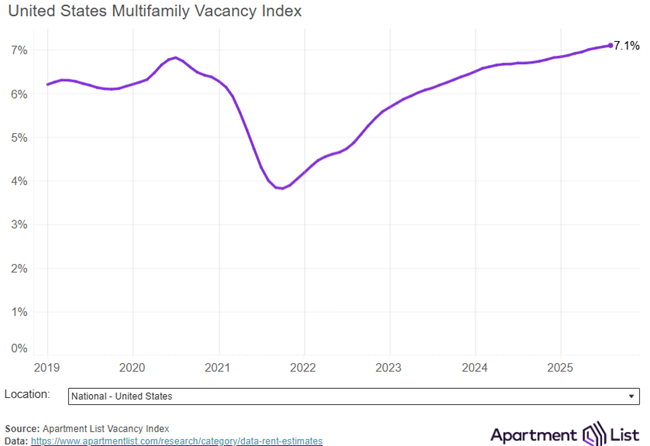

- The national multifamily vacancy rate sits at 7.1%, a record high. We’re past the peak of a multifamily construction surge, but a healthy supply of new units is still hitting the market, and vacancies are still trending up.

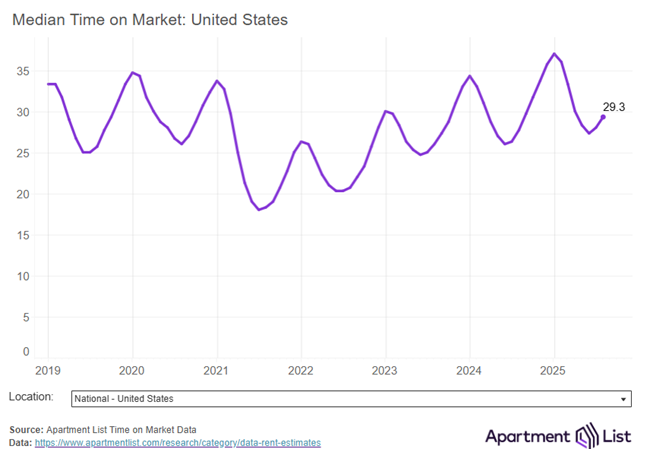

- Units are taking an average of 29 days to get leased after being listed, up one day from last month’s reading, and down from a high of 37 days in January.

Multifamily vacancy rate hits 7.1%, a new peak

The most important driver behind the soft rent growth of recent years has been a historic surge of multifamily construction.

However, while the peak of the multifamily construction surge has now passed, a healthy supply of new units is still hitting the market, and vacancies are still trending up.

Conditions are expected to tighten later this year and into next as the supply wave continues to recede, but for now the market is still absorbing a swell of new units.

New supply driving falling rents in Sun Belt markets; the Bay Area heats up

The Austin metro currently has the softest conditions among the nation’s large rental markets, with the median rent there down by 6.6% over the past year.

At the other end of the spectrum, the San Francisco metro has seen the fastest year-over-year rent growth (+4.7%).

List-to-Lease time ticks up for first time this year

As more vacant units have come onto the market, those units have also been sitting vacant for somewhat longer.

The typical “list-to-lease” time peaked at 37 days nationally in January, an all-time high going back to the start of the data series in 2019.

“We have since come down from that peak, but August saw time on market tick up for the second consecutive month, increasing from 28 days in June to 29 days this month,” the report says.

August Rents Conclusion

As the report saw national rents dip again, all key indicators are pointing toward ongoing sluggishness in the multifamily rental market, as rent growth is slipping and the vacancy rate is at an all-time high.

A return to tighter market conditions remains on the horizon, but the outlook has been complicated by a continued influx of new units to the market and macroeconomic whiplash being caused by tariffs and other policies being pursued by the Trump administration.

“With construction expected to slow further in the second half of this year and into 2026, conditions are likely to shift, but it will still take time for the market to metabolize the recent growth in the rental stock,” the Apartment List research team writes.

Read the full report here.

{kind=link}