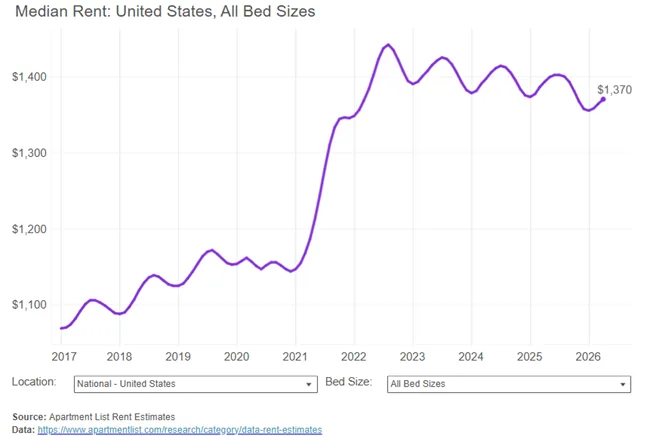

The national median rent increased by 0.5 percent in April, increasing for the third consecutive month following six straight monthly rent declines as vacancy index dropped also, Apartment List writes in the May report.

“We are now entering the time of year when the bulk of moves take place, and as such, we’ll likely see continued price increases through the summer, in line with typical seasonal patterns. Prices generally soften as fewer renters move during the fall and winter, and then gradually begin to increase as we get closer to the peak moving summer season,” the research team writes.

- After the increase of 0.5% in April, the national median rent is $1,370.

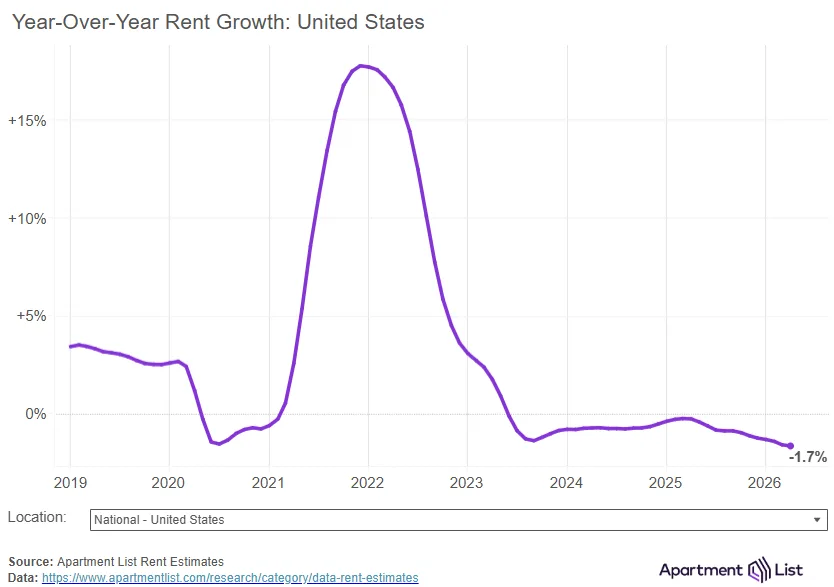

- Rent prices nationally are down 1.7% compared to a year ago. Year-over-year rent growth is “now at the lowest level that we’ve seen in our estimates going back to 2017, surpassing a record set in the early months of the pandemic. The national median rent has now fallen from its 2022 peak by a total of 5%,” the report says.

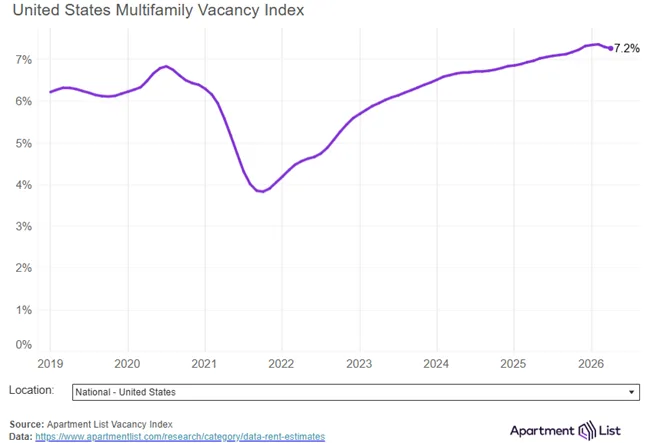

- The national multifamily vacancy rate ticked down to 7.2% this month. After hitting a new record in Q1, the vacancy rate may have now hit its peak and turned the corner. “This marks the first time that we’ve seen the vacancy rate decrease in over four years,” the researchers say.

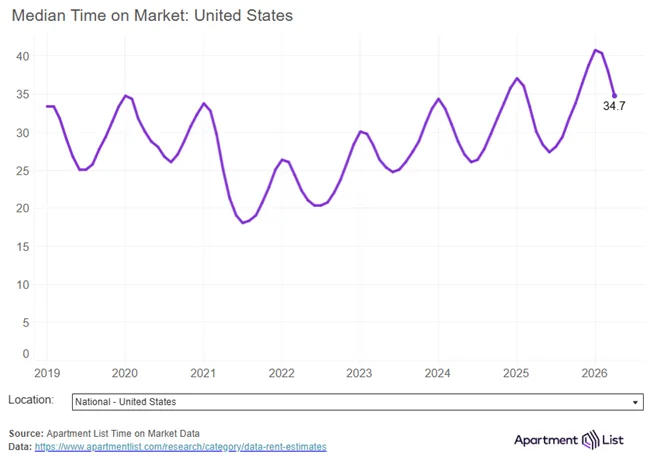

- Units are taking an average of 35 days to get leased after being listed, which is five days longer than a year ago, and nearly twice as long as it took units to turn over when the market was at its hottest in mid-2021.

- The Austin, Texas, metro continues to have the softest conditions among the nation’s large rental markets, with the median rent there down by 5.7% over the past year. At the other end of the spectrum, the Virginia Beach, Va., metro now sits atop the rankings of fastest year-over-year rent growth at +5.2%.

National median rent drop

Compared to one year ago, the national median rent is down by 1.7 percent.

At this time in 2025, it had appeared that year-over-year rent growth was on track to flip positive for the first time since mid-2023; however, that rebound stalled out and reversed course as demand has slowed amid a more uncertain labor market. Year-over-year rent growth has been gradually dipping further negative for a full year now, and the current reading of -1.7 percent is the lowest year-over-year rent growth recorded in the history of our estimates going back to 2017.

Multifamily vacancy down to 7.2%, first decline since 2021

The most important driver behind the soft market conditions that have persisted for three years is a historic surge of multifamily construction, which has gradually been absorbed. The vacancy rate has consistently loosened, gradually moving from record lows to record highs.

“We may now finally be reaching the point where the market begins to stabilize. However, it’s possible that the vacancy rate will simply plateau at this elevated rate, rather than continuing to decline in a meaningful way,” the research team says.

List-to-Lease time remains elevated at 35 days

The “list-to-lease” time is a highly-seasonal measure, and ticked down slightly this month, in line with the same seasonal pattern observed in our rent index. Units leased in April had been sitting on the market for an average of 35 days, down from 38 days in March.

Conclusion

“The rental market is beginning to enter its busy season, but multifamily conditions remain soft. Month-over-month rent growth stalled out in April, and year-over-year growth is at a new low. But even as the construction wave recedes, an uncertain macroeconomic outlook presents risks to rental demand,” the Apartment List research team says.

Read the full May report here.

{kind=link}