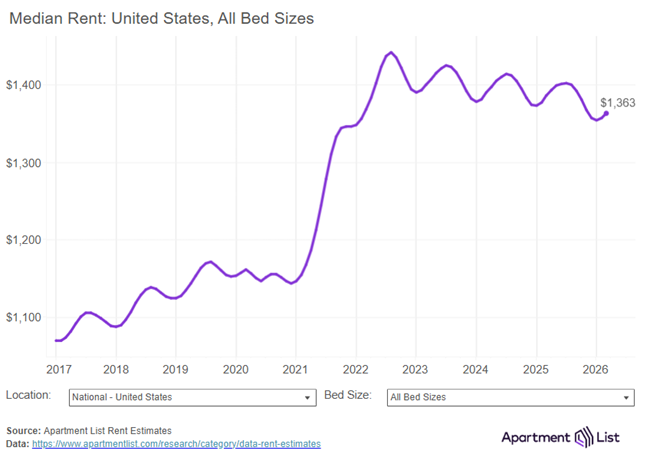

The national median rent ticked up by 0.5 percent in March, increasing for the second consecutive month following six straight monthly rent declines, according to the April report from Apartment List.

“This turn represents the market creeping out of the off-season, and we’ll likely see continued increases in the months ahead as moving activity ramps up, in line with typical seasonal patterns. Prices generally soften as fewer renters move during the fall and winter, and then gradually begin to increase as we get closer to the peak moving summer season. February marked the return to positive rent growth, and March is continuing that trend,” the Apartment List research team writes in the report.

Highlights of the April report:

- The national median rent increased by 0.5% in March, and now stands at $1,363.

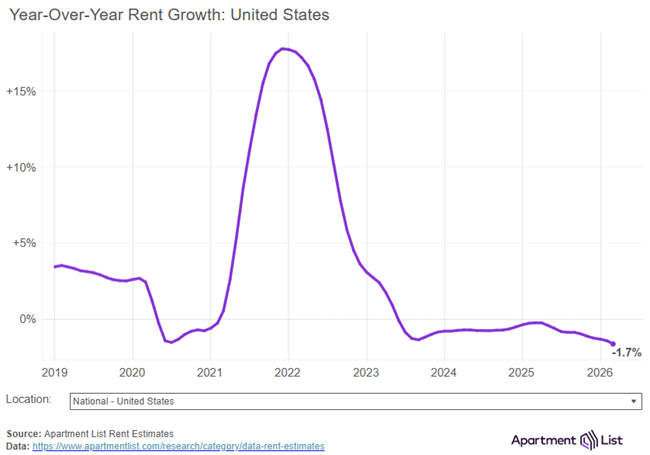

- Rent prices nationally are down 1.7% compared to one year ago. Year-over-year rent growth is now at the lowest level that we’ve seen in our estimates going back to 2017, surpassing a record set in the early months of the pandemic. The national median rent has now fallen from its 2022 peak by a total of 5.5%.

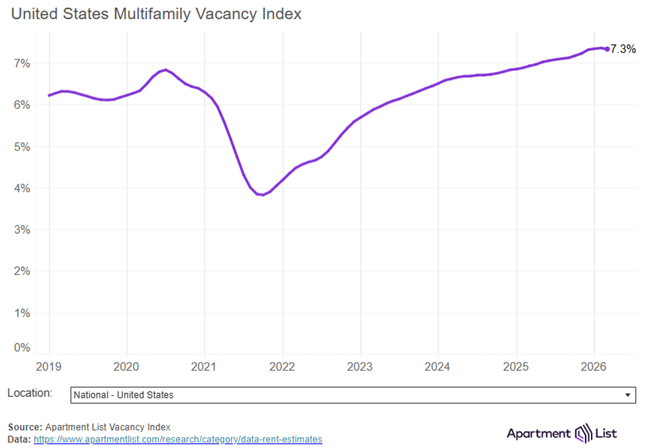

- The national multifamily vacancy rate held steady at 7.3% this month, a record high for our index going back to 2017. We’re past the peak of a multifamily construction surge, but a healthy supply of new units are still hitting the market and colliding with sluggish demand, causing vacancies to remain elevated.

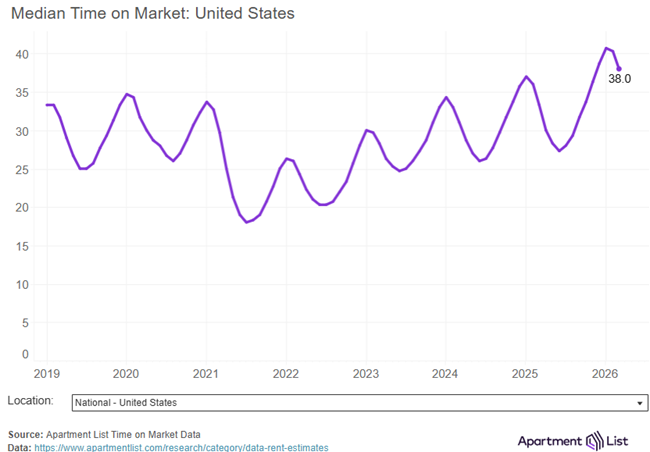

- Units are taking an average of 38 days to get leased after being listed, which is five days longer than one year ago, and more than twice as long as it took units to turn over when the market was at its hottest in mid-2021.

- The Austin, TX metro continues to have the softest conditions among the nation’s large rental markets, with the median rent there down by 6% over the past year. At the other end of the spectrum, the Virginia Beach, VA metro now sits atop our rankings of fastest year-over-year rent growth at +5.5%.

Multifamily vacancy rate at 7.3%, highest level since 2017

For now, conditions remain soft, and if anything, the runway for these sluggish conditions is likely only lengthening. The latest data from the Bureau of Labor Statistics showed U.S. employers cutting jobs, and the war in Iran is pushing prices higher just as inflation was getting back under control. These factors have put many households in a state of heightened financial uncertainty, which consequently puts a damper on housing demand.

List-to-Lease time remains elevated at 38 days

Despite the slight decline compared to last month, list-to-lease time remains notably elevated. This month’s reading is the longest that we’ve seen in any March going back to 2019 when our tracking begins (January’s 41 days set the overall record), and units are taking more than twice as long to turn over as they were in mid-2021 when the market was at its hottest. This lengthening of list-to-lease time is in line with negative rent growth, soft occupancy, and a generally cool rental market.

Conclusion

The wave of construction that has been driving these conditions is waning, but it now appears that weaker rental demand may keep rental conditions soft. A shaky labor market, renewed inflation concerns, and overall macroeconomic uncertainty are taking a toll on demand, meaning that it will take longer for the market to metabolize the recent growth in the rental stock, even if the construction industry slows in tandem.

{kind=link}