Cost and geography are defining America’s renters as young renters, family renters, and long-term renters who face different challenges of being priced out or locked in – its the affordability gap.

The United States rental market is often discussed as if it were a single, uniform experience. It is not. A new report, which includes an analysis of 2024 American Community Survey data across the 100 largest metropolitan areas by Realtor.com, finds the U.S. rental market is splitting into three distinct but overlapping groups. For most tenants, the decision of where and how to live is increasingly a calculation of financial survival rather than a lifestyle choice:

- Young renters are being priced out of the markets they once defined

- Family renters — which are disproportionately minority households — find homeownership structurally out of reach

- Long-term renters remain largely locked in place, many unable to afford the market they already live in.

Together, these trends reveal a rental landscape shaped less by individual preference than by cost, geography, and unequal access.

“We often hear that today’s renters are choosing to rent because they don’t want to be homeowners or are choosing to be ‘forever renters,’ but in order to understand what’s holding renters back, we need to know who they are, where they are, and why they’re renting,” said Danielle Hale, chief economist at Realtor.com.

“America’s rental landscape is being shaped by cost and geography in ways that limit flexibility for almost every type of tenant, whether it’s young professionals moving inland for breathing room or families in high-cost markets stuck behind an affordability wall. Despite the fact that 75% of Americans believe homeownership is part of the American dream, we found that in nearly every category of renter, achieving homeownership is a challenge.”

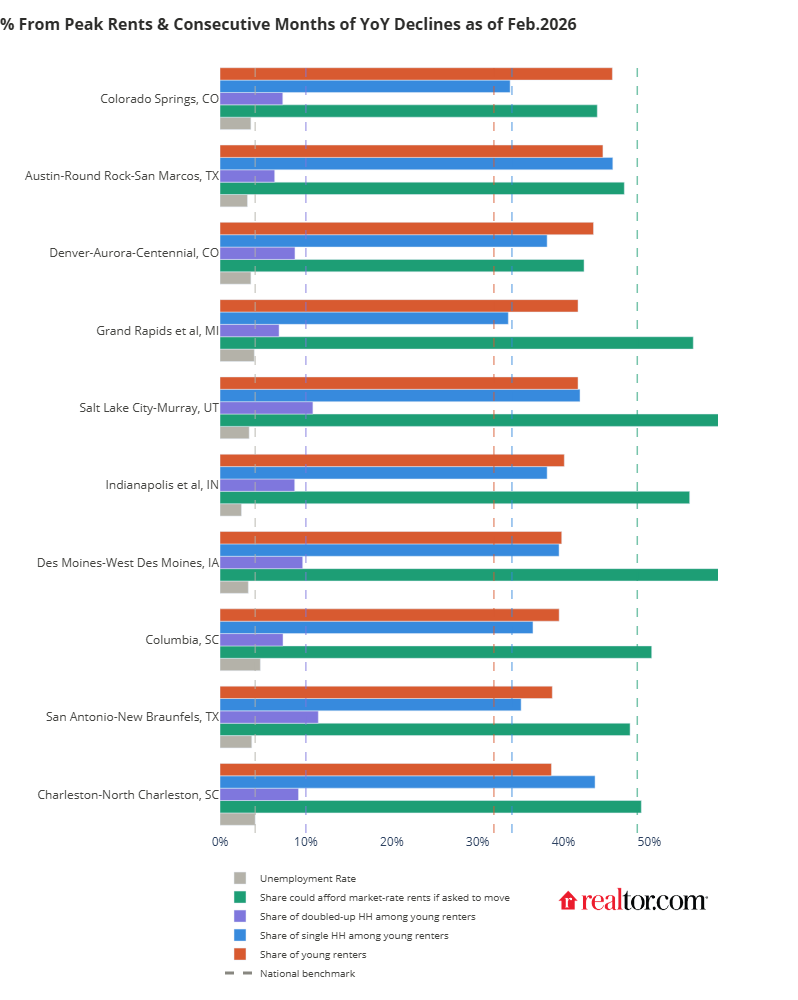

The New Geography of Young Renters

- Young renters represent 31.9% of all renter households nationally.

- A typical young-renter household in the U.S. is headed by a 28-year-old adult, with a household size of two people living in a two-bedroom unit, earning $65,000 annually.

- Young renters are concentrated in mid-size, affordable inland metros that offer job opportunity— not expensive coastal cities.

- Markets with high young-renter shares show significantly lower affordability stress, higher shares of single-person households, and lower rates of doubling-up.

The top metros for young renters include Colorado Springs (45.7%), Austin (44.6%), and Denver (43.5%). The shift is driven by a massive affordability gap: In the top 10 young-renter markets, an average of 52.6% of renters can afford a fair market rent, compared to just 32.0% in Miami and 33.6% in Los Angeles. Yet, affordability alone does not explain why young renters choose these specific markets over other affordable alternatives.

The top markets also offer something equally important — jobs. In December 2025, the average unemployment rate across the top 10 young renter markets was 3.6%, compared to a national rate of 4.1%, suggesting these are not just cheap markets but genuinely tight labor markets where early-career opportunities are abundant. Austin — named twice as a top destination for recent college graduates — has emerged as one of the country’s most dynamic labor markets, drawing technology companies, financial services firms, and corporate relocations that have created a deep well of early-career opportunity.

Where renting is affordable, these households have the financial room to live independently, with higher shares of single-person households. Where it is not, they are forced to double up. In Los Angeles, for example, 16.3% of young-rental households live in “doubled-up” arrangements, nearly twice the 8.6% average in the top 10 young-renter markets.

The Homeownership Barrier for Family Renters

- Represent 44.3% of all renter households nationally

- A typical family-renter household in the U.S. is headed by a 42-year-old adult, with a family size of three people living in a three-bedroom unit, earning $68,000 annually.

- Family renters are concentrated in majority-minority markets across California, Texas, Florida, and Hawaii.

- These renters face a double barrier: high home prices that put buying out of reach, compounded by a long-documented homeownership gap that disproportionately affects minority households.

- Markets where family renters concentrate most heavily are among the most burdened and most crowded in the country.

Family renters represent the largest share of the market at 44.3% nationally. The geography of family renting is, to a significant degree, the geography of minority America. The highest concentrations are found in majority-minority markets across California, Texas, Florida, and Hawaii, led by Stockton (63.3%), Riverside (61.7%), and McAllen (61.0%).

This concentration reflects two forces working in the same direction. First, minority groups tend to have higher family-formation rates. For example, among all Hispanic households, 67.9% are family households, compared to 60.1% among white-alone households. Second, and more fundamentally, minority families in these markets face a double barrier to homeownership.

Home prices have climbed far beyond the reach of median-income households — every one of these markets scores below the national affordability benchmark, according to Realtor.com data. This affordability wall is compounded by structural barriers that persist regardless of market conditions — unequal access to credit and limited intergenerational wealth have produced a homeownership gap that remains wide and well-documented.

The Lock-In Effect for Long-Term Renters

- Long-term renters represent 36.1% of all renter households nationally.

- They are concentrated in rent-regulated anchor cities (New York, Los Angeles) and their spillover markets across California and the Northeast.

- A majority of long-term renters cannot afford current market rents. An average of just 39.2% of renting households in the top 10 metros would face severe affordability stress if forced to move at fair market rent within the same metro, assuming the same household incomes and bedroom sizes.

- A typical long-term renting household is headed by a 55-year-old adult, living in a household of two people and two bedrooms with a median household income of $48,500.

Long-term renters, those in the same unit for five or more years, are increasingly concentrated in the country’s most expensive anchor cities. In New York (53.3%) and Los Angeles (49.6%), decades of rent stabilization have kept millions of tenants in below-market units they cannot afford to leave.

This “lock-in” effect extends to overflow markets as well. Renters priced out of Boston have moved to Providence (44.4%) and Worcester (44.0%), but may find themselves stuck again as rents rise in these secondary cities. On average, 39.2% of renter households in the top 10 long-term renter metros would face severe affordability challenges if they were forced to move within their current metro at fair market rent. The burden is most acute in Providence (45.8%) and Bridgeport (43.9%), where renters have simply run out of affordable places to go.

Not all long-term renters are the same. Some stay by choice — drawn by community ties, neighborhood familiarity, or simply a preference for stability, especially for senior renters. But for many others, staying put is not a preference.

“When you look beneath the national averages, you see a market that is failing to provide mobility,” said Jiayi Xu, economist at Realtor.com. “The lack of new, affordable inventory means that for many, the ‘American dream’ of choosing where you live has been replaced by the necessity of staying exactly where you are.”

Read the full report here.

Methodology

This analysis draws on 2024 American Community Survey (ACS) one-year estimates across the 100 largest metropolitan areas. The sample is restricted to renter households headed by an adult over 18 who is not currently enrolled in school, focusing on households actively participating in the housing market.

Photo credit Mary Long via istockimages.

FTC Seeks Comment On Potentially Unfair Rental Housing-Fees

The Federal Trade Commission has announced it is seeking written public comment on a notice of proposed rulemaking to address nationwide potentially unfair rental housing fees or deceptive fee practices in connection with rental housing.

As detailed in a Federal Register notice announcing an Advance Notice of Proposed Rulemaking, the FTC is seeking written comments, including data, evidence, analyses and arguments, regarding rental housing fees and charges throughout a lease lifecycle, from application to moveout.

“Rental-pricing practices that are neither clear nor transparent undermine competition and harm consumers,” said Christopher Mufarrige, director of the FTC’s Bureau of Consumer Protection. “The Trump-Vance FTC is focused on addressing unlawful business conduct that obscures the actual cost of housing and undermines price competition.”

The failure to advertise the true total rent can limit consumers’ ability to make informed financial decisions, increasing their search costs and exposing them to other negative monetary consequences when they take on more rent than they can afford. These practices also may undermine competition by weakening the incentives of rental-housing providers who do advertise the true total rent.

The notice seeks comments on such topics as:

Unfair and deceptive rental housing fee practices violate federal law. In the past two years, the FTC has filed two cases challenging these fee practices by nationwide housing providers. Invitation Homes, the largest single-family home rental housing provider in the country, agreed to pay $48 million to settle FTC allegations that the company violated the FTC Act by, among other things, excluding mandatory monthly fees from the advertised rent.

Greystar Real Estate Partners, the largest residential rental property owner and manager in the nation, was ordered to change its fee disclosure practices and pay $23 million in consumer redress to settle a lawsuit by the FTC and the state of Colorado that alleged the company misrepresented the true cost of renting a property and excluded mandatory fees from the advertised rent.

Case-by-case enforcement, while essential, addresses only some aspects of the harmful fee practices in the rental housing industry. The notice announced this week explores whether a rule is needed to address hidden and misleading fees that inflate rent well beyond what is advertised and other problematic fee practices imposed throughout a lease lifecycle. It also would serve as a deterrent against those practices because it would allow the agency to seek civil penalties against violators and more easily obtain redress for harmed consumers.

Consumers can submit comments electronically for 30 days, ending April 11. Consumers also may submit comments in writing by following the instructions in the “Supplementary Information” section of the Federal Register notice.